|

Proprietary Data Insights Financial Pros’ Top Midstream Oil & Gas Stock Searches in the Last 30 Days

|

|||||||||||||||||||||

|

Energy |

+30% Energy Pick Still Has Legs |

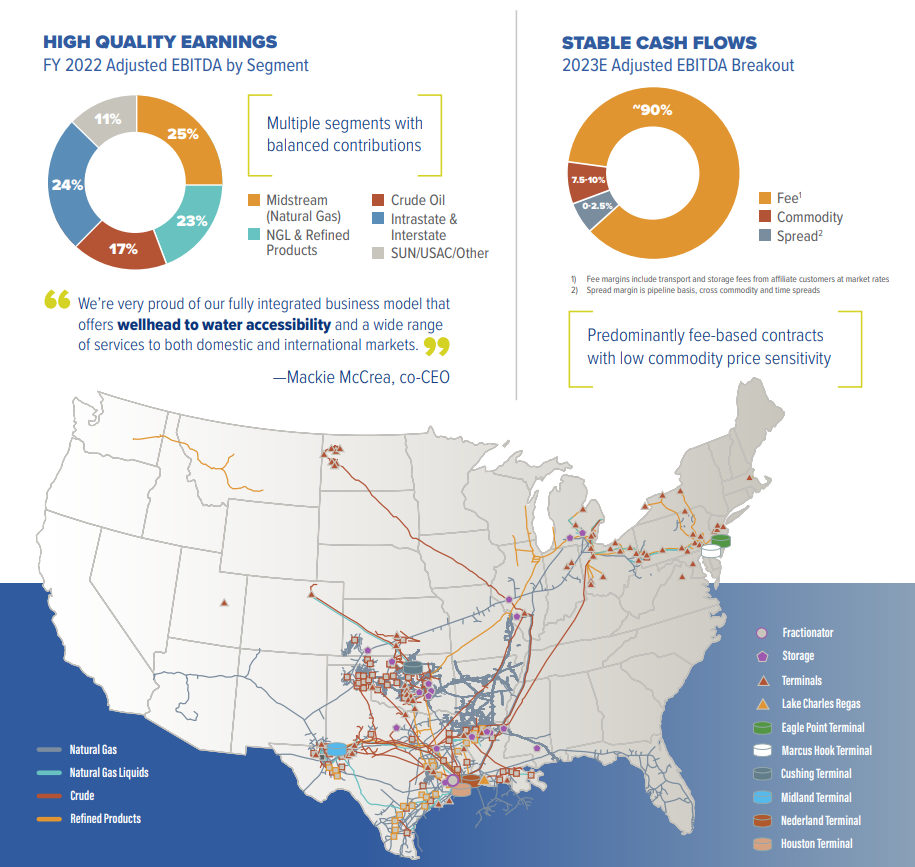

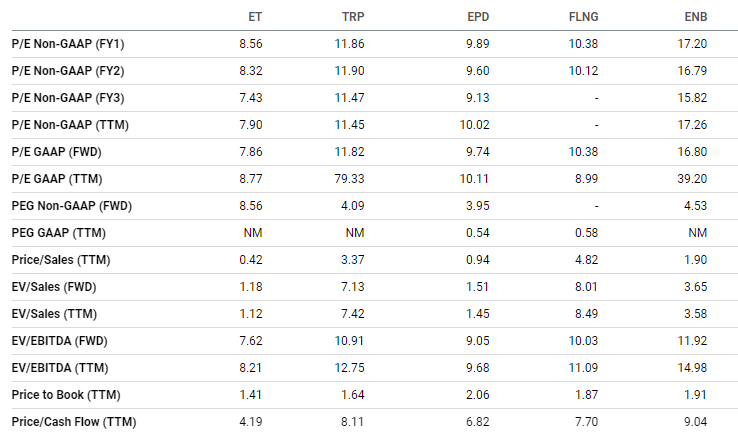

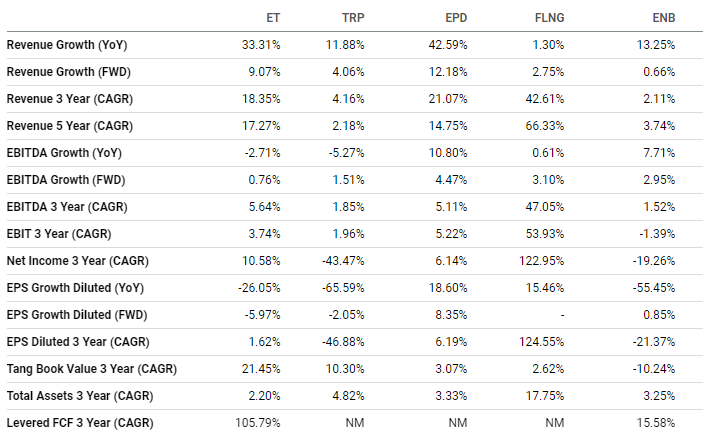

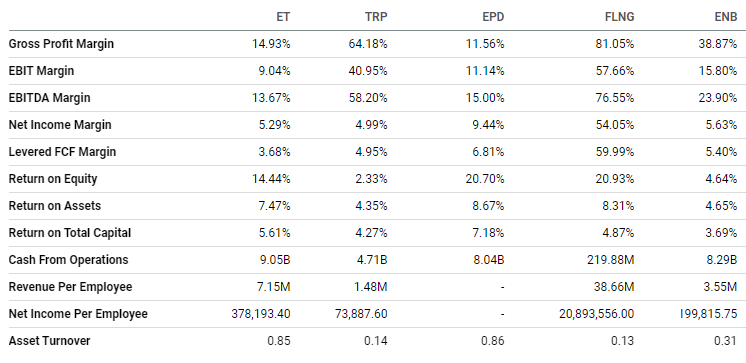

The energy boom has created a lot of winners. We shared our favorite midstream play a bit more than a year ago: Energy Transfer (ET). Since our write-up, the stock is up more than 30%, including dividends, which yield almost 10%! We got ahead of financial pros on this one, as it’s finally their top midstream oil and gas stock search for the last month, according to our proprietary Trackstar database. Here’s why ET is still our favorite pick in the space. Energy Transfer’s Business With nearly 120,000 miles of pipeline, Energy Transfer owns the second-largest pipeline network in the U.S., crossing 41 states to move oil and gas from drill sites to refineries. ET boasts a diversified portfolio that transports 30% of all U.S. natural gas and 35% of all U.S. crude oil. Source: Energy Transfer Website 85% to 90% of the company’s business is fee-based, meaning only volume matters, not commodity prices. Energy Transfer is a serial acquirer, buying companies and assets every year or two. Source: Energy Transfer 2022 was great for ET. It moved 21.6% more intrastate natural gas volume, 42.9% more interstate, and 11.8% more crude year over year. Financials Source: Stock Analysis Energy Transfer took full advantage of higher energy demand, helping revenues skyrocket 73.1% in 2021 and 33.3% in 2022. While this year’s revenue growth has been slow, management still expects it to hit 9.1%. Management expects capital expenditures to be $1.7 billion in 2023, which is lower than 2022’s $2.7 billion. It expects adjusted EBITDA to land between $12.9 and $13.3 billion, roughly in line with the last two years. As a midstream company, Energy Transfer must distribute all profits after CapEx to shareholders. While ET has $48.3 billion in long-term debt, that’s typical for an asset-heavy industry. Valuation Source: Seeking Alpha Compared to its peers, ET is the best across every measure in every category, except price-to-earnings growth in the trailing 12 months (TTM). But its 8.6x forward-looking price/earnings-to-growth ratio supersedes that. Growth Source: Seeking Alpha ET is still dominant in growth. While it doesn’t have the best YoY or forward revenue growth, nor YoY EBITDA growth, it’s still doing fantastic in nearly every category. One metric we love: 105.8% free-cash-flow growth. Profitability Source: Seeking Alpha Profitability is the one category where ET doesn’t always get great marks. But that’s more a function of the segments of its services rather than a problem with its operations. The company relies on high volume and low margins, as a grocery store does. Plus, ET’s got a healthy cash flow and decent returns on equity, assets, and total capital. We expect these numbers would be even higher if it halted its acquisition spree. Our Opinion 10/10 Energy demand isn’t dropping, even if the price of energy does. With the focus on cleaner alternatives, natural gas has become the fossil fuel of choice. We love this stock because ET operates the backbone of the industry. Its consistent operations mean the dividend is a great option to reinvest year after year. |

|

News & Insights |

Just Spilled |

|

Want to get content like this directly to your inbox? Then we urge you to sign up for our newsletter here |