|

Proprietary Data Insights Financial Pros’ Top Semiconductor Stock Searches in the Last 30 Days

|

|||||||||||||||||||||

|

Technology |

Did We Warm Up to Nvidia? |

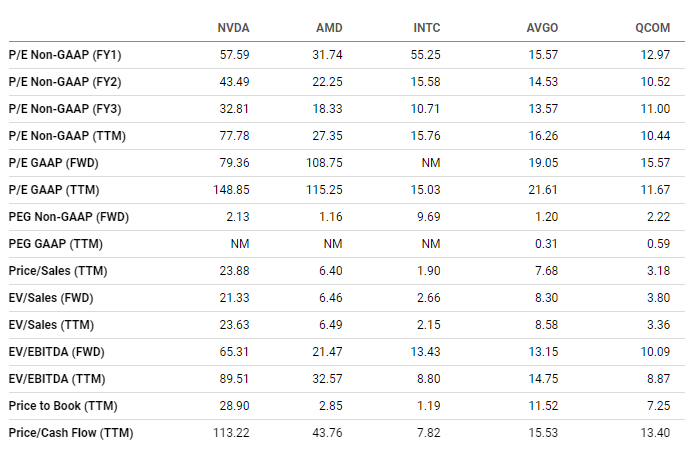

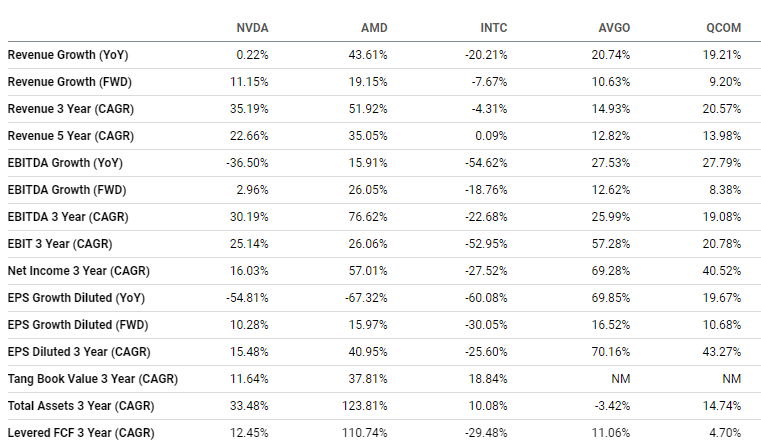

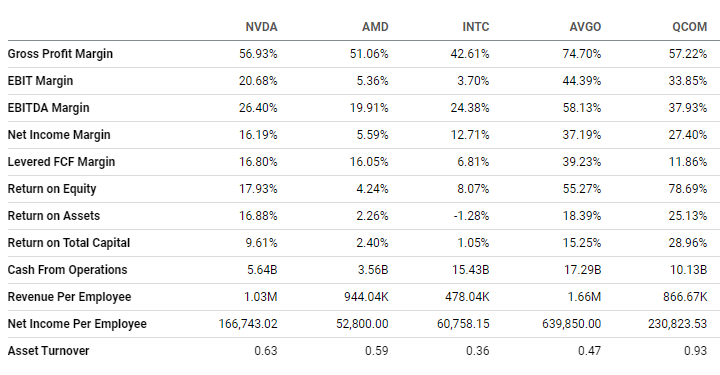

In August 2022, we covered one of the hottest semiconductor companies: Nvidia (NVDA). Back then, in our proprietary Trackstar database, it garnered only 35% more of financial pros’ searches than Advanced Micro Devices (AMD), the #2 search. Now, Nvidia pulls in nearly 3x the search volume. We gave NVDA a 6/10 in August. And we’ve changed our rating… Nvidia’s Business Most of us know Nvidia as the premium graphics card maker that blossomed in the late 1990s, disappeared for a decade, and reemerged as a leader in AI processing. The company’s parallel processing allows algorithms to run simultaneously on thousands of computing cores instead of just a few. Today, Nvidia dominates data centers, professional visualization, and gaming markets, leveraging partnerships with nearly every major cloud service provider. This was evident in NVDA’s presentation of 2022 financial results, where it showed how it splits revenues into five categories: Gaming, Data Center, ProViz, Auto, and OEM [original equipment manufacturer] & Other. Financials Source: Stock Analysis Until 2022, excluding 2019, Nvidia grew at a blistering pace. Yet it maintained excellent operating and profit margins. Excess supply from overproduction, a $1.6 billion charge for terminating the company’s ARM Holdings acquisition, and higher research and development costs raised operating expenses for 2022. But management said it expects better gross margins and flat operating expenses in Q1 this year. And Nvidia holds plenty of cash and very little long-term debt relative to its size. Valuation Source: Seeking Alpha We struggled with the company’s valuation before and still do. It’s hard to get behind a company that’s valued at nearly 80x forward earnings and 113x operating cash. We know Intel (INTC) has all sorts of challenges. But it’s a fraction of NVDA’s price. Everything here says Nvidia is expensive. Growth Source: Seeking Alpha Nvidia bulls argue the company makes up for valuation in growth. But the company’s year-over-year growth shows how difficult the processor environment can be. AMD had better growth over the last several years and is far cheaper by price-to-cash-flow and non-GAAP price-to-earnings ratios. Profitability Source: Seeking Alpha That’s not to say Nvidia doesn’t deliver excellent margins and returns. While it’s not always the highest in every category compared to its peers, its returns on equity and assets are top-notch. And its return on capital is pretty decent too. Our Opinion 4/10 With higher interest rates and a forecasted recession looming, we can’t get behind NVDA. Its growth doesn’t justify its multiples. It makes great products and delivers on its promises. But the stock is simply too expensive. |

|

News & Insights |

Just Spilled |

|

Want to get content like this directly to your inbox? Then we urge you to sign up for our newsletter here |