|

Proprietary Data Insights Financial Pros’ Top Communications Equipment Stock Searches in the Last 30 Days

|

|||||||||||||||||||||

|

Technology |

3% Dividend but No Growth |

Communication equipment isn’t a sexy business. But it can be quite lucrative. Cisco Systems (CSCO) has been at it since 1984. It’s been a dominant player in the space since 1993, when it introduced its improved 7000 series router. But it failed to change with the times, and shares stagnated from 2001 to 2016. Recently, our proprietary Trackstar database has shown sporadic interest in CSCO from financial pros searching for communications equipment stocks. That might relate to the nationwide 5G rollout. We covered CSCO stock last May and gave it a 7/10. Given the recent interest in it and outperformance of the S&P 500 and Nasdaq-100, we checked if Cisco deserves a spot in your long-term portfolio now. Cisco Systems’ Business Network security helped Cisco pull out of its 15-year malaise. The company has been rapidly expanding its presence in this domain with products and services that:

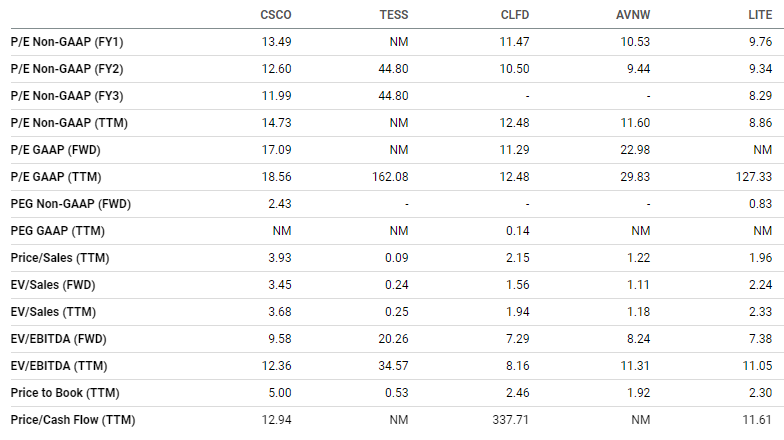

Cisco boasts a massive global presence, with most of its sales coming from the U.S. Source: Cisco Systems Products make up almost three-quarters of the company’s total sales. Interestingly, the gross margins on products and services are pretty close to one another. Source: Cisco Systems FY 2022 annual report Financials Source: Stock Analysis Cisco’s revenues plateaued in 2019. It took until the latest rolling 12-month period for it to break its peak. Otherwise, growth has been lackluster at best, which has been a common critique of the company. Cisco has done an excellent job maintaining margins and returning cash to shareholders with a 3% dividend payout, a healthy share buyback program, and paying down a huge amount of its debt. It just doesn’t grow. Valuation Source: Seeking Alpha The lack of growth is largely why the valuation is so compelling. Cisco trades at just 12.9x trailing and forward operating cash flow. Its price-to-earnings ratios aren’t great. Clearfield (CLFD) is better in trailing and forward, coupled with sizable growth, which you’ll see in the next table. And at 3.9x, CSCO trades at the highest price-to-sales ratio of its peers. Growth Source: Seeking Alpha As we mentioned, CSCO hasn’t grown much, unlike CLFD. CSCO’s 5.7% forward growth outlook isn’t that great either. No one gets excited for a company that’s just plodding along. Profitability Source: Seeking Alpha Cisco’s margins are the best of the bunch across every category. And its returns on equity, assets, and total capital are outstanding. Our Opinion 7/10 We kept our original rating because CSCO’s downside is fairly limited. We don’t expect big things from this stock. But at the right price, say $47.50 or so (it currently trades at $49.76), it’s worth a look. |

|

News & Insights |

Just Spilled |

|

Want to get content like this directly to your inbox? Then we urge you to sign up for our newsletter here |