|

Proprietary Data Insights Financial Pros’ Top Oil & Gas Refining & Marketing Stock Searches in the Last 30 Days

|

|||||||||||||||||||||

5.75% Dividend Yield |

|

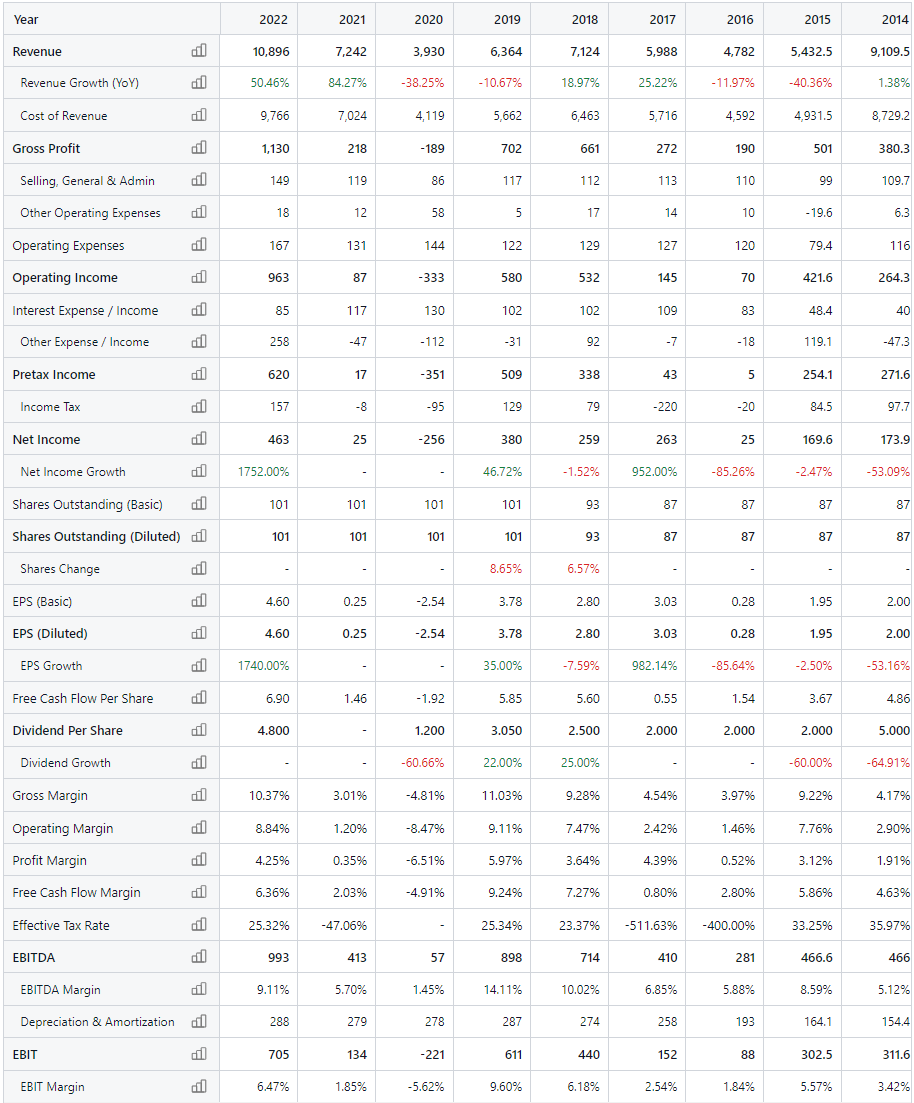

Billionaire Carl Icahn doesn’t shy away from big bets. His company Icahn Enterprises has a 71% stake in CVR Energy (CVI). Within less than a week, CVI recently surged from 0 to 96 searches in one day, according to our Trackstar database. And financial pros keep searching for it. The company pays a whopping 5.75% dividend yield. But it has a complicated business model. Is it right for your portfolio? CVR Energy’s Business CVR Energy owns and operates CVR Refining, which consists of two mid-continent refineries and linked pipelines. It also owns 37% of CVR Partners (UAN), which owns two fertilizer plants. CVR Energy is exploring spinning off its UAN stake by forming a holding company that would trade independently of UAN and CVI. Some of the company’s strategic priorities include focusing on environmental, health, and safety matters; preserving cash flow; and maximizing shareholder returns. Financials Source: Stock Analysis Saying revenues have exploded is an understatement. They nearly tripled from 2020 to 2022. Yet gross, operating, and profit margins were largely the same. That’s typical for refiners that profit more from volume than oil prices. But CVI’s ownership in UAN gives it a more diverse revenue stream than most refiners have. The company maintains low levels of debt that it could pay off in two years based on free cash flow. Valuation

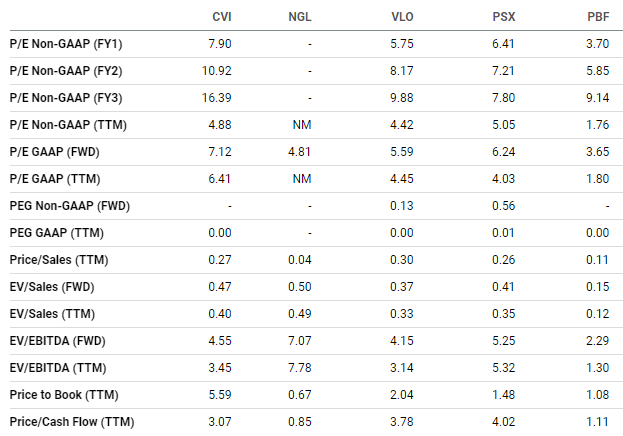

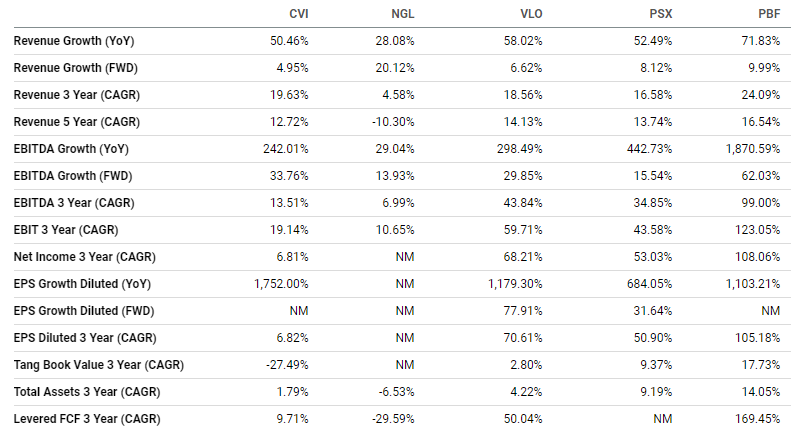

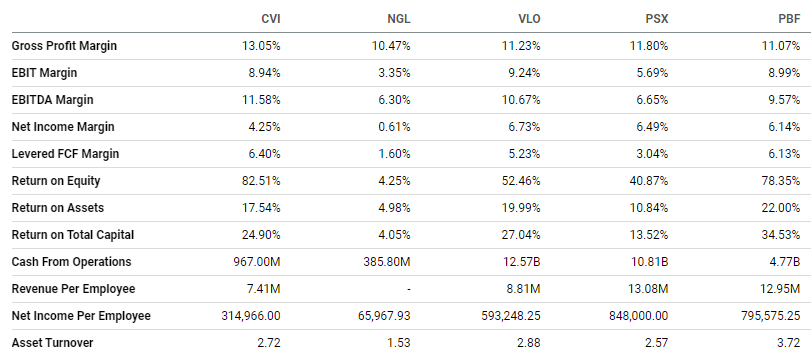

Source: Seeking Alpha Like many oil and gas companies, CVI trades at a pretty cheap valuation, with a trailing price-to-earnings ratio of 6.4x and a forward P/E ratio of 7.1x, though this is more expensive than the peers we compared CVI to. Also like its peers, CVI has a great price-to-cash ratio: just 3.1x. Growth Source: Seeking Alpha CVI’s year-over-year growth was fantastic, though three of its peers beat it. It also has one of the lower forward revenue growth estimates. But it has great three- and five-year average growth rates. And its forward EBITDA growth estimates are the second-best of the group. Profitability Source: Seeking Alpha Interestingly, CVI has better gross margins than its peers, though its EBIT and net income margins are in the middle to lower end of the pack. Of the group, it has the best return on equity. Its returns on assets and total capital are nice.

Our Opinion 9/10 We love CVI’s diverse revenue streams. And its potential spinoff is a catalyst for higher share prices. Management is very shareholder-friendly. We don’t rate this stock a 10 only because some of its peers look a bit better. |

|

News & Insights |

Just Spilled |

|

Want to get content like this directly to your inbox? Then we urge you to sign up for our newsletter here |