|

Proprietary Data Insights Financial Pros’ Top Utility Stock Searches in the Last 30 Days

|

|||||||||||||||||||||

Why AEE Stands Out From Other Utilities |

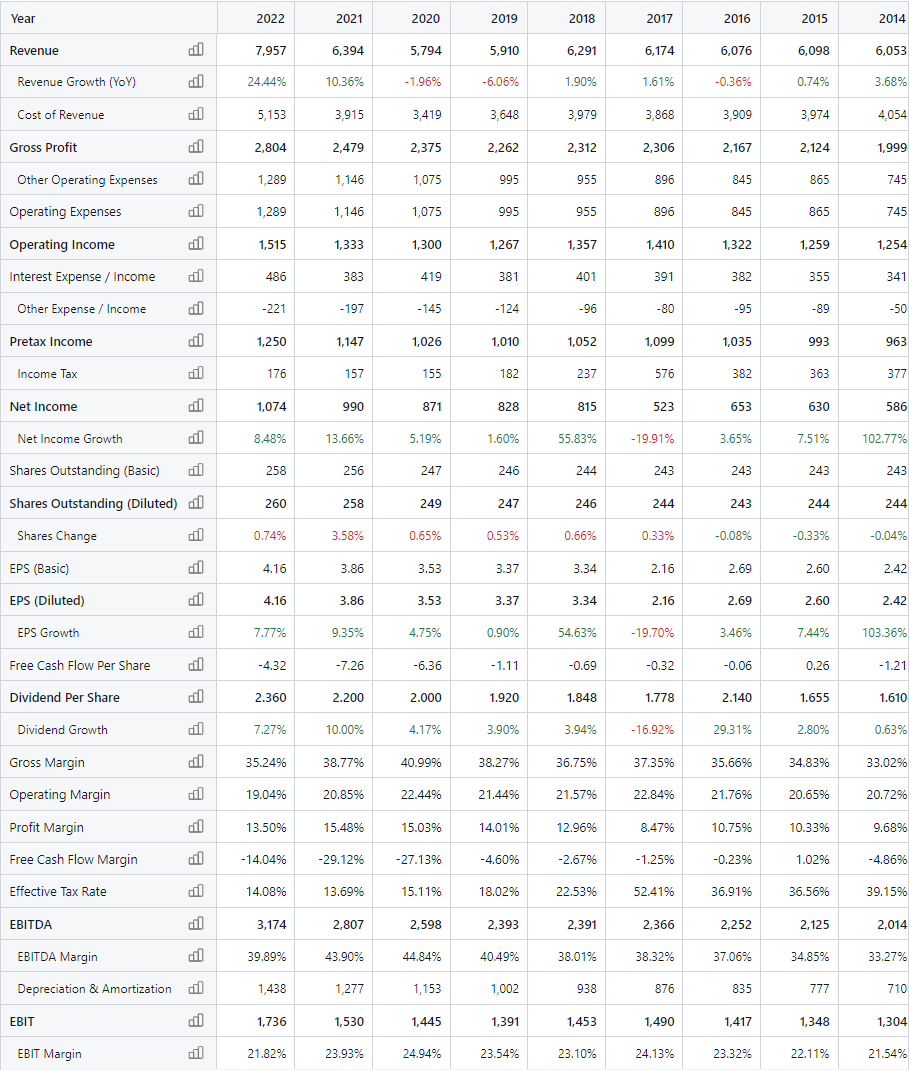

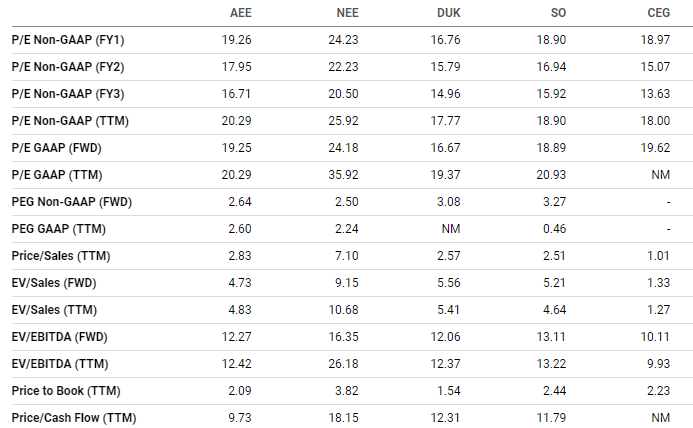

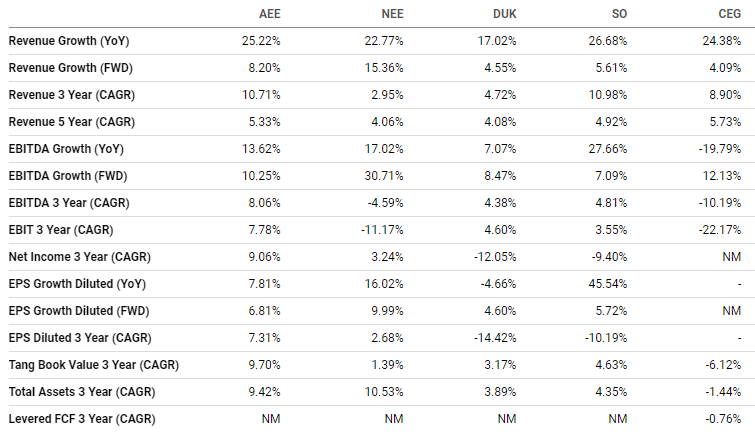

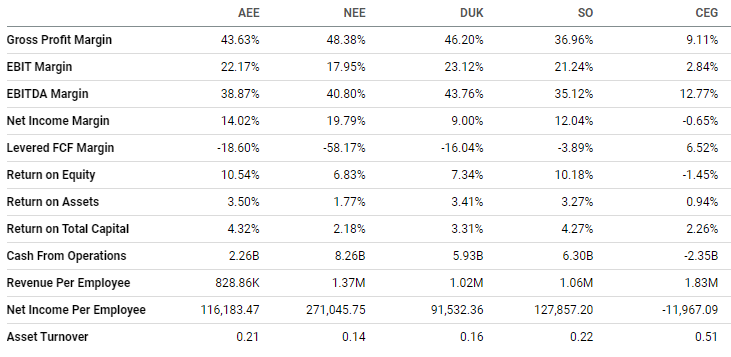

Utilities are the curmudgeons of industrials. They’re stuck in their ways and refuse to change. Ameren (AEE) is a bit different, which is probably why financial pros have lately taken such an interest in this stock, according to our Trackstar database. Before AEE’s earnings last month, they hadn’t searched for it in weeks. Though the utility’s valuation is mediocre, the company’s story really stands out. Ameren’s Business Ameren is a multi-utility company based in St. Louis. It generates and distributes electricity and natural gas to customers in Missouri and Illinois. Ameren’s Missouri segment leverages coal-fired, nuclear, natural gas, and renewable facilities. The company aims to reduce its carbon emissions 60% from 2005 levels by 2030 and 85% by 2040, with the goal of net zero by 2045. Additionally, it plans to expand its renewable energy output to 2,800 megawatts by 2030 and 4,700 MW by 2040. Financials Source: Stock Analysis Revenues grew steadily through 2019, when they took a hit that the pandemic exacerbated in 2020. But Ameren announced it expects earnings per share to have a compound annual growth rate of 6% to 8% from 2023 to 2027 and base rates to have a CAGR of about 8% for the same period. While the company spends a good chunk of its cash – about $260 annually – on nuclear decommissioning and environmental compliance, operating cash flow exceeds $2.2 billion annually. Currently, Ameren holds $13.7 billion in long-term debt, which isn’t much relative to its cash flow or its $31.3 billion in property, plant, and equipment. But its interest expenses are a hefty $486 million annually and will likely get more expensive over time. Valuation Source: Seeking Alpha AEE isn’t cheap compared to its peers. It trades at one of the highest price-to-earnings trailing multiples and in the middle for forward multiples. Plus, its price-to-book ratio of just 2.1x shows investors don’t place as much value on its assets as they do for other utilities. But its price-to-cash-flow ratio is fantastic at just 9.7x. Growth Source: Seeking Alpha AEE earns top marks for its year-over-year revenue growth. And though it’s not top looking forward, it’s still double most of its peers. Overall, AEE consistently delivers growth, whether on revenues, EBITDA, or EPS. Profitability Source: Seeking Alpha While AEE isn’t the most profitable, it’s pretty close, whether we’re talking about gross or net income margin. And it does darn good with returns on equity, assets, and total capital. Our Opinion 7/10 Normally, we wouldn’t be too hot on utilities in a high-interest-rate environment, since they tend to be loaded with debt. But Ameren doesn’t have as much debt as other utilities. And its cash flow could easily pay off its tab. Plus, it’s got decent growth with a solid outlook. |

|

Want to get content like this directly to your inbox? Then we urge you to sign up for our newsletter here |