|

Proprietary Data Insights Top Software Stock Searches This Month

|

|||||||||||||||||||||

Uber Eats the Competition |

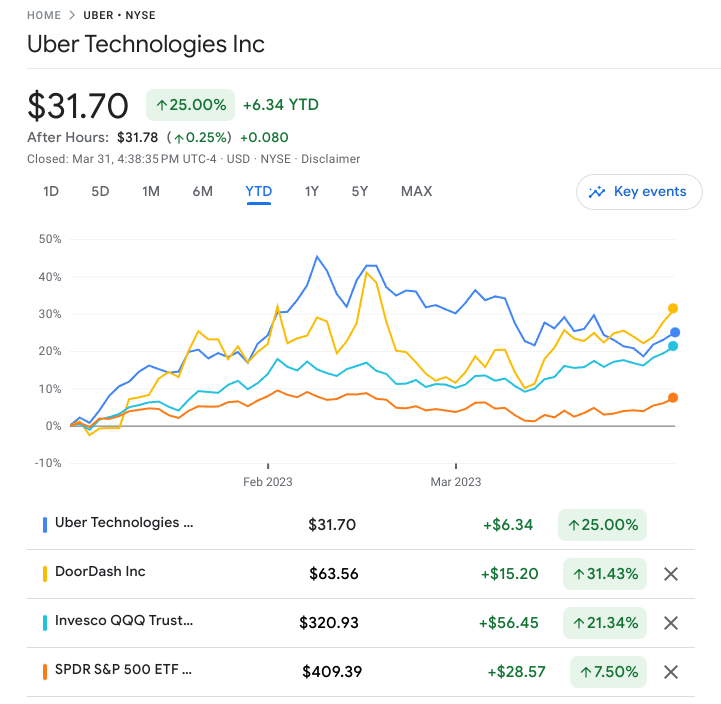

Source: Google Finance Over the last several months, The Juice has been beating the bullish drum for two relatively speculative stocks – DoorDash (DASH) and Uber (UBER). Year-to-date, they’re both crushing the game, outpacing the S&P 500 (SPY) by a mile and the rallying Nasdaq-100 (QQQ) by a comfortable margin. Interestingly, neither stock shows up among the most searched software stocks in Trackstar, our proprietary sentiment indicator. However, as we have said in the past, sometimes it’s a good thing when you’re following a stock, you’re getting excited about it, it’s performing well and it still flies under the radar. We’ll update DASH another time, but today we focus on Uber. So much of what’s happening at the company simply doesn’t get reported – or goes under-reported – in the popular and financial media. We’re fine with this. Because we know Uber is much, much more than a rideshare service that delivers takeout. We relay the latest under-the-radar news on the company in a second, but first, a review of our bull case, as Uber continues to build one of tech’s most expansive and impressive ecosystems since Amazon.com (AMZN). October 19, 2022: Can Canada Get Uber High? We want to hear Uber tell investors it’s striking while the iron is hot. That this Toronto experiment is the beginning of bold, innovative, and creative moves. More pushing the envelope the way the company did when it pissed off city after city by aggressively disrupting the taxi industry. For starters, we want to hear it’s expanding weed delivery into major U.S. cities. Beyond that, Uber needs to do a better job becoming part of your daily life in multiple areas. Just like Amazon’s done via Prime membership. Since we penned that piece, UBER is up roughly 15%. While there’s no word yet that Uber plans to help get more of North America high, the company continues to leverage rideshare into potentially lucrative targeted advertising partnerships. Last November, we detailed how Uber continues to grow its advertising business. We think we’re onto something. Here’s what Uber CEO Dara Khosrowshahi had to say about its ad business on its most recent earnings conference call (bold emphasis added): And I think just on Ads, for folks out there, we passed $500 million in annual run rate, and that’s based on increasing the number of active advertisers that we have, like 80% on a year-on-year basis. But if you look at the merchant penetration, the percentage of merchants on our delivery side who are advertising, only 25% of our merchants are active in the auctions that we have going on. So we think there’s substantial upside to our Advertising business. We committed to $1 billion in revenue by 2024, and we are progressing very, very well against that target. Bull-ish. Now the latest effort by Uber to diversify its revenue streams: The Certified Virtual Restaurant Program allows merchants to tap into a pipeline of virtual restaurant concepts curated by Uber and vetted to meet high-bar standards in menu quality, operations, and branding… By participating in the program, independent restaurants will have access to virtual concept creators’ account management and customer success teams, and can leverage their expertise in operating quality virtual restaurants successfully on Uber Eats—whether operated out of an existing brick-and-mortar restaurant or a delivery-only kitchen. That’s from a press release Uber released late last week announcing its Certified Virtual Restaurant Program, which basically provides turnkey programs for restaurateurs looking to create restaurants that operate primarily – and often solely – with an online presence. The Bottom Line: Thanks to its rideshare core, Uber has tons of data. It can use this data to expand into other areas, such as targeted advertising and building out virtual restaurant concepts via Uber Eats. We haven’t seen this type of synergistic ecosystem since Amazon. We’ll continue to keep you updated. And we’ll continue to suggest shares of UBER stock, particularly for long-term investors with a decent size appetite for risk and huge desire for potentially out-sized rewards. |

|

News & Insights |

Freshly Squeezed |

|

Want to get content like this directly to your inbox? Then we urge you to sign up for our newsletter here |