|

Proprietary Data Insights Financial Pros Investors Top Discount Store Stock Searches in the Last 30 Days

|

|||||||||||||||||||||

Costco’s Valuation Problem |

|

Costco (COST) is the 3rd largest retailer in the world with:

Source: Costco Investor Presentation Until recently, it was the MOST popular discount retailer by search volume amongst financial pros. And while it’s still #2, many are beginning to worry that the stock’s price has gotten over its skis. The stock trades at a whopping 34.3x next year’s earnings and 23.1x cash. That’s fairly rich for a company who’s managed 11.5% average revenue growth over the last five years and requires large amounts of capital expenditures to move forward. Yet, its loyal customer base and massive private brand selection keep surprising analysts. So what do we think? Costco’s Business For $120 a year, you can become a Costco member, gaining access to some pretty fabulous deals. The retailer runs discount stores where members pay an annual fee for the privilege of shopping in the store and online. Originally a bulk retailer, Costco has expanded into categories from food to airlines. A quick look at the new brands below shows you what we’re talking about: Source: Costco Investor Presentation Costco’s business model is simple. They mark up their goods 14% over cost and charge a membership fee. That’s it. Given the 5-year and 7-month cadence, the company is probably due for a membership price hike soon. Inflationary pressures have actually helped Costco in some ways, pushing customers toward its private label items, including Kirkland Signature. The company reported solid growth in its store brand sales penetration by +1.5% YoY for food products in FQ2’23 vs. +0.5% annually over the past ten years. Additionally, Cosco forecasts moderating inflationary pressures, with prices declining to between 5% and 6% YoY as of FQ2’23, against 6% to 7% in FQ1’23 and 8% in FQ4’22, interestingly focused on food products Financials Source: Stock Analysis Costco’s done a solid job driving revenue growth in the last few years, pushing out of the single and into double digits. However, gross margins declined while profit margins improved slightly. Believe it or not, the company holds hardly any long-term debt. And with free cash flow of +$4 billion or $12.34 per share, it can easily afford the tiny 0.72% dividend.

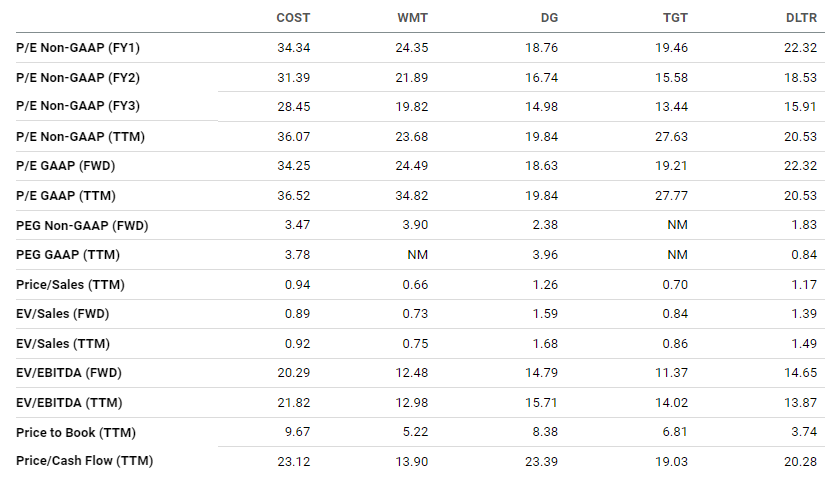

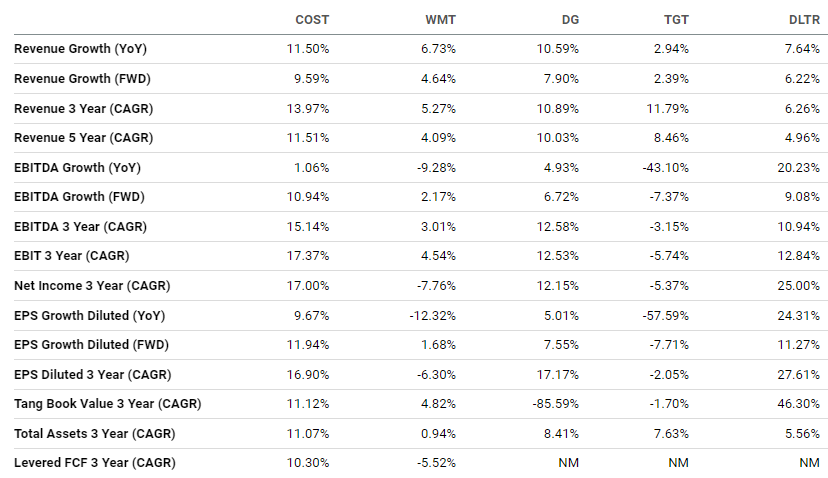

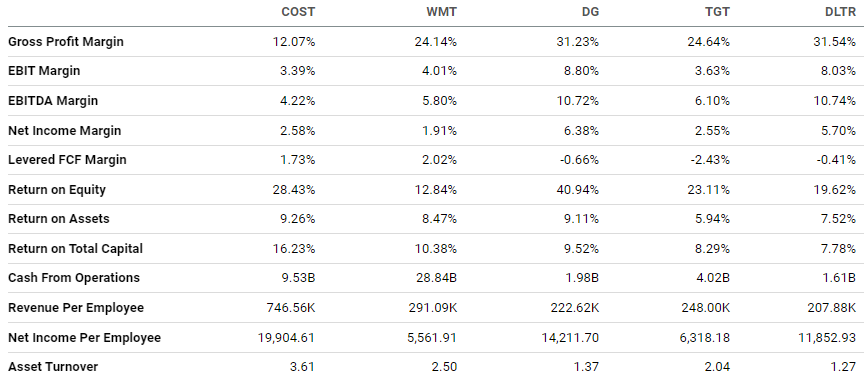

Valuation Source: Seeking Alpha When the rubber meets the road, Costco is just expensive. It trades at a higher P/E, multiple than all its peers, and is the second most expensive measured by price-to-cash flow. Growth Source: Seeking Alpha Yes, Costco boasts fantastic growth. But Dollar General (DG) comes pretty close and is half the price of Costco in terms of P/E ratio, though as expensive looking at price-to-cash. Profitability Source: Seeking Alpha Costco’s gross margins aren’t as good as its peers, nor are its EBITDA, EBIT, or net income margins. Our Opinion 6/10 Costco is a great business. But it’s not worth paying the premium. Even Dollar General, which appears to be cheaper, still isn’t that exciting. If we’re going to pay for a stodgy store, we want a lot more bang for the buck. |

|

Want to get content like this directly to your inbox? Then we urge you to sign up for our newsletter here |