|

Proprietary Data Insights Financial Pros Investors Top Drug Manufacturers Stock Searches in the Last 30 Days

|

|||||||||||||||||||||

Does Eli Lilly Deserve Its Price Premium? |

|

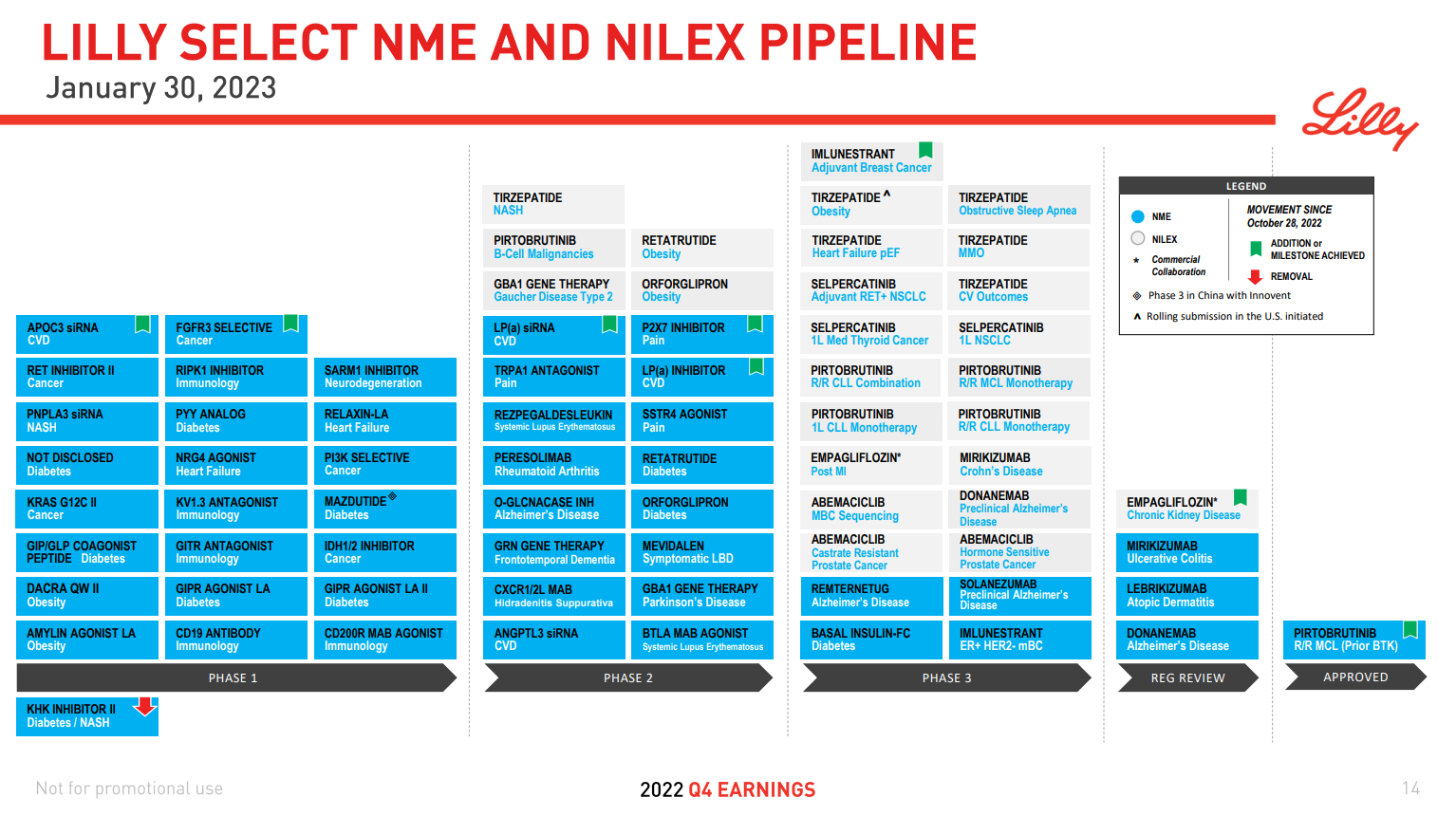

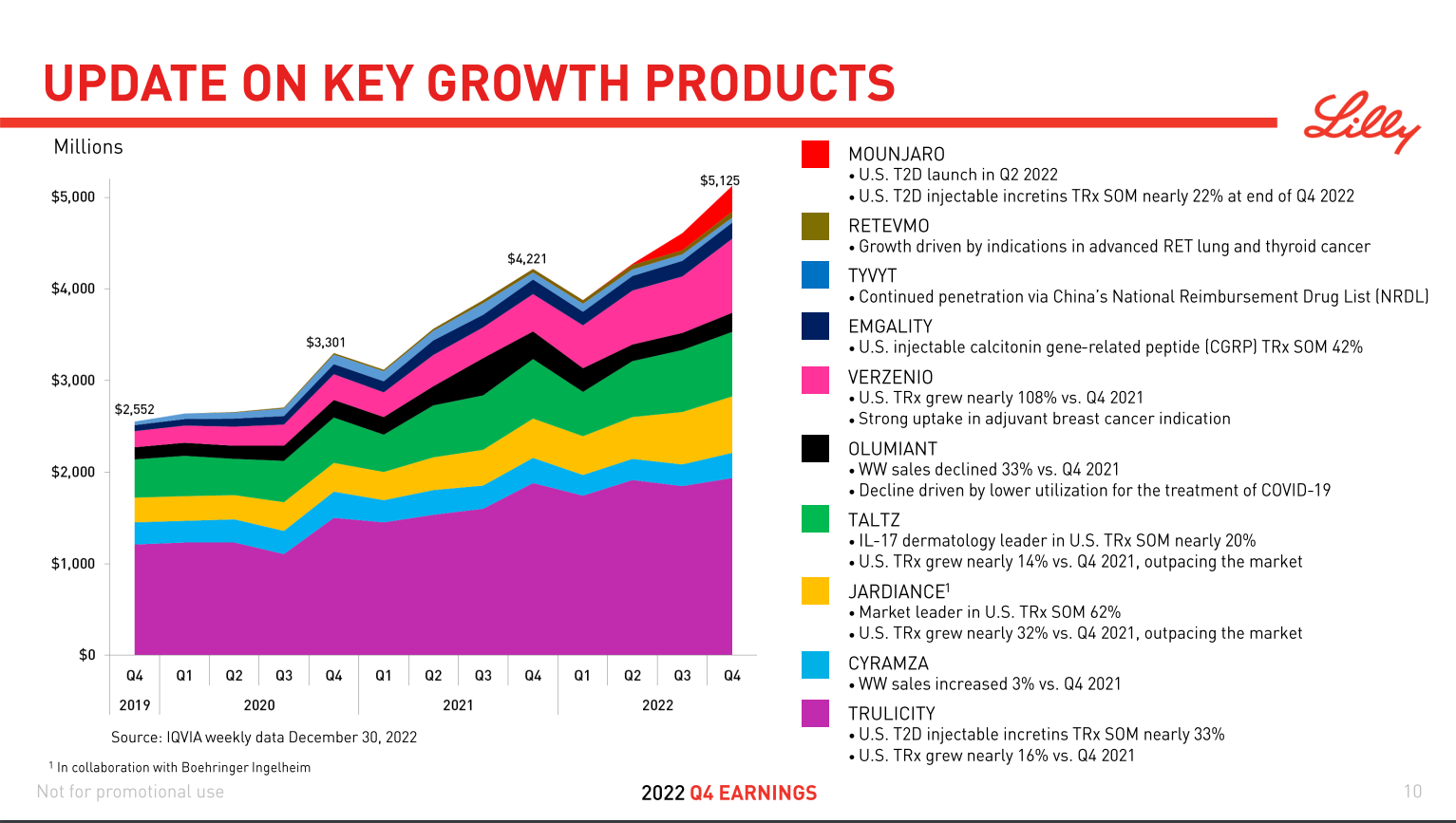

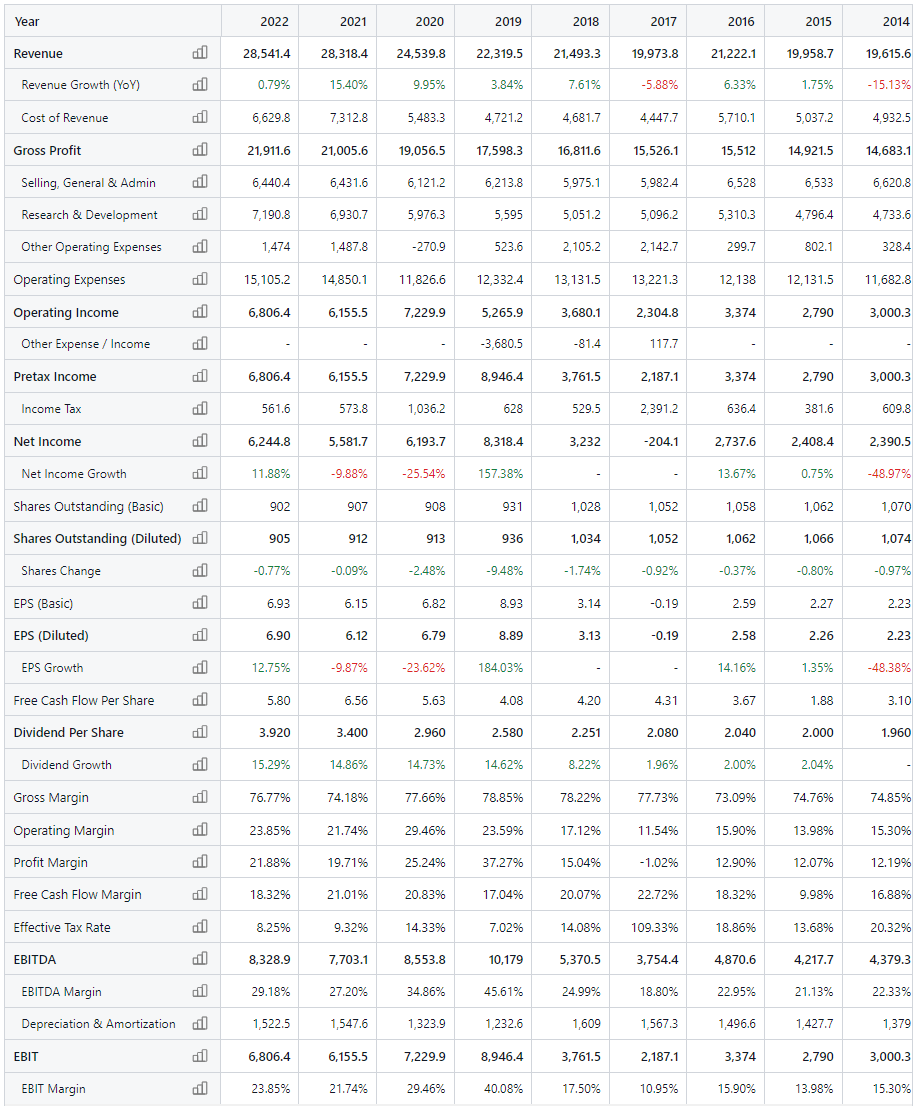

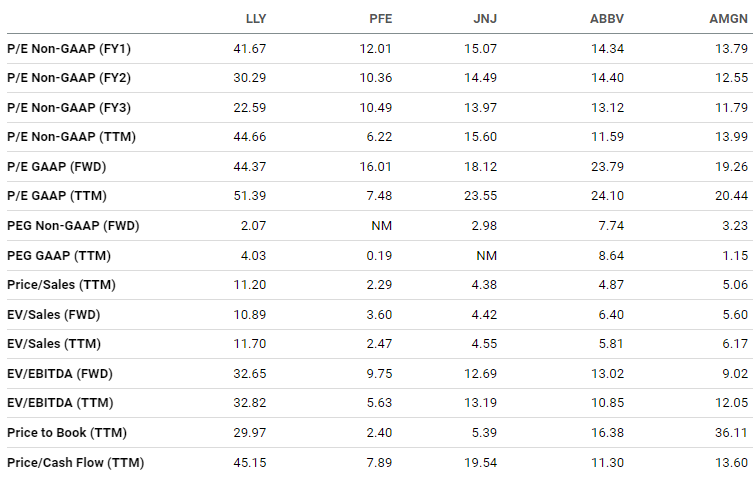

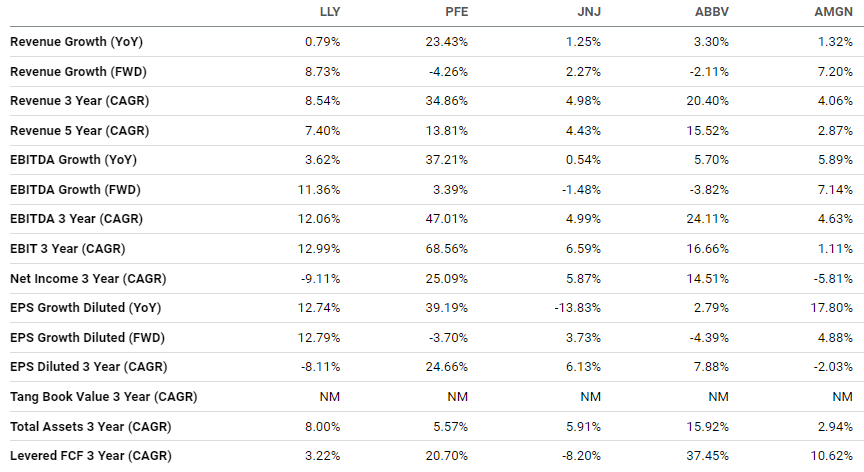

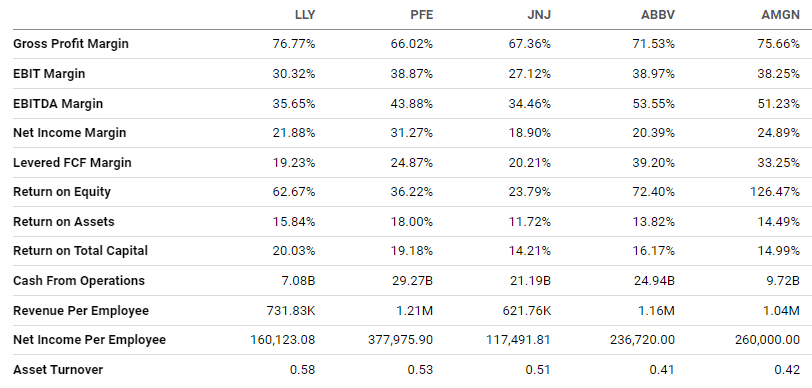

Among financial pros’ top five drug manufacturer stock searches, Eli Lilly (LLY) performed best over the last year, up 23% in price. Over five years, LLY is up 394%. Only AbbVie (ABBV) comes close at 117%. Although Eli Lilly expects revenues to climb 8.7% next year, beating all its peers, the stock is expensive, trading at double the price-to-earnings and price-to-cash ratios of its nearest competitor. So does it make sense to put LLY in your portfolio? Eli Lilly’s Business Eli Lilly rose to fame in the 1990s with its blockbuster antidepressant Prozac. Since then, the company has become one of the largest pharmaceutical players in the world. Its drugs cover a wide range of categories, from neuroscience to oncology. The company boasts one of the largest drug pipelines in the marketplace. Source: Eli Lilly And investors are really excited about the key growth products the company has launched in the last few years. Source: Eli Lilly These products are so important to Eli Lilly’s business that despite a huge negative impact on volume from COVID-19 antibodies, these products grew 15.3%, netting the company a drop of just 2% in overall volume growth. Financials Source: Stock Analysis It’s interesting to see LLY’s premium valuation given the stock’s decent but not blockbuster revenue growth. That may be due to LLY’s massive improvement in profit margin since 2018. Yet its free-cash-flow margin is only slightly higher. Nonetheless, with $22 billion in cash and no real long-term debt, Eli Lilly can acquire its way to the future. Valuation Source: Seeking Alpha Investors are apparently willing to pay nearly twice as much for LLY as for its competitors. To give you an idea of how rich the valuation is, famously sky-high-value Tesla (TSLA) trades at 53.1x trailing earnings and 41.5x trailing cash. Growth Source: Seeking Alpha Speaking of which, it’s safe to say Eli Lilly’s growth doesn’t come close to Tesla’s. In fact, it’s barely better than its peers in many respects. Profitability Source: Seeking Alpha And here’s another kick in the pants: Tesla runs a 15.4% net income margin, not too far behind Eli Lilly’s. In fact, compared to its peers, Eli Lilly’s profitability isn’t that impressive.

Our Opinion 3/10 Eli Lilly may be a great company with a fantastic pipeline. But there’s no reason to overpay for LLY stock. There are plenty of comparable drug companies with better growth and valuations. |

|

News & Insights |

Just Spilled |

|

Want to get content like this directly to your inbox? Then we urge you to sign up for our newsletter here |