|

Proprietary Data Insights Financial Pros’ Top Downstream Oil and Gas Stock Searches in the Last 30 Days

|

|||||||||||||||||||||

Can This 7.4% Dividend Survive Recession? |

|

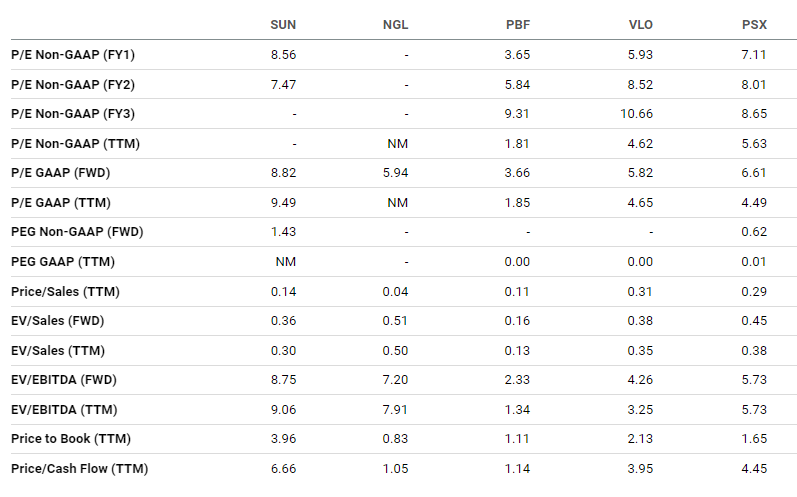

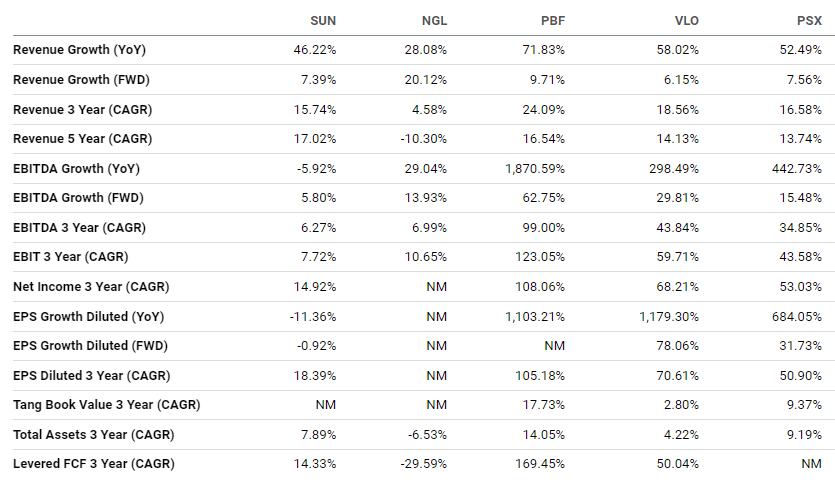

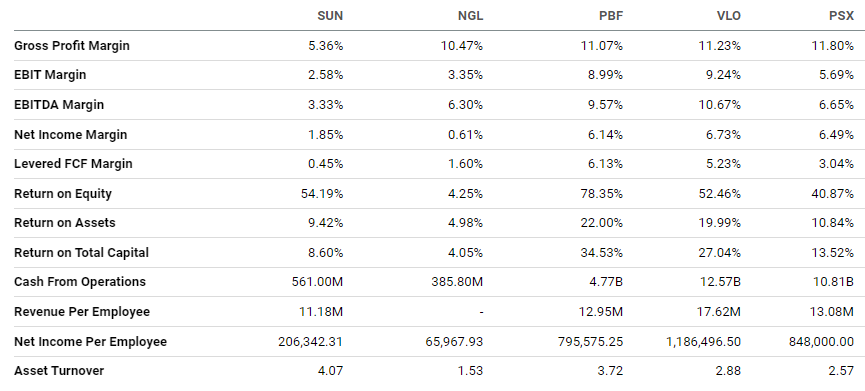

Sunoco (SUN) tops our list of downstream oil and gas plays. These companies refine and market gasoline. Essentially, they make gas and sell it at their gas stations. This stock is financial pros’ top search among its peers, according to our proprietary Trackstar database. And its 7.43% dividend is nearly twice that of the next one on this list. But can the company maintain its dividend in a recession? Sunoco’s Business With 10,000 convenience stores across more than 30 states, Sunoco is one of the U.S.’ biggest motor fuel distributors in terms of volume. The company buys fuel from refiners and sells it to customers. That accounts for 96.3% of the company’s revenues. Sunoco is a master limited partnership (MLP). MLPs pay out most of their profits as dividends to avoid corporate income taxes. Financials Source: Stock Analysis Sunoco’s biggest danger is that higher oil prices and a recession will dampen demand and hurt sales. But its revenue growth is usually steady because of the company’s prudent management and acquisitions. Though the recent growth could retrench after a record-breaking year, forecasts still put the company up 7.4% for sales this year. Sunoco carries $3.5 billion in long-term debt. But it’s lowered the ratio of its net debt to operating cash flow since 2019, a trend likely to continue so long as interest rates remain high. Valuation Source: Seeking Alpha Most energy names trade at reasonable valuations given their record-breaking profits and margins. So it’s a bit concerning to see Sunoco trade at 6.7x cash flow. That said, NGL Energy Partners (NGL) doesn’t pay a dividend, PBF Energy (PBF) yields just 1.9%, Valero (VLO) yields 3.0%, and Phillips 66 (PSX) yields 4.0%. So higher dividend payouts mean higher price-to-cash-flow ratios. Growth Source: Seeking Alpha Sunoco’s growth has been ridiculous. 2022 lapped 2021, and 2021 growth exploded past 2020 and the pandemic. Again, forecasts predict growth of around 7% for 2023. Profitability Source: Seeking Alpha SUN has lower margins than its peers. But it’s more of a pure marketing and distribution play than the others. Sunoco simply buys gas and resells it. Others also refine oil into gas, yielding slightly higher gross margins. Nonetheless, Sunoco does great with returns on equity, assets, and total capital, even if it’s not in the top spot. Our Opinion 10/10 We believe SUN’s dividend is safe. Demand for gasoline is unlikely to drop anytime soon. And even if it does, it likely won’t majorly impact Sunoco, given its revenues’ historical resiliency. We love this play right now and think it has great management to keep returning value to shareholders. |

|

News & Insights |

Just Spilled |

|

Want to get content like this directly to your inbox? Then we urge you to sign up for our newsletter here |