|

Proprietary Data Insights Financial Pros’ Top Farm Equipment Stock Searches in the Last Month

|

|||||||||||||||||||||

Other Stocks Don’t Run Like a Deere |

|

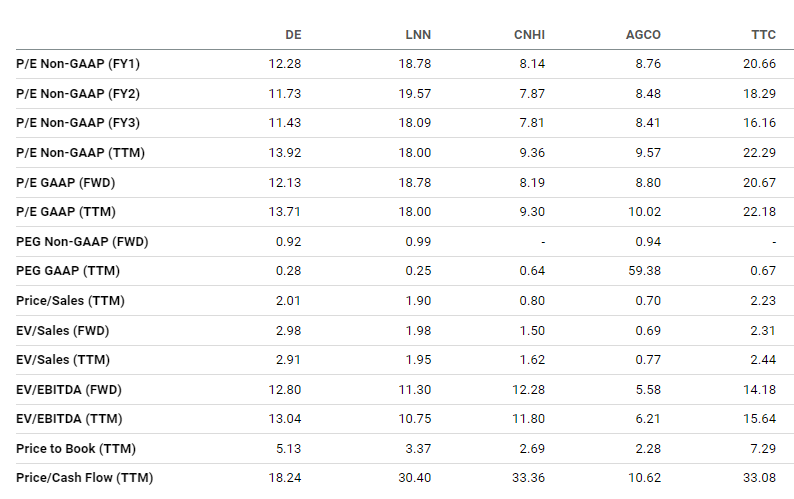

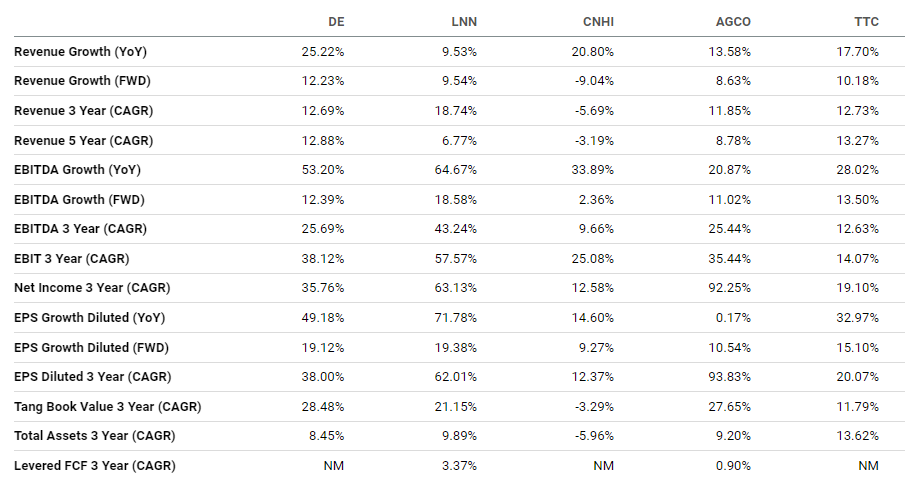

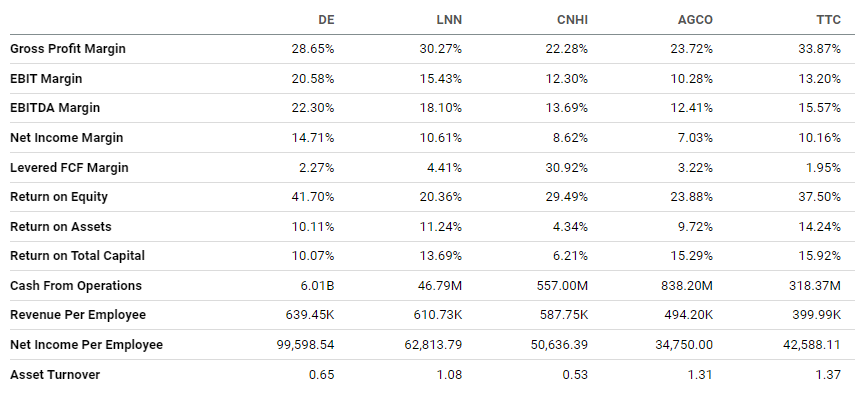

The U.S. is set to produce about 350 million metric tons of corn this year, making it far and away the world’s top producer of the crop. In fact, it’s one of the top three agricultural producers in the world. So it’s no surprise Illinois-based agricultural equipment giant Deere & Company (DE) derives more than half its revenues from customers at home. Despite inflationary pressures, the company has improved gross margins over the last five years. Financial pros are always searching for this portfolio-staple stock. But the market pullback brought more big-money eyeballs, according to our proprietary Trackstar search database. And even with the stock up more than 150% since 2019, it’s surprisingly cheap. Let’s dive deeper… Deere’s Business No other company in the world produces more agricultural equipment than Deere. The iconic green and yellow brand has been manufacturing and servicing agricultural and farming equipment since 1837. Deere orders are fully booked through Q4 of this year, reflecting growing agricultural needs, including strong demand to replace aging equipment. U.S. and Canadian sales are expected to bloom 12.5% in construction and forestry this year. Agricultural sales should eclipse that by rising a whopping 20%. The only drawback is Asian sales, which are forecasted to decline slightly in 2023. Financials Source: Stock Analysis Deere has grown remarkably since 2017, achieving double-digit sales gains in all but two years. Last year, it grew sales 19.4% and had an equally impressive 14.7% profit margin, its highest in decades. This is largely due to Deere’s massive improvement in expenditures and gross margins. Interestingly, the company has very little debt relative to its sales and cash flow, allowing it to maintain a 1.4% dividend yield and a decent share buyback program. Valuation Source: Seeking Alpha DE isn’t the cheapest among its peers, trading at 13.9x trailing earnings and 12.1x forward earnings. But it’s the second-cheapest in terms of price-to-cash-flow ratio and price-to-earnings-growth (PEG) ratio. Growth Source: Seeking Alpha Deere’s premium comes from its remarkable growth relative to its competitors, its forward outlook, and as you’ll see below, its profitability. Its 12.2% expected sales growth next year is best in class. And its EBITDA and EBIT growth over the last three years are impressive even if they’re not the top of this list. Profitability Source: Seeking Alpha Deere’s profitability is better than any of its peers’ except in gross margins, and only barely. The company boasts the best return on equity and the best net income margin by a mile.

Our Opinion 9/10 While Deere could get a little cheaper from here, it currently trades at a nice discount ($377.33 a share). We think it’s fundamentally better than its competitors in the aggregate, with better brand recognition, scale, and capability to maintain its margins. We can clearly see why financial pros love this stock. |

|

News & Insights |

Just Spilled |

|

Want to get content like this directly to your inbox? Then we urge you to sign up for our newsletter here |