|

Proprietary Data Insights Financial Pros’ Top Airline Stock Searches in the Last Month

|

|||||||||||||||||||||

#2 Airline → #1 Pick |

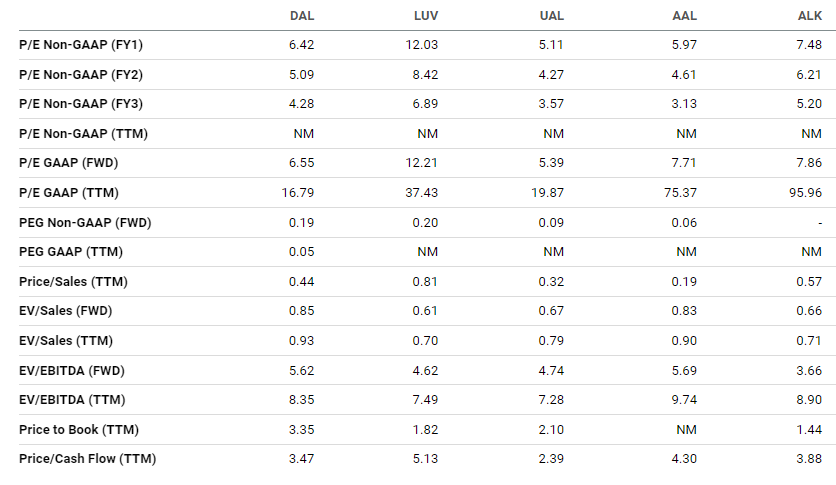

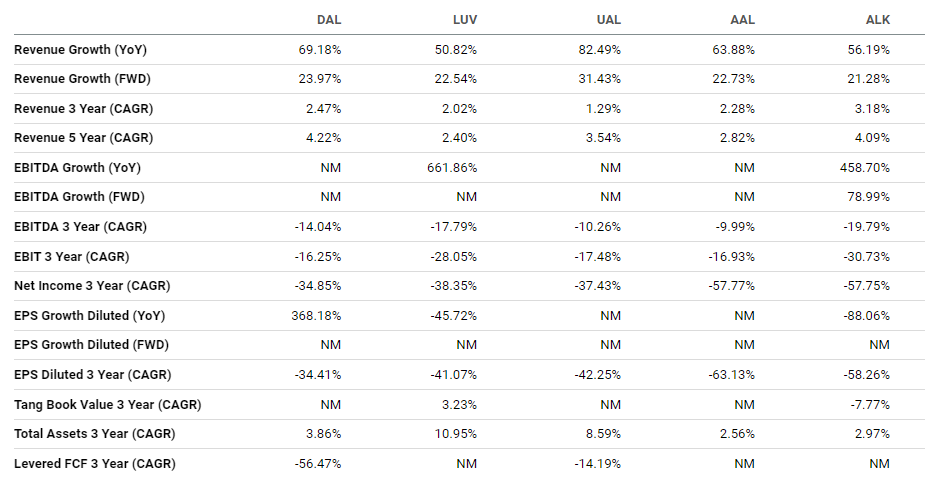

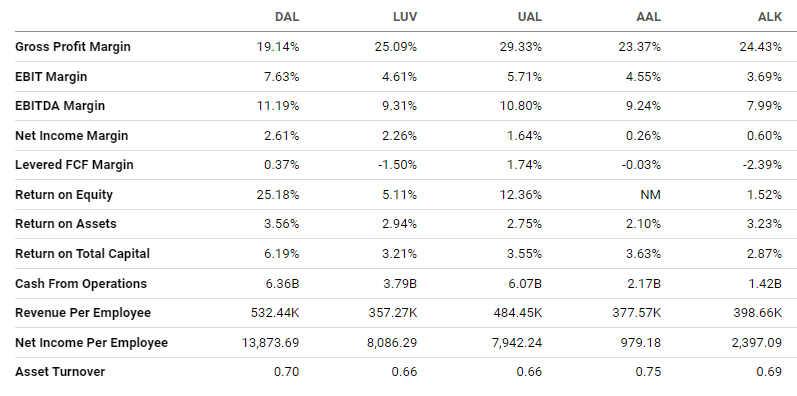

For as long as we can remember, United Airlines (UAL) played second fiddle to Delta Air Lines (DAL). United’s service was lousy, timeliness was terrible, and operations cost more than its rivals’. This month is the first time in years that financial pro search volume put United so close to Delta without earnings in the mix, as United doesn’t report until April 18. As we dug in, we expected United would prove to be the poor investment it always had been… We were wrong. United Airlines’ Business United is based in Chicago. It’s the third-largest airline in the world by revenue behind Delta and American Airlines (AAL). United boasts a fleet of 732 owned and 136 leased aircraft with an average age of 16.7 years. It expects that to grow by 149 planes in 2023 and another 127 in 2024. These planes service 79 domestic destinations and 111 international destinations in 74 countries. Financials Source: Stock Analysis As with all airlines, the pandemic decimated United’s business. Total revenues finally recovered to pre-pandemic levels even though United has moved fewer passengers fewer miles in 2022 than in 2019. This largely speaks to the higher prices consumers are paying. Margins have also recovered but are still lower than their historical averages. Part of what’s hurting the company is the jump in interest expenses from $646 million in 2019 to over $1.67 billion in 2022. As you can imagine, long-term debt skyrocketed from $13.1 billion in 2019 to $28.3 billion by 2022, though it’s down slightly from $30.4 billion in 2021. That brought United’s debt-to-EBITDA ratio up from 1.7x in 2019 to 2.6x in 2022. Delta’s is 1.3x. But United’s paying off around $3 to $4 billion in debt per year. Valuation Source: Seeking Alpha Excess leverage is likely why United is discounted relative to its peers. It trades at the lowest price-to-cash-flow ratio and price-to-earnings ratio, and the second-cheapest price-to-sales ratio. Historically, that makes UAL a pretty good deal. Growth Source: Seeking Alpha As we said, United’s revenue growth came back strong in 2022. And it expects revenues to grow another 31% this year. The real question is whether the company can keep cash flow this strong. Profitability Source: Seeking Alpha To that end, United has the best gross and second-best EBIT margins, plus the top returns on assets, equity, and total capital. And it’s pulling in the most cash from operations, which is key to its future. Our Opinion 8/10 From a risk/reward perspective, UAL isn’t a bad bet. It’s extremely cheap and currently making the right moves to improve its balance sheet. Shares trade at the same price they did nearly 15 years ago. We like the stock as a small speculative play. |

|

News & Insights |

Just Spilled |

|

Want to get content like this directly to your inbox? Then we urge you to sign up for our newsletter here |