|

Proprietary Data Insights Financial Pros’ Top Processed Meat Stock Searches in the Last Month

|

|||||||||||||||||||||

The 10/10 Stock That’s Lost Search Interest |

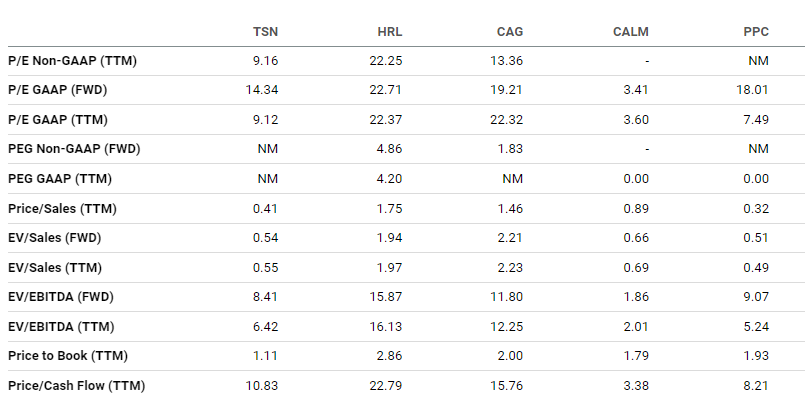

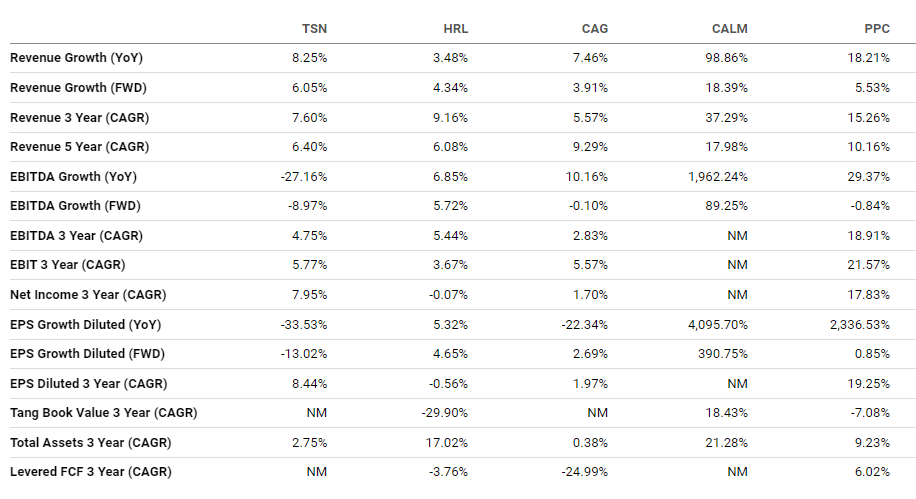

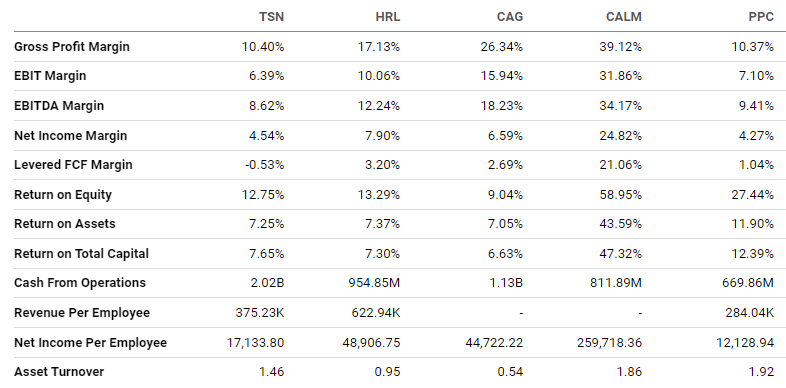

Beef prices have risen an average of 3.75% annually in the last century. Since 2019, that’s skyrocketed to 5.72% compared to broader inflation of 4.13%. That sounds bad. But it’s been worse for Tyson Foods (TSN). After a banner 2021, the company got smoked by higher cattle costs, which accounted for almost half its YoY operating income decline. Chicken and pork profits also fell $175 million and $55 million last year, respectively. While we scour our Trackstar search data for notable jumps in interest, declines also catch our attention. And over the last month or so, financial pros have stopped looking at Tyson. Now, forecasters expect cattle, chicken, and pork prices to drop in the coming months. That’s put Tyson at an incredibly cheap valuation too good to ignore. Tyson Foods’ Business Founded in 1935, Tyson Foods is one of the world’s largest food companies and top protein producers. Its brands include Jimmy Dean and Hillshire Farm. It’s one of the “big four” companies that produce 55% to 85% of the beef, pork, and chicken in the U.S., along with JBS, National Beef, and Cargill. Financials Source: Stock Analysis Tyson’s done great at improving top-line results above typical packaged foods companies every year. 2021 was incredible for Tyson, as the company with typically tight margins improved operating margin by 2.4% and profit margin by nearly 1.7%. That might not sound like much, but it’s a golden era for a food processor. Tyson now faces tighter cattle supply against strong beef demand. While droughts have shrunk herds, current prices are similar to 2014’s, when unsustainably high cattle prices plunged. Valuation Source: Seeking Alpha Tyson trades at just 9.1x trailing 12-month earnings and 14.3x forward earnings. That’s better than its closest peers save for Cal-Maine (CALM), which is a bit different, as it produces egg products. Additionally, TSN’s price-to-sales ratio of 0.4x is historically low, and its price-to-cash-flow ratio of 10.8x and forward price-to-cash-flow ratio of 8.7x are pretty compelling. Growth Source: Seeking Alpha Tyson’s export business has helped the company drive more volume than domestic growth provides. That’s kept revenue growth north of 5% most years, including this year’s forecast. We think forward-looking earnings drops are overstated should cattle prices decline. Profitability Source: Seeking Alpha Tyson has a respectable gross margin given the size and scope of its business. Net income margins have suffered due to inflation. But we expect them to improve as cattle costs fall. Our Opinion 10/10 We love the risk/reward on TSN. First, you get a 3% dividend while you wait. Second, the company has initiatives set to save hundreds of millions of dollars through automated operations. Lastly, and most importantly, should input costs drop, current profit forecasts are far too low. |

|

Want to get content like this directly to your inbox? Then we urge you to sign up for our newsletter here |