Editor’s Note |

It’s Friday. Time to give you a stock pick from our sister newsletter, The Spill, so you can think about it over the weekend and maybe make a move Monday morning. While The Juice helps you be better with money across the board, The Spill focuses on stocks financial pros are researching and judges how good of buys they are. If you’re already sold, you can sign up for The Spill – for free – here. |

|

Proprietary Data Insights Financial Pros’ Top Mortgage REIT Searches in the Last Month

|

|||||||||||||||||||||

15.5% Dividends? |

|

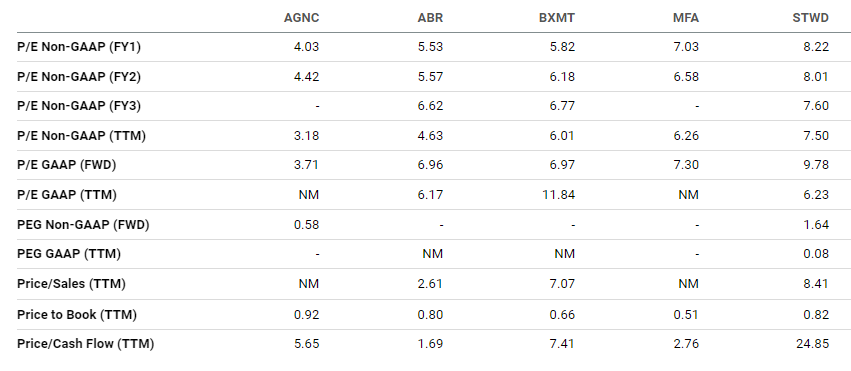

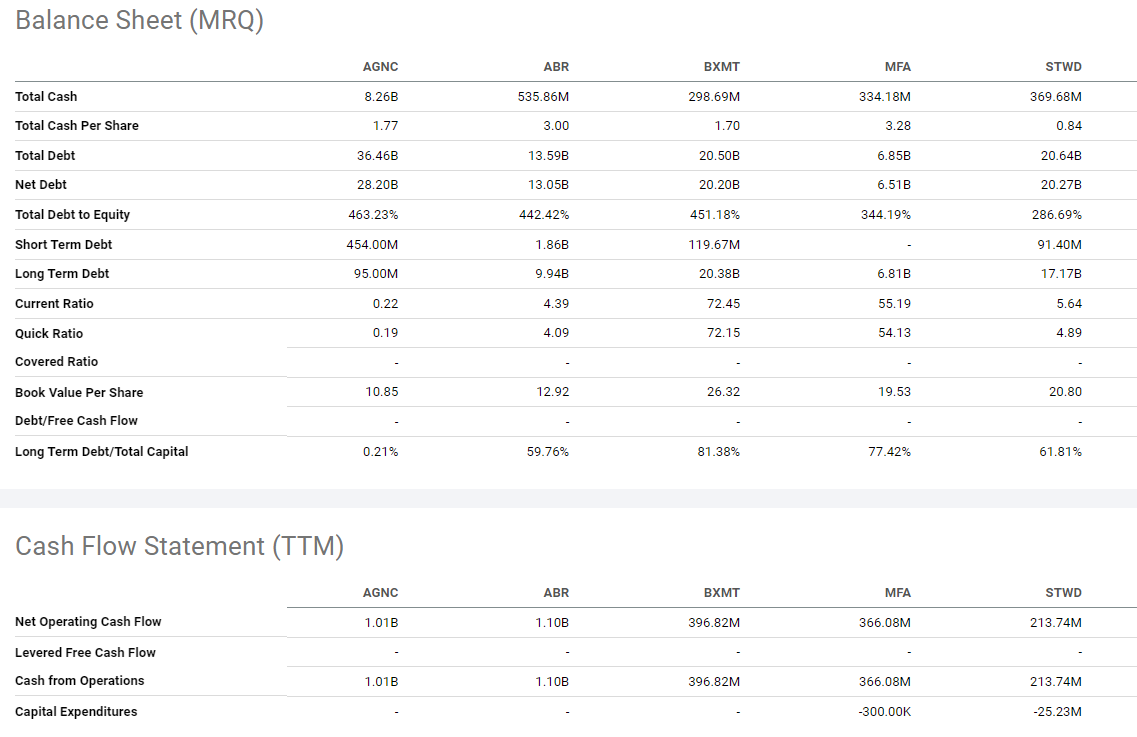

We can’t think of anything more precarious than trying to pick the bottom in the bond market. After all, the Fed hasn’t said it plans to stop raising interest rates. But a looming recession and regional banking trouble could force its hand. Should that happen, mortgage real estate investment trusts (REITs) could benefit handsomely. No joke, the average dividend yield among financial pros’ top five mortgage REIT stock searches, according to our Trackstar database, is north of 14%. That might be more stable than it sounds. So today, out of the top five searches, we’re focusing on the one with the best valuation metrics and debt profile: Arbor Realty Trust (ABR). Arbor Realty Trust’s Business REITs are special entities that don’t pay corporate taxes so long as they pass along 90%+ of their profits to shareholders. That’s why they pay juicy dividends. Many of these companies borrow heavily to employ leverage. Arbor is different from most mortgage REITs, which typically own just a bunch of mortgage-backed securities. It provides loans and origination services to multifamily and single-family rental portfolios as well as other diverse commercial real estate assets, giving it multiple revenue streams. ABR’s mixed portfolio balances across multiple product lines, including holding multifamily loans on its books and servicing Fannie Mae loans. Note that a short-selling outfit called “NINGI Research” recently published a hit piece on Arbor. But its claims are without merit and lack a fundamental understanding of Arbor’s business model. A good example of why this hit piece is misguided: It claims Arbor’s loans vanished from its balance sheet overnight. They didn’t. They simply converted from one loan to another. As many companies have done, ABR took bridge loans, short-term debt, and moved them to agency loans, mortgages on multifamily properties backed by Fannie or Freddie Mac. Financials Source: Stock Analysis Arbor has steadily increased revenues, boasting double-digit year-over-year growth most of the last decade. Plus, it’s improved operating and profit margins as well as free cash flow over that same period. Last quarter, Arbor reported $14.3 billion in loans and lease receivables, a massive increase over its $4.0 billion in 2019. It carries $13.5 billion in debt obligations. Valuation Source: Seeking Alpha Typical valuation measures aren’t as meaningful. Price-to-book ratio can signify what a stock’s price assumes loans or underlying assets are worth. Currently, all the REITs we compared trade below 1.0x on this measure, meaning they’re at a discount to fair value. Although Arbor’s price-to-book isn’t the lowest, it’s pretty cheap. Plus, it trades at one of the deepest price-to-cash-flow ratio discounts. Dividend Yield Source: Seeking Alpha Investors buy REITs for the income they produce. Of the REITs we compared, ABR has the most years of consecutive dividend growth as well as solid three- and five-year average annual dividend growth. It currently yields 15.5%. Debt & Cash Source: Seeking Alpha A REIT’s ability to pay its shareholders is a function of its debt and credit risk management. All the companies we compared have similar total debt-to-equity ratios. But we like ABR’s lower net debt. And ABR produces the best operating cash flow.

Our Opinion 10/10 Arbor Realty Trust consistently delivers stellar growth with a diversified portfolio. Even with higher interest rates, it keeps its average maturity at around 20 months, meaning any poor results won’t last long. We like ABR as a long-term hold so long as management keeps up its performance. To get content like this daily, sign up for The Spill for free here. |

Freshly Squeezed |

|

|

Want to get content like this directly to your inbox? Then we urge you to sign up for our newsletter here |