|

Proprietary Data Insights Financial Pros’ Top Rental & Leasing Services Stock Searches in the Last Month

|

|||||||||||||||||||||

Unpacking Potential: Is U-Haul’s Stock a Value or a Trap? |

|

2020 was an odd year for rental and leasing companies. While Hertz (HTZ) declared bankruptcy, AMERCO (UHAL) saw revenues jump 14.2% We noticed financial pros bottom fishing in the group last week after months of shunning the industry. Their top pick, UHAL, trades at a paltry 6.0x operating cash. Yet, the company pays no dividends, generates no free cash flow, and net debt continues to climb…. …which made us wonder whether UHAL was a steal or a value trap. U-Haul’s Business Anyone who’s relocated cross-country or helped a friend move apartments probably has experience renting the orange and white truck. U-Haul is a leading provider of moving and self-storage services in the United States and Canada. The company has over 48,000 locations in North America and over 1 million trucks and trailers in its fleet. Its business breaks down into three segments:

Surprised the company also provides life insurance? We were too. Remember how we wondered where all the cash went? Investments into the blossoming self-storage segment. The segment saw an admirable 21% revenue growth in FY 2023, albeit slightly decelerating from the impressive 29% in FY 2022. Looking forward, in FY 2024, the team sets its sights on bolstering investments in the self-storage division through finalizing ongoing projects, securing new locations, and launching fresh development initiatives. Financials

Source: Stock Analysis U-Haul grew yearly revenues for the past decade, with its largest pump coming after the pandemic. Margins declined initially during that same period before rebounding to pre pandemic levels. The company’s CAPEX outstripped operating cash flow by $1 billion last year and $200 million the year before. In fact, there was only one year in the last decade where operating cash flow was greater than CAPEX. But it’s not like the company gets nothing for that money. Its tangible book value climbed from $2.8 billion in 2017 to $6.7 billion in the latest report. And with retained earnings climbing similarly, we know that the majority of the money is tied up in hard assets. Valuation

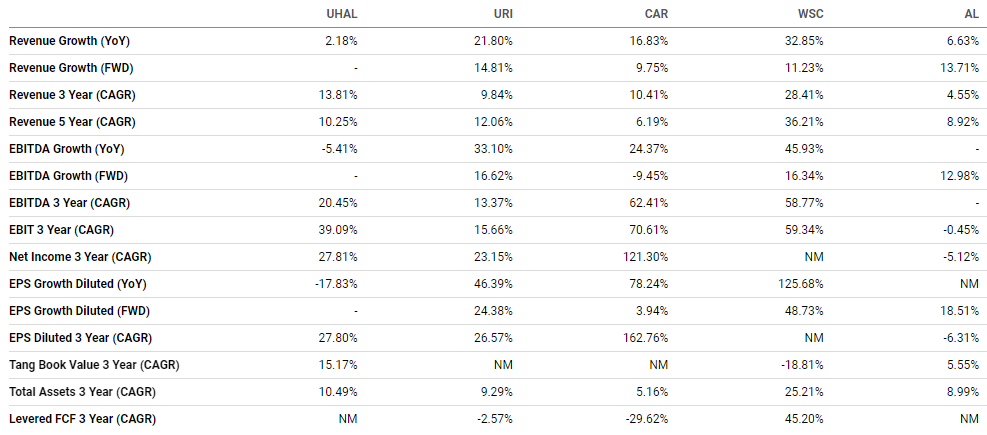

Source: Seeking Alpha As mentioned earlier, UHAL trades at a cheap 6.0x cash. However, so does rival United Rentals (URI), which rents equipment used more for construction and business. And car rental company Avis (CAR) trades at just 2.0x cash. UHAL is cheap on a P/E, Price-to-sales, and price-to-cash basis. However, so is most of the industry. Growth Source: Seeking Alpha Currently, there aren’t listed estimates for forward revenue growth. And YoY growth slowed markedly in the last few months. Comparatively, business-focused rental companies like URI are expected to grow at 14.8% and Willscot (WSC) at 11.2%. Even Air Lease (AL), which rents aircraft, expects double-digit growth next year. Profitability

Source: Seeking Alpha While UHAL runs a good margin, it isn’t at the top. In fact, its gross margins are the worst among its peers. And it’s the only one in the group besides AL not to generate free-cash-flow. Our Opinion 6/10 U-Haul trades at a discount, but not a huge one. It remains to be seen whether its investments will pay off down the road. And right now probably isn’t the best time to invest, especially with interest expenses knocking off 15.5% of operating income. However, if U-Haul trades down towards $40, it becomes a steal. |

|

News & Insights |

Just Spilled |

|

Want to get content like this directly to your inbox? Then we urge you to sign up for our newsletter here |