|

Technology

|

|

Proprietary Data Insights |

Financial Pros’ Top Live Venue Stock Searches in the Last Month |

Has AMC Theaters Finally Bottomed? COVID-19 decimated movie theaters. AMC Entertainment (AMC), one of the largest in the world, flirted with bankruptcy more than once. Somehow, it survived. And today, it could be on the brink of a miraculous turnaround. AMC partnered with Taylor Swift to release her tour experience – a whole new way to bring people to the theater. And it appears to be working. Shows are sold out months in advance with a $100 million projected. That caught the attention of financial pros who began to search for this stock at a blistering pace according to our Trackstar Data. Believe it or not, this could be the final point in a long-awaited turnaround for the movie chain. AMC’s Business With 950 theaters and a whopping 10,500 screens worldwide, AMC is the popcorn-popping top-of-the-line theater chain. Their modern theaters include power-reclining chairs, Coke drink vending machines, and much more. When it comes to the financial score, AMC segments its business into the following areas:

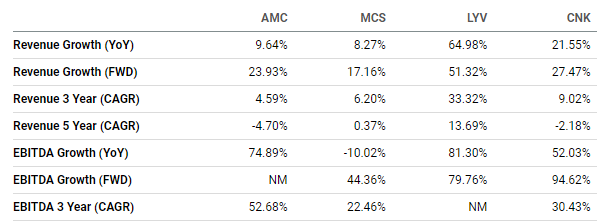

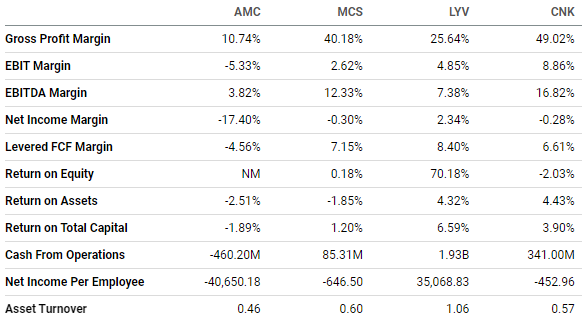

The latest quarterly roundup has AMC surprisingly in the black with a net income of $34 million. While things aren’t exactly the same as the pre-COVID days, this marks their first positive net income since the third quarter of 2019. Operating cash flow was still negative. But at -$13 million, it was VERY close to breakeven. Plus, upcoming blockbusters and a concert film featuring Taylor Swift have investors humming a happier tune. [instorylist_ad] Financials Source: Stock Analysis Revenues are starting to get back to their pre pandemic levels. However, labor and operating costs shot up over the few years. Total debt doubled from $5 billion to over $11 billion during the pandemic. And the company also more than doubled the number of shares outstanding. Plus, more recent news to issue more shares wasn’t well-received. Yet their interest expense hasn’t increased much, only costing them around $350 million per year. So, while their share issuance was dilutive, the stock has the potential to regain some ground, at least if it can improve operations. Valuation Source: Stock Analysis We brought in other movie theater and live entertainment stocks for our comparison. None of them have a respectable trailing P/E ratio. However, Cinemark (CNK) is expecting a decent forward-looking P/E ratio. Plus, all the other chains run a decent price-to-cash flow ratio. Only AMC has yet to get back to that level. Growth Source: Seeking Alpha Interestingly, CNK has the second-best YoY revenue growth, only behind Live Nation (LYV), which put up an impressive 65% growth and expects to do more than 50% growth next year. These aren’t just coming off basement levels. In LYV’s case, it hit $19.2 billion in revenues compared to $11.6 billion prepandemic. But it’s also trading at higher valuations. Still, all expect sizable revenue growth in 2023. Profitability Source: Seeking Alpha Why is it that AMC’s gross margins are still in the dumpster, yet Marcus (MCS) and CNK are doing just fine? We can’t help but blame management for the gap. Our Opinion 4/10 AMC could be in for a huge turnaround…if they were well run. But the comparisons to other chains don’t make the company look good, and the constant share dilution is a reminder that share prices are never safe. We wouldn’t recommend the stock here despite the catalysts.

|

|

Want to get content like this directly to your inbox? Then we urge you to sign up for our newsletter here |