|

Proprietary Data Insights Financial Pros’ Top Consumer Healthcare Stock Searches in the Last Month

|

Do We Still Love This 10/10 Stock? |

So, you thought CVS (CVS) was just that ubiquitous corner pharmacy where you grab toothpaste and pick up Aunt Sally’s medications? Think again. In early March, we rated CVS a 10/10. As the top consumer healthcare stock amongst financial pros, we loved the holistic transformation the company embarked on. Once a simple retail pharmacy chain, CVS aimed to become a fully integrated healthcare provider, acquiring Aetna in 2018 for $70 billion. Yet, the stock has dropped nearly 20% since then as it slid into Q1 earnings and remained there through the present. So, do we stand by our rating? Yes, and here’s why. CVS’ Business CVS embarked on an ambitious plan to branch beyond its pharmacy stores to become a benefits manager and provider. The $70 billion acquisition of Aetna in 2018 was the largest acquisition of that type in history. You can think of CVS as your one-stop shop for everything from prescription drugs to beauty products and healthcare insurance. Fun fact: they cater to a staggering 100 million customers per year, and their mammoth team of 300,000 employees makes it all possible. Today, the company reports in three segments:

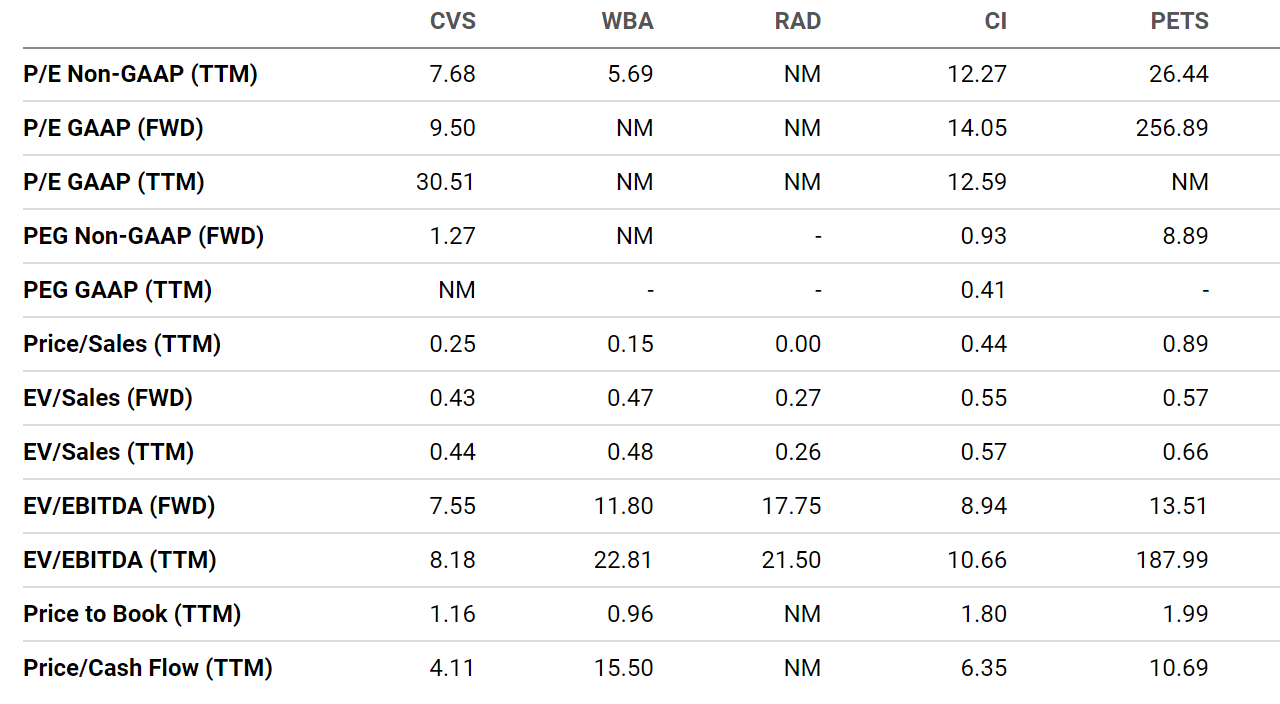

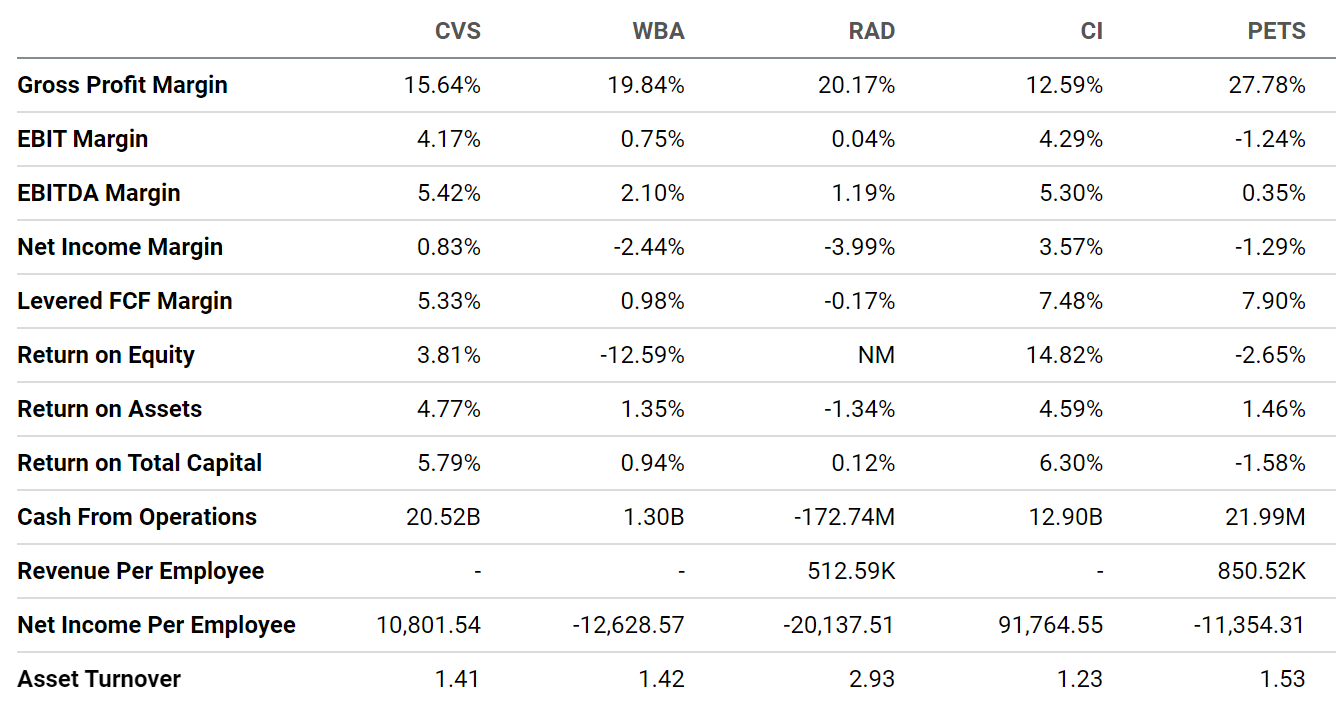

In its Q2 2023 earnings release, CVS achieved net income of $2.8 billion, slightly down from the same period last year but pushed revenues up by 11% to a cool $72.6 billion. The company appears to be struggling with its Medicare, which makes up 25% of its total revenues. Its Q2 utilization rate was higher than expected, driving up costs. Plus, the reimbursement rates are a big question mark going forward. California’s Blue Shield recently dropped CVS as its benefits provider in favor of a new approach to negotiating drug prices directly with manufacturers. Financials Source: Stock Analysis Revenue growth hasn’t been a problem for CVS, especially with its acquisition of Aetna. The focus now is on the margins as gross margins fell over the last few years, taking down operating and profit margins. However, many costs were non-cash as the free-cash-flow margin remained relatively stable. CVS took on a lot of debt to acquire Aetna. And so far, it hasn’t done much to pay down the $80+ billion. That’s a hefty amount, considering they only generate $20 billion in cash from operations annually. And interest runs at a whopping $2.4 billion annually. So, it’s fair to say their cost-cutting measures are needed to alleviate some of the pressures on the bottom line. We do question whether should continue to pay their almost 4% dividend alongside their share repurchase program, which combined cost them almost $7 billion annually. Pushing that back towards debt repayment may be more appropriate. Valuation Source: Stock Analysis We compared CVS to other drug stores such as Walgreens (WBA) as well as health insurer Cigna (CI) to get a blended view. CVS trades at the lowest price-to-cash flow of the group and close to the lowest non-GAAP price-to-earnings ratio. It’s certainly cheap. But is it a value trap? Growth Source: Seeking Alpha Revenue growth is expected to slow dramatically for CVS, dropping below double digits. However, the company is expected to improve its EBITDA and EPS going forward, a positive sign of the ongoing transformation. Only CI is expected to put up decent growth in these same categories going forward. Profitability Source: Seeking Alpha CVS doesn’t have the best gross margin. But its EBIT margin is near the top, as is its free cash flow margin. We’d like to see these improve to become top of the pack within the following year. Our Opinion 10/10 We’re sticking with our call as nothing has materially changed. Transformations of this magnitude take time. And we expect there to be hiccups along the way. However, the long-term outlook for the company remains bullish. Plus, the company has plenty of cash to maneuver when needed. _____________________________________________________________ News & Insights Just Spilled |

|

Want to get content like this directly to your inbox? Then we urge you to sign up for our newsletter here |