|

Proprietary Data Insights Financial Pros’ Top Social Media Stock Searches in the Last Month

|

Financial Pros Question the Limits of META’s Growth |

We covered META back in February of this year and in September 2022, rating it a 7/10 and 8/10, respectively. Shares are up more than 70% since February and over 200% since September. Fears of advertising slowdown and user attrition appeared overblown. Yet, the company faces a new challenge – saturation. Financial pros made this stock the top social media search, focusing on articles related to revenue growth. Over 90% of global social media users have a Facebook account, and 80% in the U.S. How much growth can there be? Is Meta at the mercy of advertising spend or is its moonshot into the Metaverse going to pay off? Meta’s Business Zuckerberg’s social media fortress stems from his dorm room project, Facebook – the flagship app with nearly 3 billion monthly active users. Yet, it’s expanded far beyond as it transforms itself into the next generation of social media and technology. Meta’s operations now include Instagram, Messenger, WhatsApp, and a slew of ad-driven platforms, they’re the life of the digital party. Their newest venture, Reality Labs, dives into AR/VR hardware, software, and Metaverse content. Meta segments its business into the following areas:

Source: META Q2 2023 Investor Relations 2022 was a rough year for the company as it experienced its first total user decline in its history. That’s on top of ad revenue falling. Both have rebounded. Yet, Zuckerberg is aware Facebook’s maturity means he’ll need to dig for gold elsewhere. It’s also not clear when Reality Labs will turn a profit. Zuckerberg said he plans to spend $10-$15 billion a year on the segment. Revenues continue to rise for the segment as costs decline, a very positive sign. Financials Source: Stock Analysis With a rebound in advertising spend, Meta’s revenues climbed well past their highs in 2021 and are expected to keep climbing. However, they will likely be in the single digits as Meta hits a user saturation point and consumer spending declines. While the operating margin declined in 2022, the cuts to overhead brought it back to a healthy 31.8% in the latest quarter. Although total debt sits at $37 billion, Meta has $53.5 billion in cash, more than enough to cover its debts. While the company doesn’t pay a dividend, it’s spent $81.5 billion buying back stock in 2021 and 2022, a 10% total yield.

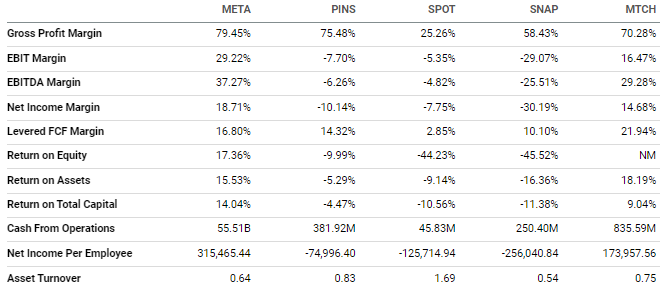

Valuation Source: Seeking Alpha Compared to its peers, Meta is a steal, except for maybe Match Group (MTCH). It trades at a lower P/E and price-to-cash ratio. You could argue Meta’s price-to-sales ratio is a bit high. But that’s largely because it’s profitable. Growth Source: Seeking Alpha Social media companies didn’t see much advertising spend this year. And most don’t expect much growth in 2023-2024. The fact that Meta’s forward growth numbers aren’t much lower than peers like Pinterest (PINS) and Snap (SNAP) says a lot about the user and advertising growth problems facing the industry. Profitability Source: Seeking Alpha Meta’s margins dominate its peers by a mile, helping it deliver above-average returns on equity, assets, and total capital. However, it’s worth noting the free cash flow margins for PINS and MTCH aren’t too shabby. Our Opinion 6/10 Although shares have tripled since September 2022, shares appear fairly valued to trading at a slight discount. However, we see revenue headwinds that make shares far less attractive than in February. Our slight downgrade in rating reflects a cautious revenue outlook in 2023, extending into 2024 |

|

Want to get content like this directly to your inbox? Then we urge you to sign up for our newsletter here |