Earlier:

• Summary for Week Ending Nov 23rd

Negotiations concerning the “fiscal slope” in the US will be back in the headlines this week. And, in Europe, the discussion on funding for Greece will resume on Monday.

There are two key housing reports this week: Case-Shiller house prices on Tuesday, and New Home Sales on Wednesday.

Revised Q3 GDP will be released on Thursday, and the October Personal Income and Outlays report will be released on Friday.

For manufacturing, three regional manufacturing reports will be released (Richmond, Dallas and Kansas City Fed surveys), plus the Chicago PMI will be released Friday.

The NY Fed will release their Q3 Report on Household Debt and Credit on Tuesday, and the FDIC is expected to release the Q3 Quarterly Banking Profile this week.

—– Monday, Nov 26th —–

8:30 AM ET: Chicago Fed National Activity Index for October. This is a composite index of other data.

10:30 AM: Dallas Fed Manufacturing Survey for November. The consensus is for 4.7 for the general business activity index, up from 1.8 in September.

Expected: LPS “First Look” Mortgage Delinquency Survey for October.

—– Tuesday, Nov 27th —–

8:30 AM: Durable Goods Orders for October from the Census Bureau. The consensus is for a 0.8% decrease in durable goods orders.

9:00 AM: S&P/Case-Shiller House Price Index for September. Although this is the September report, it is really a 3 month average of July, August and September.

9:00 AM: S&P/Case-Shiller House Price Index for September. Although this is the September report, it is really a 3 month average of July, August and September.

This graph shows the nominal seasonally adjusted Composite 10 and Composite 20 indexes through August 2012 (the Composite 20 was started in January 2000).

The consensus is for a 2.9% year-over-year increase in the Composite 20 index (NSA) for September. The Zillow forecast is for the Composite 20 to increase 3.0% year-over-year, and for prices to increase 0.4% month-to-month seasonally adjusted.

10:00 AM: Richmond Fed Survey of Manufacturing Activity for November. The consensus is for a decrease to -8 for this survey from -7 in October (below zero is contraction).

10:00 AM: FHFA House Price Index for September 2012. This is based on GSE repeat sales and is no longer as closely followed as Case-Shiller (or CoreLogic). The consensus is for a 0.5% increase in house prices.

10:00 AM: Conference Board’s consumer confidence index for November. The consensus is for an increase to 72.8 from 72.2 last month.

3:00 PM: New York Fed to Release Q3 Report on Household Debt and Credit

—– Wednesday, Nov 28th —–

7:00 AM: The Mortgage Bankers Association (MBA) will release the mortgage purchase applications index.

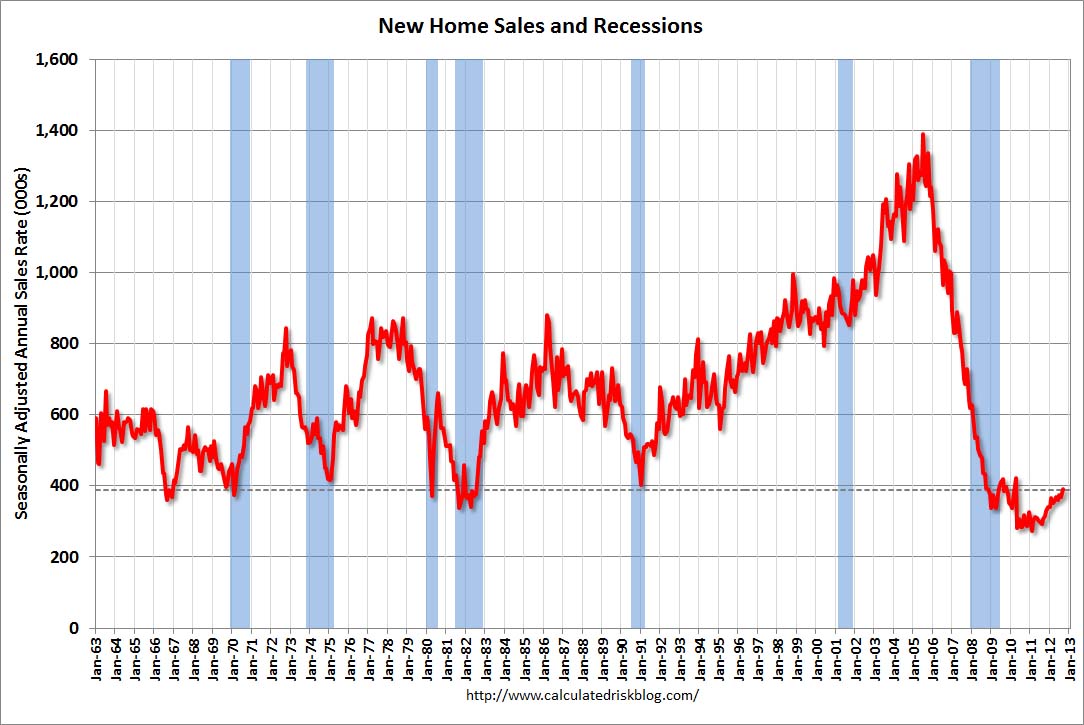

10:00 AM ET: New Home Sales for October from the Census Bureau.

10:00 AM ET: New Home Sales for October from the Census Bureau.

This graph shows New Home Sales since 1963. The dashed line is the September sales rate.

The consensus is for a decrease in sales to 387 thousand Seasonally Adjusted Annual Rate (SAAR) in October from 389 thousand in September.

2:00 PM: Federal Reserve Beige Book, an informal review by the Federal Reserve Banks of current economic conditions in their Districts. This might show some slight improvement. Some analysts will be looking for concerns about Europe or the “fiscal cliff”.

—– Thursday, Nov 29th —–

8:30 AM: The initial weekly unemployment claims report will be released. The consensus is for claims to decrease to 390 thousand from 410 thousand.

8:30 AM: Q3 GDP (second release). This is the second release from the BEA. The consensus is that real GDP increased 2.8% annualized in Q3, revised up from 2.0% in the advance release.

10:00 AM ET: Pending Home Sales Index for October. The consensus is for a 1.0% increase in the index.

11:00 AM: Kansas City Fed regional Manufacturing Survey for November. The consensus is for an a reading of -1, up from -4 in October (below zero is contraction).

—– Friday, Nov 30th —–

8:30 AM ET: Personal Income and Outlays for October. The consensus is for a 0.3% increase in personal income in October, and for 0.1% increase in personal spending. And for the Core PCE price index to increase 0.2%.

9:45 AM: Chicago Purchasing Managers Index for November. The consensus is for an increase to 50.3, up from 49.9 in October.