By request, here is an update to four key indicators used by the NBER for business cycle dating: GDP, Employment, Industrial production and real personal income less transfer payments.

Note: The following graphs are all constructed as a percent of the peak in each indicator. This shows when the indicator has bottomed – and when the indicator has returned to the level of the previous peak. If the indicator is at a new peak, the value is 100%.

These graphs show that some major indicators are still significantly below the pre-recession peaks.

Click on graph for larger image.

Click on graph for larger image.

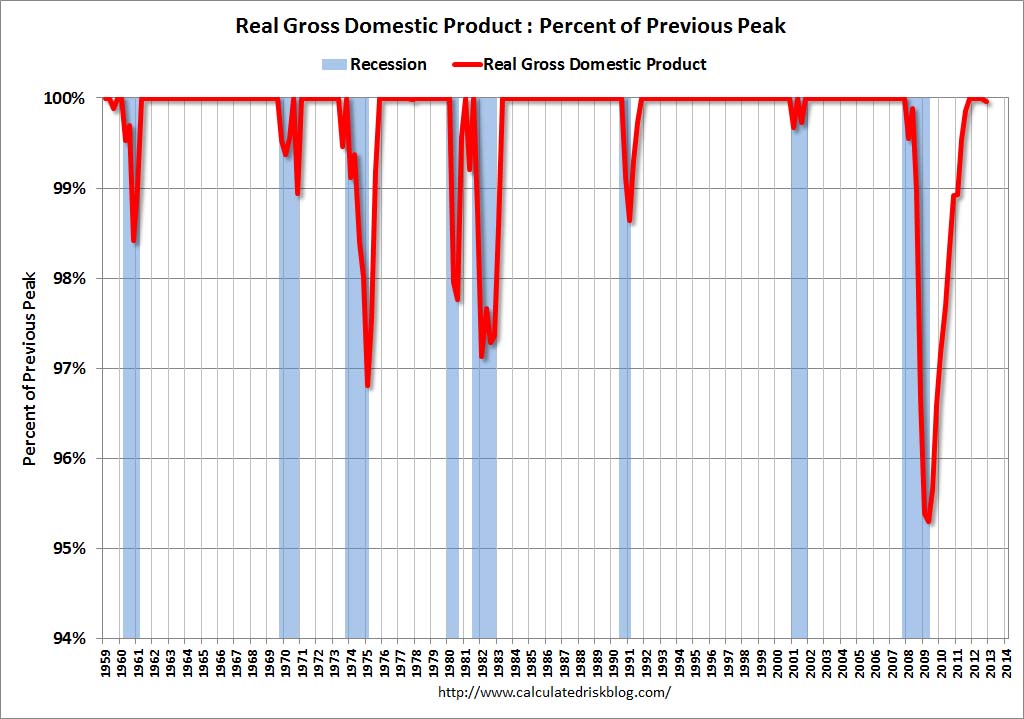

This graph is for real GDP through Q4 2012.

Real GDP returned to the pre-recession peak in Q4 2011, and hit new post-recession highs for four consecutive quarters until dipping slightly in Q4 2012 (Q4 GDP will probably be revised up).

At the worst point – in Q2 2009 – real GDP was off 4.7% from the 2007 peak.

Real GDP has performed better than other indicators …

Real GDP has performed better than other indicators …

This graph shows real personal income less transfer payments as a percent of the previous peak through the December report.

This measure was off 11.2% at the trough in October 2009.

Real personal income less transfer payments returned to the pre-recession peak in December, but that was due to a one time surge in income as some high income earners accelerated earnings to avoid higher taxes in 2013. Without that distortion, real personal income less transfer payments would probably still be 2.5% or so below the previous peak.

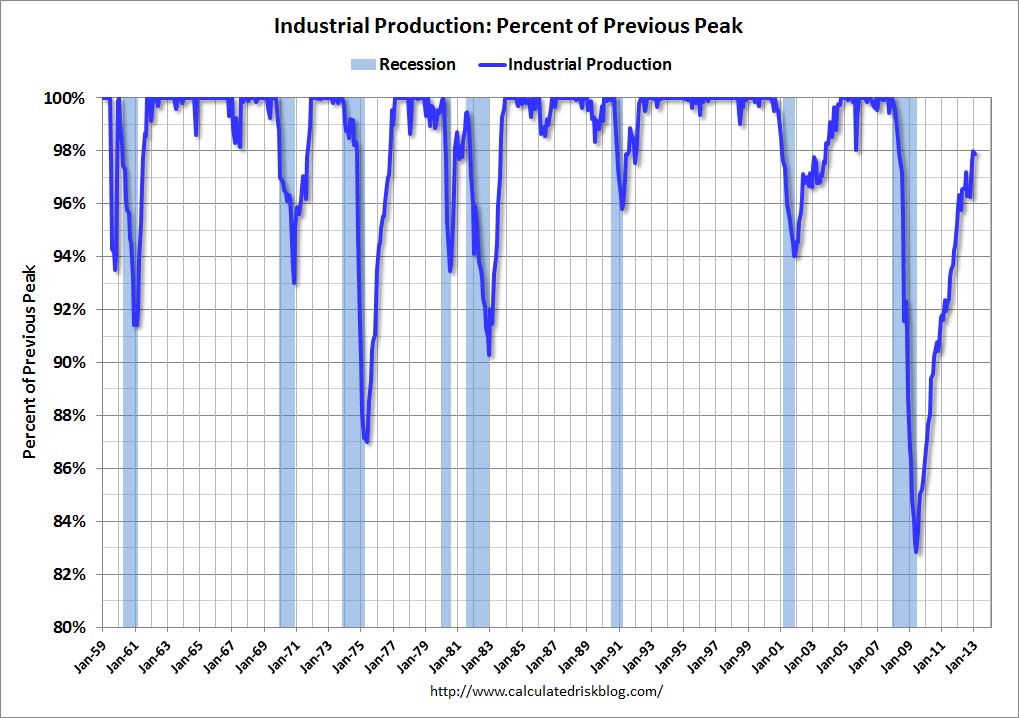

The third graph is for industrial production through January 2013.

The third graph is for industrial production through January 2013.

Industrial production was off over 17% at the trough in June 2009, and has been one of the stronger performing sectors during the recovery.

However industrial production is still 2.1% below the pre-recession peak. This indicator will probably return to the pre-recession peak in 2013.

The final graph is for employment and is through January 2013. This is similar to the graph I post every month comparing percent payroll jobs lost in several recessions.

The final graph is for employment and is through January 2013. This is similar to the graph I post every month comparing percent payroll jobs lost in several recessions.

Payroll employment is still 2.3% below the pre-recession peak.

All of these indicators collapsed in 2008 and early 2009, and only real GDP is back to the pre-recession peak (personal income was due to a one time increase in income and will be back below the pre-recession peak in January). At the current pace of improvement, industrial production will be back to the pre-recession peak later this year, personal income less transfer payments late in 2013, and employment in late 2014.