After the system was finished, we decided to register the trades officially at a tracking service and trade it live. It was our belief that the system was worth offering for subscription or had additional value beyond the money we could make trading it. Both of us had day jobs, and we fairly quickly realized that trading the close was difficult for both of us, for two reasons. The first reason is that for those of us who trade and work, Murphy’s Law ensures that whenever there is a big trade that needs to be made, work will interfere. The second reason is that systems that rely on binary buy or sell signals sometimes flip-flop or hover near the threshold. If it is 3:39 and the trade has to be entered by 3:40 for a market-on-close order and it is flip-flopping between buy, hold, and sell, making the correct trade can be a challenge. Couple this second reason with the first reason and we eventually decided to stop tracking the system and trading it live.

If I remember correctly (it has been a little over 4 years), we also weren’t sure if the system would continue working.

We can now look back and see that the system did indeed endure through a rough patch in 2009 and 2010. I believe the character of the market changed after the crash of 2008, and 2009 and 2010 saw a return to a market that wanted to trend. The S&P 500 returned better than 20% in 2009 and over 10% in 2010. The mean reversion system managed to squeeze out 10% in 2009 and was flat in 2010.

Based on this performance, and the flailing performance of other similar systems, it was easy to write mean reversion off as being dead.

My friend and partner went our separate ways, and have not worked together since.

I have not forgotten about this system, and continue to watch it. Consider that it now has better than 4 years of out-of-sample trades. So how has it been performing? I guess the title of this post gives it away…

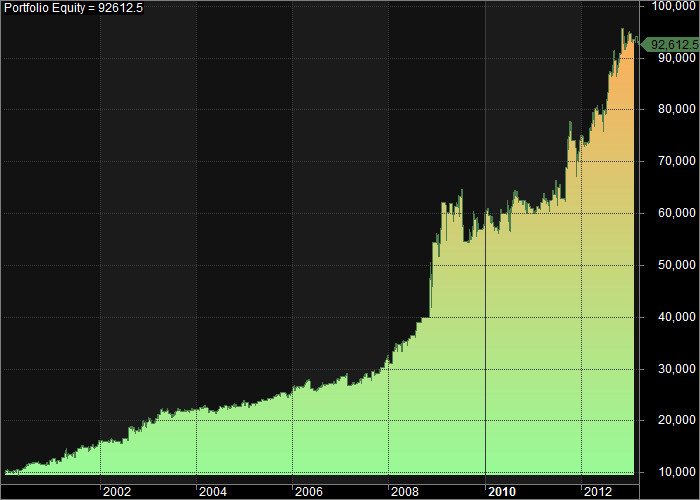

Let’s look at the equity curve for the long/short version. The system uses leverage for any trade that is with the trend. For example, if a dip is being bought and the trend is up, then 2x leverage is used.

That equity curve shows a system with an annualized return of 18.35%, including .005/share for commissions. In 2011 it returned 24.3%.

The equity curve clearly shows where mean reversion peaked in 2008 and where it took a 2 year cooling-off period in 2009 and 2010.

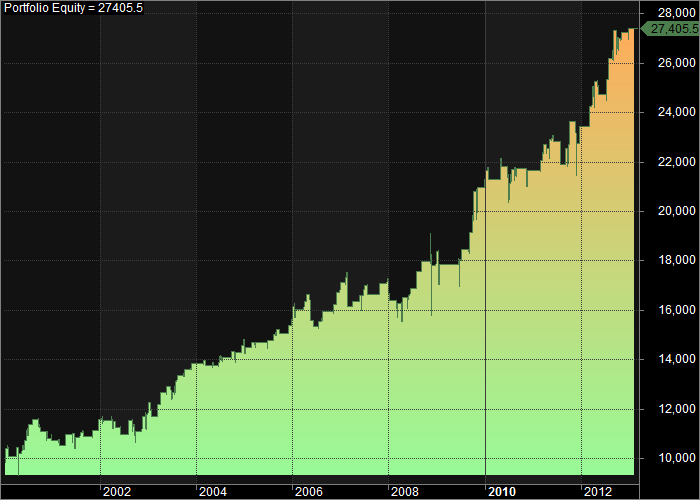

Now let’s look at the long-only version, still using leverage.

This equity curve shows a system with an annualized return of 7.93%, including .005/share for commissions. It has beat the S&P 500 in both 2011 and 2012 with about half the maximum drawdown of the S&P. Time in the market (exposure) is only 11%.

I will likely get deeper into the system stats in a later post.

For now, it seems ridiculous to me that I’m not trading a version of this system. This speaks to the difficulty in system trading as the rules must be adhered to even during long periods of under-performance. There are some important questions I intend to answer in the future. Once I have these answers, I may begin trading it again.

Here are some of the questions:

- Is there a way to accurately place orders for this system while at work?

- Can exposure be increased without significantly increasing drawdowns?

- Can tracking system health be used to in conjunction with the equity curve to improve results?