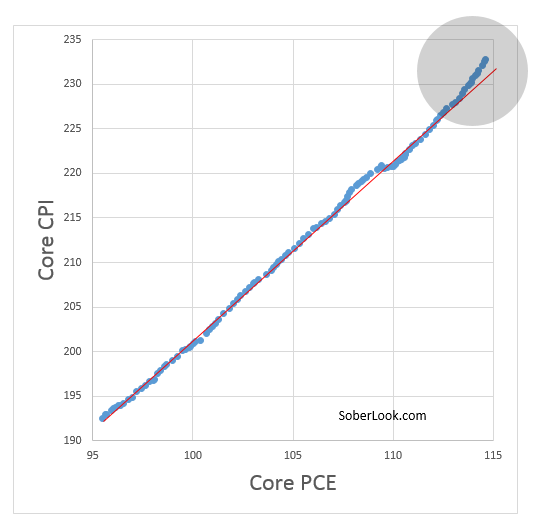

The two major US core inflation indices have diverged. The explanation for this divergence has to do with the difference in relative importance of housing in the indices. And recent increases in the cost of shelter accentuated these differences.

DB: – Shelter prices have been rising at an annual rate of 2.2% in the PCE, well above the overall level of inflation measured by the index. But housing accounts for a much greater share of the core CPI index – around 42% – relative to the 15% share of the core PCE index. The weight effect of housing alone explains around 50 basis points of the annualized inflation differential between the core index, virtually the entire excess amount of observed CPI inflation. The weighting effect of housing prices in core inflation is exaggerated by factor that has little to do with housing. The relative importance of “core” components of CPI inflation has dropped by about 2 percentage points since 2010, while remaining steady in PCE inflation. This has the effect of increasing the relative importance of housing prices in core CPI.

|

|

Core CPI vs PCE compared to line fit |

Given the Fed’s focus on the Core PCE measure – which is lagging behind the CPI – the central bank now has plenty of room to pursue its monetary expansion program. In fact if the PCE growth slows further, some FOMC members may even push to increase securities purchases in order to avoid disinflation. In the mean time, liquidity driven credit markets are moving dangerously close to bubble territory.