Or: “Dudley Makes Mock of the Monetarists.”

In my post The Fed is not “Printing Money.” It’s Retiring Bonds and Issuing Reserves, I said:

…when the Fed gives the banks reserves and retires bonds, it’s taking on market risk/reward, replacing it with absolutely nonvolatile, risk/reward-free assets (at least in nominal terms). It’s removing leverage and volatility from the banking system.

And:

The banking system doesn’t “take money” out of total reserves, or reduce those reserves, to fund loans.

And now I find this in a speech today at the Japan Society by FRBNY President and CEO William Dudley (HT Matthew Klein). Emphasis mine:

…asset purchases work primarily through the asset side of the balance sheet by transferring duration risk from the private sector to the central bank’s balance sheet. This pushes down risk premia, and prompts private sector investors to move into riskier assets. As a result, financial market conditions ease, supporting wealth and aggregate demand. The fact that such purchases increase the amount of reserves in the banking system and the size of the monetary base is a byproduct — not the goal — of these actions.

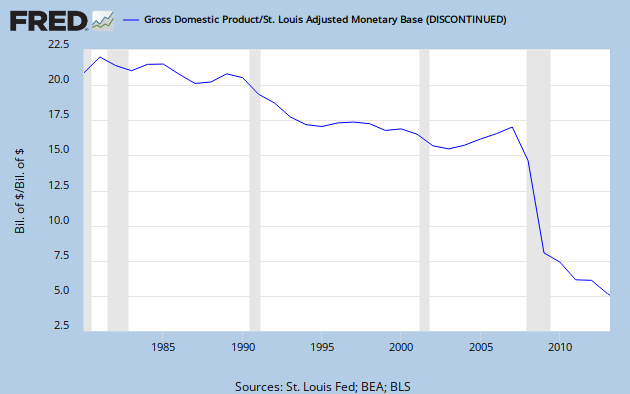

Or to put it another way: when you increase M in MV = PY, the most likely result — the result you have to assume by default absent some convincing story about real-economy incentives, causes, and effects — is a purely arithmetic decline in V (cf. Dudley’s “byproduct”), with zero effect on P or Y.

{kind=link}

This is doubly true if by M you mean the Monetary Base (as monetarists do, inconsistently but often) — the only measure of money that includes reserve balances. Increasing the quantity of reserve balances (hence the monetary base) does not magically increase either P or Y.

Cross-posted at Asymptosis.