By Surly Trader

The Credit Suisse Fear Barometer has dropped like a rock since the beginning of May (see figure 1).

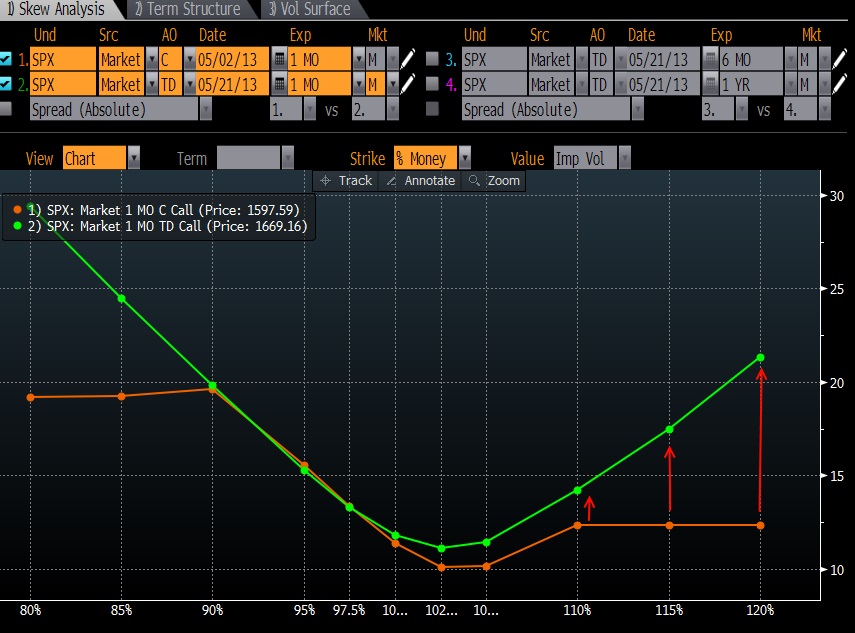

This has little to nothing to do with implied volatility dropping and everything to do with the shape of the implied volatility curve. In this case, the 1 month 10% out of the money call option implied volatility has risen from about 12.4% to 14.4%. This extra 10% out of the money call premium has made 10% out of the money puts more affordable even though the put cost hasn’t changed (see figure 2).

This might get at the renewed sense that we are going to have binary outcomes in the near-term. Either the Fed is going to reinforce its commitment to quantitative easing and the market shoots up OR the Fed is going to hint at a pull-back in quantitative easing and the market is going to fall off a cliff.

This manic behaviour definitely played out today in the S&P 500. When the Fed indicated its commitment, the market shot up in the morning. When the thought sunk in that the Fed might prematurely scale back its purchases, the market pulled back sharply (see figure 3).

Up is down, right is left. Nothing matters except for how long and how much QE is going to be pumped into the system. Economic news only influences traders’ thoughts on whether it will shorten or lengthen the life of quantitative easing. The only thing that can be certain is that before all is said and done, at least one bubble will be inflated and at least one bubble will burst in the aftermath of our central bank experimentation. Japan seems to be a likely and volatile candidate.

(Figure 1)

(Figure 2)

(Figure 3 – 2.3% range doesn’t quite compare with silver but we are getting there)