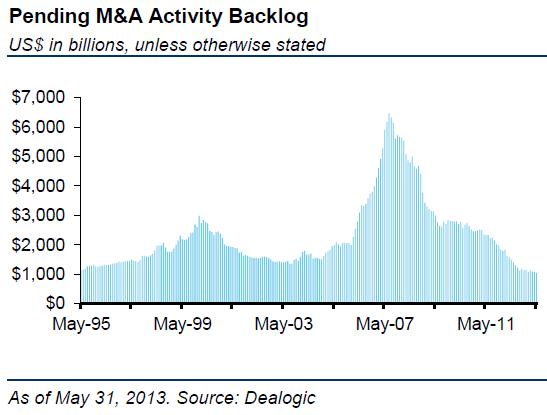

The volume of mergers and acquisitions (M&A) in the US remains anemic. Even the highly anticipated Dell transaction fell through (see WSJ story). In spite of large cash positions on corporate balance sheets, the CEOs are not pulling the trigger. Private equity firms on the other hand are facing declining capacity for large acquisitions (see discussion).

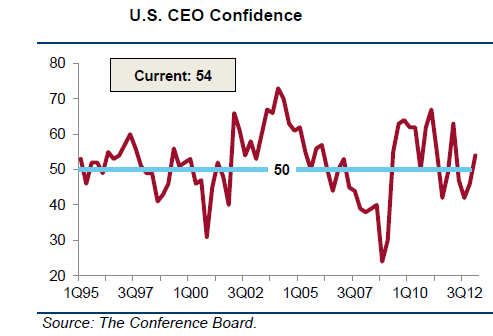

In the past, M&A activity usually followed the equity markets. But why not this time around? After all we’ve seen the equity markets hit new all-time highs recently. The answer has to do with CEO business confidence, which is the ultimate driver of M&A. According to Barclays Capital, “ask the management of any brokerage company what it takes for M&A to increase, and they will tell you it is CEO confidence.” And according to the Conference Board, the US CEO confidence has been subdued.

|

| Source: Barclays Capital |

Investment bankers at Goldman however feel that this could all change for the better soon.

GS: – Global M&A volumes in 2013 represent approximately 4% of global market cap relative to the 20 year average of closer to 7%.

A similar dynamic is evident in equity capital markets. IPOs currently represent 20 basis points of global market cap, which is 50% lower than the 20 year average. Activity has varied across the globe and we have started to see a meaningful pick up in the US new issue market.To the extent the operating environment stabilizes and our clients feel more confident, we believe activity could revert to more normalized levels. If half of the gap was closed relative to 20 year average activity levels, M&A volumes could increase by approximately $700 billion and IPOs could increase by roughly $50 billion.

Those are some impressive numbers. Of course it could be wishful thinking on Goldman’s part, given the firm is still the largest M&A shop and derives a substantial portion of its fee income from these activities. They miss the good old days of the M&A gravy train during 2006 – 2008. For now things don’t look too rosy over the next few months, as the current M&A pipeline (expected deals) has been relatively weak.

|

| Source: Barclay Capital |

If Goldman is right and CEO confidence improves, we may in fact see a pop in activity later this year. But the return to the boom days of 2006 – 2008 period will remain elusive for years to come.

SoberLook.com