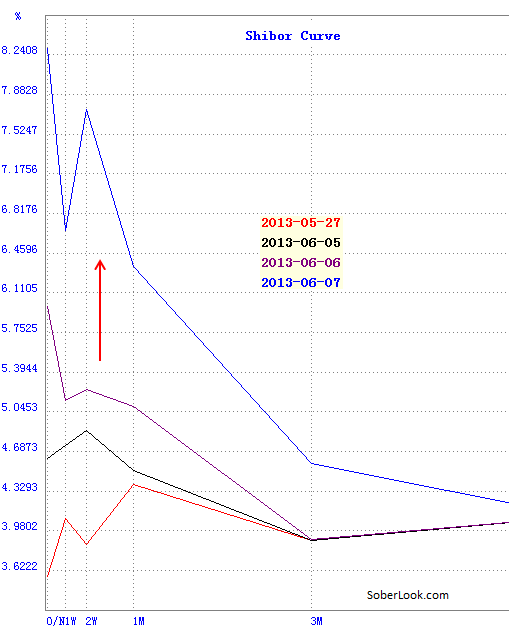

China’s interbank rates have unexpectedly spiked last week as the SHIBOR curve (China’s LIBOR equivalent) became highly inverted. Given that there have been no indications of a change in policy by the PBoC (the central bank), there is only one thing that can cause such a move: a liquidity squeeze.

|

| Source: Shanghai Interbank Offered Rate |

China analysts point to a number of possibilities for this spike, including some action by the authorities to curb FX speculation or other trading activities. The best explanation however was that a panic ensued among China’s banking institutions due to a rumor that several banks were about to fail. This rumor, though unverified, caused banks to cut lending to each other, creating a liquidity squeeze. The squeeze was exacerbated by China’s markets being closed this Monday through Wednesday for the Dragon Boat Festival and liquidity already being tight coming into last week.

Reuters: – Early Friday, rates skyrocketed from already-high levels the previous day. Rumours that several mid-sized banks had defaulted on interbank loans added an element of fear to an acute liquidity shortage related to a coming national holiday and a slowdown in capital inflows. The rumours couldn’t be verified.

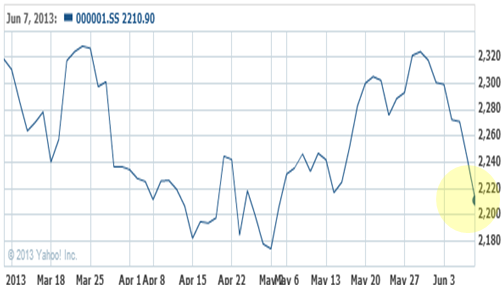

The stock market tanked in response.

|

| Shanghai composite |

It is thought that the PBoC has stepped in on Friday afternoon to ease liquidity conditions. The spike in short-term rates was not limited to SHIBOR, as the repo rates (secured lending) have been on the rise in recent days as well (with the repo curve now also highly inverted).

Reuters: – The weighted-average one-day repo rate closed at 8.68 percent on Friday – the highest since October 2007 – from 6.15 percent on Thursday. It’s extremely unusual for the one-day rate to move higher than the seven-day rate.

Dealers said the central bank had likely conducted short-term repos with selected banks, who were then able to transmit funds to the rest of the market.

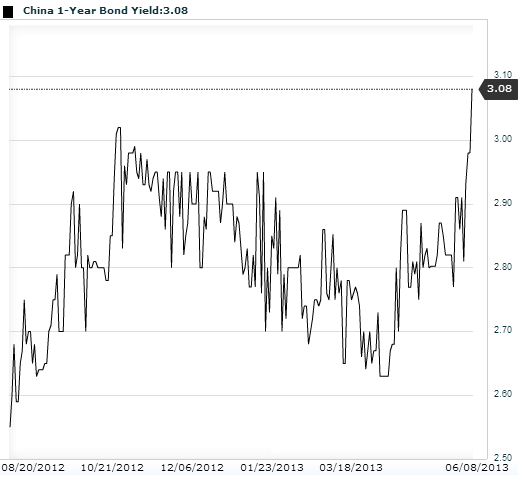

Even the one-year government-issued bill rate spiked, indicating that the short-term liquidity concern has spilled over to some longer term instruments.

|

| Source: Investing.com |

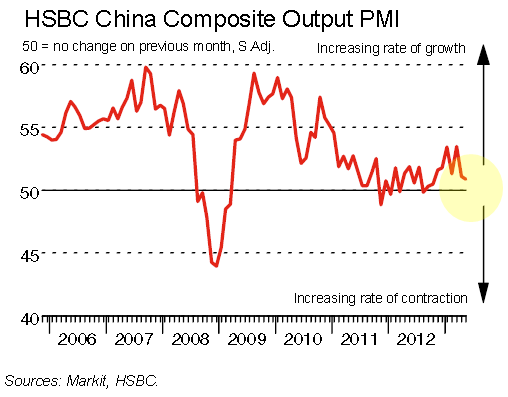

This is a dangerous development, particularly when China is already struggling with a relatively weak (by historical standards) growth. While the nation’s PMI numbers indicate an ongoing expansion on the whole, it is quite a slow one.

A spike in short term rates could dramatically dampen bank lending and slow growth even further. A prolonged spike could even put China into a recession. Many are hoping that the PBoC will deal with this issue aggressively by injecting more liquidity into the banking system in order to reduce the risk of a major credit contraction.