Edward Lambert at Effective Demand; Effective Demand = Effective Labor Income/(cu*(1-u)) points to the result of an economy left to maximize Profits at the expense of Labor. I have my own version or underlying causes of this issue and Edward gives the economic side of it.

I am going to show a graph of Productivity against Effective demand. It is an intriguing and a disturbing graph. Let me start by giving the equation for the productivity used in the graph.

Productivity = real compensation per hour: business sector/(labor share: business sector * 0.78)

The data for this equation comes from this graph at FRED.

The equation for effective demand is…

Effective Demand = real GDP * (labor share: business sector * 0.78)/TFUR

TFUR (total factor utilization rate) = capacity utilization * (1 – unemployment rate)

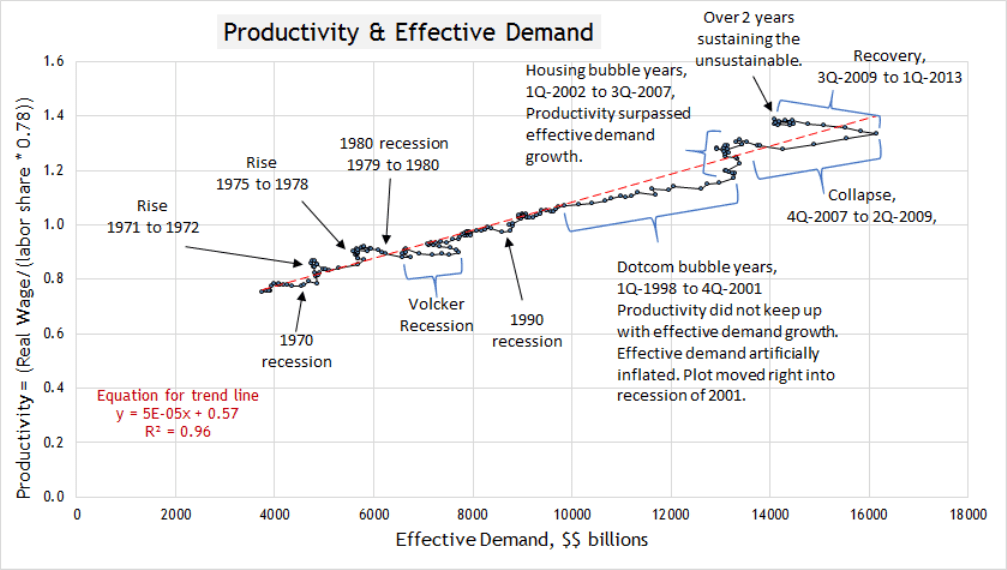

Let me just show the graph and then start explaining…

The graph shows quarterly data from 1967 to the 1st quarter of 2013. The red dashed line is a trend line for the data. We can see that from 1967 to 1997, the plot stayed very tight on the trend line. There were deviations from this line during times of shocks and recessions. But it is very interesting how closely the plot followed the trend line before 1997.

Before 1997, the plot going below the trend line was associated with a recession. The explanation of this is that effective demand rises more during a recession because of more available capacity of labor and capital. At the same time. productivity tends to fall behind the trend line due to rising labor share, not falling real compensation.

When the plot goes above the trend line, productivity is ahead of effective demand. Productivity rises due to labor share settling down and real compensation rising. Effective demand tends to stay still during the expansionary phase of a business cycle. The economy grows up to the effective demand limit and then gets set for a contraction.

We used to have a balance between productivity and effective demand. The economy moved directly on top of the trend line for many many quarters. And now the economy has lost that balance. Since the late 90′s it is a fleeting moment when productivity and effective demand come together on the trend line.

Before 1997, there was very little movement away from the trend line. Then something unusual happened between 1997 and 2001, the dotcom bubble years. The plot went progressively below the trend line even though there was no recession. Productivity was rising during these years, but effective demand was rising at such an unusual rate that productivity could not keep up with it. Effective demand was being artificially created and inflated. The recession of 2001 followed the same unusual path as before the recession.

In 2002, the economy had to make an adjustment. Productivity had to rise or effective demand had to fall. During the housing bubble years (from 2002 to the quarter right before the 2008 recession), productivity rose, while effective demand basically stayed steady. The plot went back above the trend line showing that productivity was beyond the capacity of effective demand and that productivity was at a non-sustainable level. The economy sustained this high level of productivity in the face of low effective demand for a few years, but eventually the correction would come in 2008. The correction was a collapse.

Look at where the economy is now. Since the end of 2010, the plot has barely moved from a productivity just below 1.4 and an effective demand around $14.1 trillion. The plot is way above the trend line and has been just sitting in the same spot for over 2 years. Effective demand is too low for the current productivity in the US. This is an economic bomb building energy that will eventually go off when real GDP approaches $14.1 trillion.

A friend of mine had a dream a few nights ago, where a spirit said that the economy is dying. The graph above would lead one to think the same.

Think about it… where can the economy go now from here?

There are 2 options . . .

Option #1 looks at the equation for Productivity: You have to lower productivity by increasing labor share in relation to real compensation.

1. If you lower real compensation, labor share would fall, but it would have to fall slower than real compensation. Keep in mind though that a lower labor share would lower effective demand too, which would work against the objective. However, if labor share actually rose in the face of lowering real compensation, you would see an economic contraction. So lowering real compensation is not a good option.

2. On the other hand, if you raised labor share faster than raising real compensation, productivity would come down as effective demand increased from higher labor share. This is a safe and sensible way to correct the huge imbalance we find ourselves in.

Option #2 looks at the equation for Effective Demand: You have to increase effective demand back up to $16 trillion. There are two options here as well.

1. Utilization of labor and capital would have fall. (TFUR in the equation above would have to fall.) This would mean a rise in unemployment, which would mean another collapse.

2. Labor share would have to rise. This would also have the beneficial effect of lowering productivity, as long as real compensation rose moderately.

As we can see, the only real option to avert another collapse is to raise labor share of income. This is not likely as businesses are even now fighting an increase in just the minimum wage. Businesses are trying to maximize their profits and do not want to raise labor costs. Yet this objective of theirs is going to kill the economy.

The graph above shows that there is a bomb ticking, and it is a bigger bomb than we saw in 2008. Higher productivity in the face of low effective demand is unsustainable. Yet, we have been sustaining it for over 2 years now with an incredible expansionary monetary policy in the face of an incredibly low labor share of income.