It seems that aside from halting the yuan appreciation (see discussion) Beijing has decided to use fiscal rather than monetary tools to stimulate the economy.

Bloomberg: – Chinese Premier Li Keqiang said the nation will speed railway construction, especially in central and western regions, adding support for an economy that’s set to expand at the slowest pace in 23 years.

The State Council also yesterday approved tax breaks for small companies and reduced fees for exporters as it pledged to keep the yuan’s exchange rate “basically stable at a reasonable and balanced level,” according to a statement after a meeting led by Li. China plans a railway development fund, the government said.

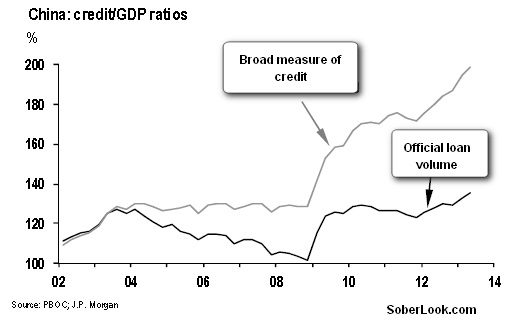

Once again, the rationale to maintain a relatively tight monetary stance is to make sure that the shadow high yield deposit business and property speculation doesn’t grow out of control (see post). Applying the brakes too suddenly however is quite dangerous, particularly for a nation that in recent years has become addicted to credit. The broad measure of credit (sometimes called “social financing”) is now nearly double the GDP.

|

| Source: JPMorgan |

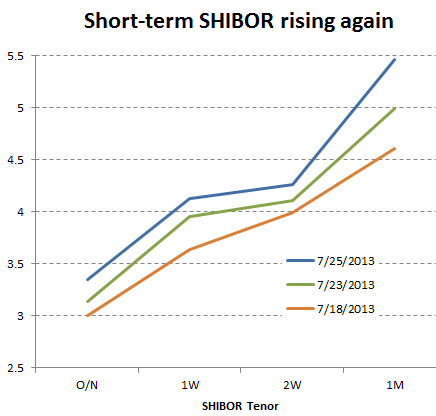

Tight and uncertain monetary policy could have a severe adverse effect on China’s weakened economy by forcing an uncontrolled unwind of credit. And PBoC’s policy remains both tight and uncertain. The overnight interbank (SHIBOR) rate has risen by 35bp in the past week. Most central banks would spend months fretting over such an adjustment. Other short-term rates have risen even more.

PBoC’s attempt to force an abrupt end to credit addiction could easily offset any economic benefits of speed railway construction or tax breaks. Bursting such a massive credit bubble is a delicate process, which China’s central bank is not executing in a controlled manner.

From our sponsor: