Credit Suisse is ringing alarm bells on corporate earnings – both in the US and Europe. The Wal-Mart negative earnings surprise last week for example could be signaling a slower earnings trajectory for other firms.

|

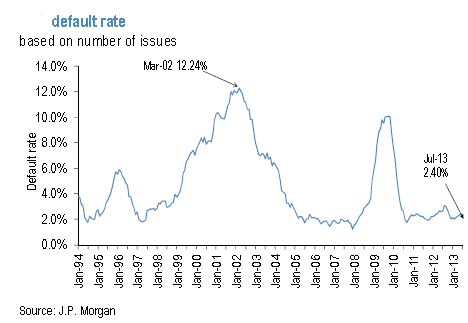

What CS is particularly focused on is not necessarily the stock market valuations in the US and Europe (which is a separate problem), but corporate default rates instead. So far default rates have been extraordinary low – around the levels seen during 2005-2007 “bubble” years.

|

|

US HY issuers default rate (source: JPM) |

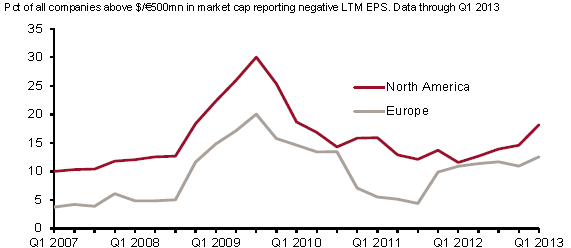

Increasing numbers of middle market firms are having difficulties growing revenue or even losing money and yet obtaining all sorts of financing (see post). The current earnings situation is simply not consistent with the current level of default rates.

CS: – … the current levels of companies losing money on both sides of the Atlantic is rising. This is not yet a phenomenon in the largest companies – which is why Wal-Mart might be very important – more, it is a problem in the medium-capitalisation range. But it would normally be associated with a very much higher high-yield default rate and therefore much tighter financing conditions of which all markets, not just credit markets, would have to take notice.

|

|

Source: CS |

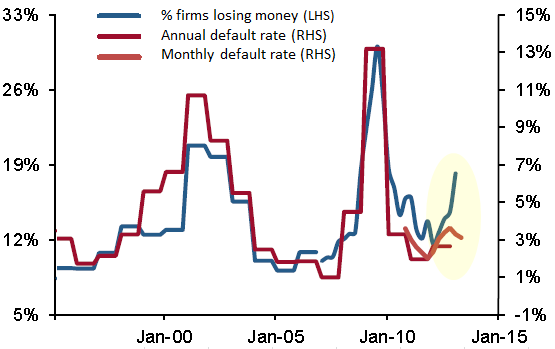

As the percentage of money-losing firms rises, corporate default rates should follow. The chart below compares the two trends: “Current profit performance is consistent with a default rate of 6%, not

the current 2.8% in the US …“

|

|

US firms only (source: CS; slightly modified/simplified) |

That is why Q3 earnings results will be vital. If the rise in the number of firms with poor or negative earnings continues, default rates are sure to pick up. And the catalyst could be the sudden spike in interest rates we’ve had – which has the potential to squeeze corporate margins.

CS: – So we have a strong suspicion that the medicine applied to the financial sector has suppressed corporate defaults (the thematic “zombie companies” argument.) Raising the awful possibility that we may be only part-way through a current default event dating all the way back to 2008/9, with the other foot to fall as we all realize that the new normal has to involve some sort of positive interest rate.