This Friday’s US non-farm payrolls report is likely to be one of the most impactful pieces of economic data for global financial markets in recent months. All major asset classes will be impacted because this is considered the one critical piece of data the Fed will need to make its decision at the next FOMC meeting. The expectations for new jobs, particularly the private payrolls number continue to be tempered. According to Econoday, the average forecast for August is 178,000 new private jobs and 175,000 total.

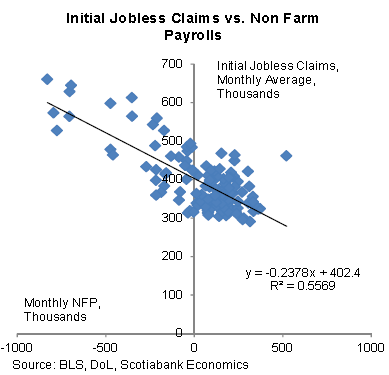

While these numbers are sufficient for the Fed to begin tapering its purchases, the forecasts are not great – the average number of jobs created per month over the past couple of years is 188,000. Why are the forecasts below recent averages? After all, initial jobless claims have been declining steadily, with consistently fewer people filing for unemployment for the first time (see Twitter chart). Unfortunately, while there is a long-term relationship between jobless claims and payrolls, the claims number is not a great predictor of new jobs created.

|

| Source: Scotiabank |

Based the regression performed by Scotiabank, this Friday’s non-farm payroll gain should be 347,000/month – which is impossible. That’s why nobody tries to use these claims numbers to forecast new job creation (Scotia’s own forecast is 185k).

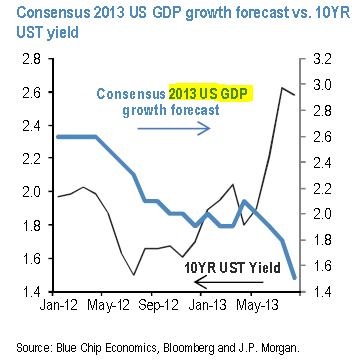

Instead, many forecasters (in addition to various labor surveys) focus on where they see the nation’s economic expansion trending. And the US GDP growth consensus has been significantly tempered in the past few months (which JPMorgan attributes to higher rates).

|

| Source: JPMorgan |

That’s why going forward, payrolls forecast will remain below recent historical averages. But unless there is a major surprise to the downside, the forecasted figures are good enough for the Fed to begin slowing purchases of securities.