India is about to get a new new central bank governor, Raghuram Rajan, a University of Chicago economist with outstanding academic credentials. He is expected to start this Thursday, smack in the middle of a financial crisis the likes of which have not been seen in India since the early 90s. He will be dealing with a no-win situation in which he is faced with just two key choices:

1. Let the currency continue to fall and face a dramatic rise in inflation and a corporate sector struggling with increasing import prices. That could lead to a rise corporate failures as margins are squeezed. The currency fall would be exacerbated by the fact that several large Indian firms carry some of their liabilities in dollars. Furthermore, the government deficit will rise further as it continues to subsidize ever more expensive fuel imports.

2. Tighten liquidity further and raise short-term rates. This is what the RBI has in fact been doing, but unfortunately it hasn’t worked. The rupee traded near all-time lows again today.

|

|

Source: Investing.com |

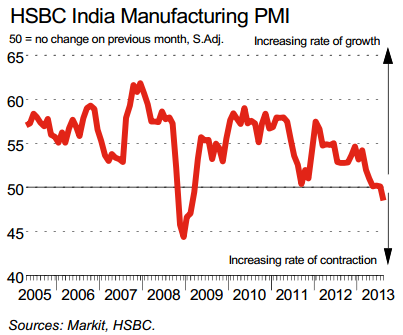

And now we are seeing this uncertainty and tight liquidity quickly spill over into the “real economy”. The GDP growth slipped to nearly a decade low (see chart) and yesterday we saw the manufacturing sector contracting in August for the first time since the Great Recession.

|

|

Source: Markit |

The RBI of course could also use its foreign reserves to defend the currency. But once the markets sense that the reserves are running low, debt downgrades and market panic will ensue, with the 1991 nightmare scenario (see post) becoming a reality. At this stage the RBI will avoid using its reserves in outright rupee purchases as much as possible. The central bank could also perform some sterilized operations (see post), but these tend to be fairly short-lived.

India’s new central banker certainly has his work cut out for him. He is expected to be more transparent with the markets and provide leadership, hoping to instill some much needed confidence in India’s central bank. Unfortunately what India faces is a structural issue, driven by a massive current account imbalance resulting from funding the trade deficit with foreign capital inflows. This capital from foreign investors however has recently turned into outflows. To solve that will take time – something the RBI and its new governor do not currently have.