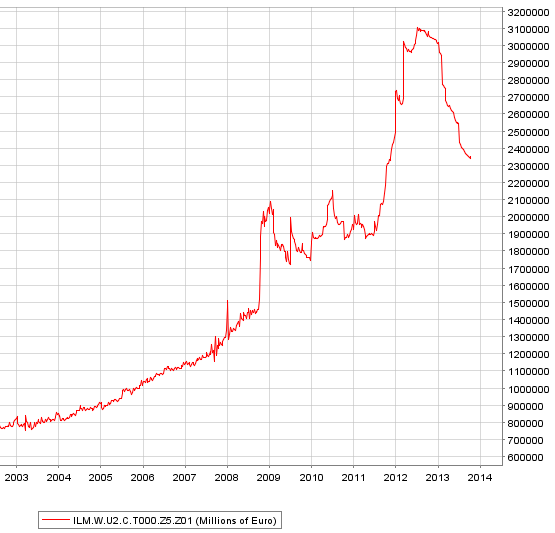

Over the past year, the ECB’s (Eurosystem’s) consolidated balance sheet declined roughly three quarters of a trillion euros. As discussed earlier (see post) most of this decline is due to the repayment of a portion of the MRO/LTRO loans that the ECB extended to the area’s banks in 2011 and 2012.

|

|

ECB’s (Eurosystem) balance sheet (source: ECB) |

Some economists – particularly those looking at the Fed and the BOJ – view this reduction as a form of tightening in the area’s monetary conditions. The ongoing need to roll a number of maturing periphery governments’ and banks’ bonds, risks flaring up the debt crisis. Many believe the ECB should flood the banking system with liquidity once again in order to blunt any roll issues as well as to halt the declines in credit growth (see post).

A number of economists think that “LTRO-III”, a third major long-term lending program to the euro area’s banks, will help the situation. According to them it is only a matter of time before the ECB decides to proceed with another round of liquidity injections.

Goldman: – We no longer expect the ECB to offer a longer-maturity LTRO by the end of the year, following the latest statements from a number of Governing Council members to the effect that such a move was not being considered at this point. However, we maintain our view that such a measure would address several potential problems affecting the banking sector and the wider economy. A longer-maturity LTRO would, for example, buy insurance against the risk that maturing short-term government and bank debt would lead to renewed tensions in the Euro area financial system. We therefore continue to believe the ECB will eventually counter the decline in excess liquidity by offering another longer-maturity LTRO.