Years ago I was watching the action around an Atlantic City roulette table when I noticed a man taking careful notes. When I asked what he was doing he said he was looking for long consecutive strings of red or black. If the run got long enough he was going to bet that the ball on the next spin would land on the opposite color because it was “due.”

When I asked him how the ball knew what colors it had previous landed on he frowned and shifted a few steps away.

The Gambler’s Fallacy is an intuitive belief that long streaks, even with fair coins or dice, influence the odds of the next result.

On a day to day basis the stock market is a lot like the game of roulette, with the probability of an up or down day being very close to 50%. However unlike the roulette ball, the people trading on the stock market can remember what has happened previously—so after a long stretch of up days, you would expect a higher probability of a down day. Or so I thought.

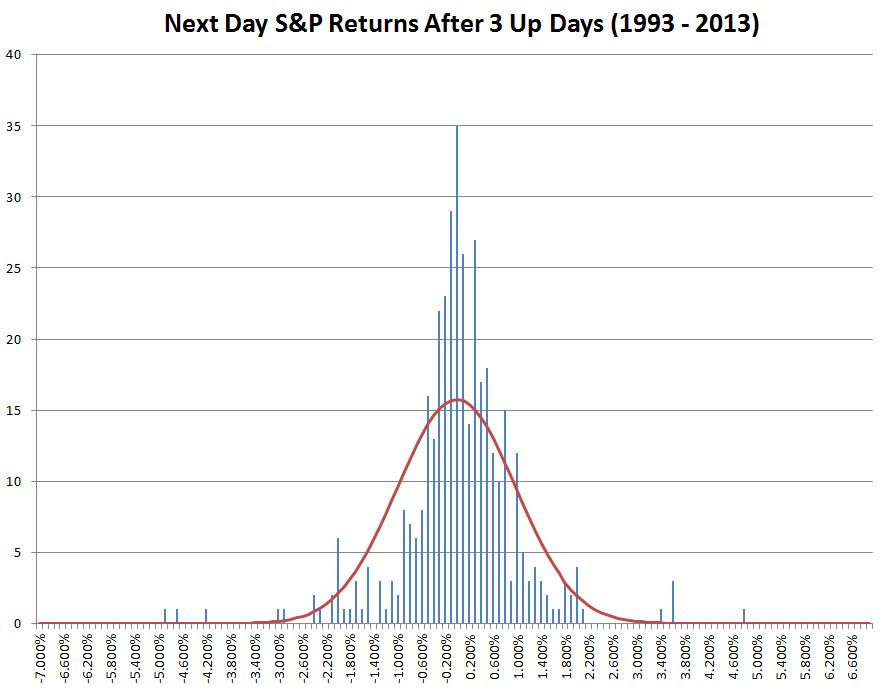

For a long time I’ve believed that the market tends to move in 3 day cycles, but inspired by reading Moneyball (borrow free on Amazon prime), I decided to see if the data supported my intuition. I took the S&P 500 index data from 1993 to 2013 and analyzed market moves after 3, 4, 5, and 6 up days in a row. Rather than just plotting a binary up or down results I plotted the frequency of the percentage results using 0.1% bins.

|

The red line shows the outline of what a perfect normal distribution would look like. The actual data is more clustered around zero, under-represented on the sides of the distribution, with some “Black Swan” events in the tails of the distribution.

Instead of supporting my intuition the data shows that the stock market is very much like roulette, with no directional bias after three consecutive up days. The average return (mean) is -.016%— indicating very close to even odds.

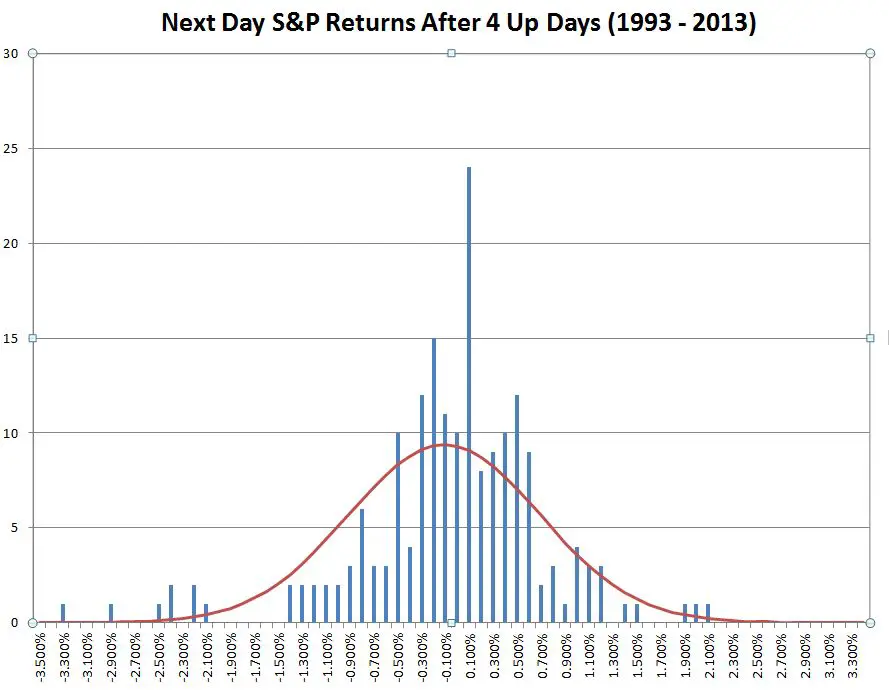

I repeated the analysis for bull runs of 4, 5, and 6 consecutive days.

|

|

These sequences also show average returns close to zero. With even odds the number of consecutive days with gains should decrease by 50% for each additional day—and they do.

The 5 Up Days statistics are distorted by a giant 8.9% drop on 1-Dec-2008 so I show the 5 up data with and without that drop

| 3 Up Days | 4 Up Days | 5 Up Days | 5 Up Days (minus 1-Dec-08) | 6 Up Days | |

| Occurrences | 390 | 188 | 93 | 92 | 46 |

| Average Next Day Returns (Mean) | -0.0156% | -0.109% | 0.0444% | 0.0522% | -0.0360% |

| Next Day Standard Deviation | 0.99% | 0.88% | 1.19% | 0.75% | 0.58% |

| Largest Loss | -4.9% | -3.3% | -8.9% | -1.8% | -1.6% |

| Largest Gain | 4.7% | 2.1% | 2.2% | 2.2% | -2.1% |

If you exclude the “7 sigma” event in 2008 there is a trend towards less actual volatility the next day with longer bull streaks. It might be the case that the people involved with the market become increasingly aware of the bull run and start behaving cautiously. This trend would be no help for directional plays, and it’s hard for me to imagine a volatility play that could take advantage of a one day lull.

Clearly my notion that the market moves in 3 day cycles was bogus, and the data suggests that any sort of directional analysis based on market history is just another example of the Gambler’s Fallacy.