Earlier I posted some questions for next year: Ten Economic Questions for 2014. I’ll try to add some thoughts, and maybe some predictions for each question.

Here is a review of the Ten Economic Questions for 2013.

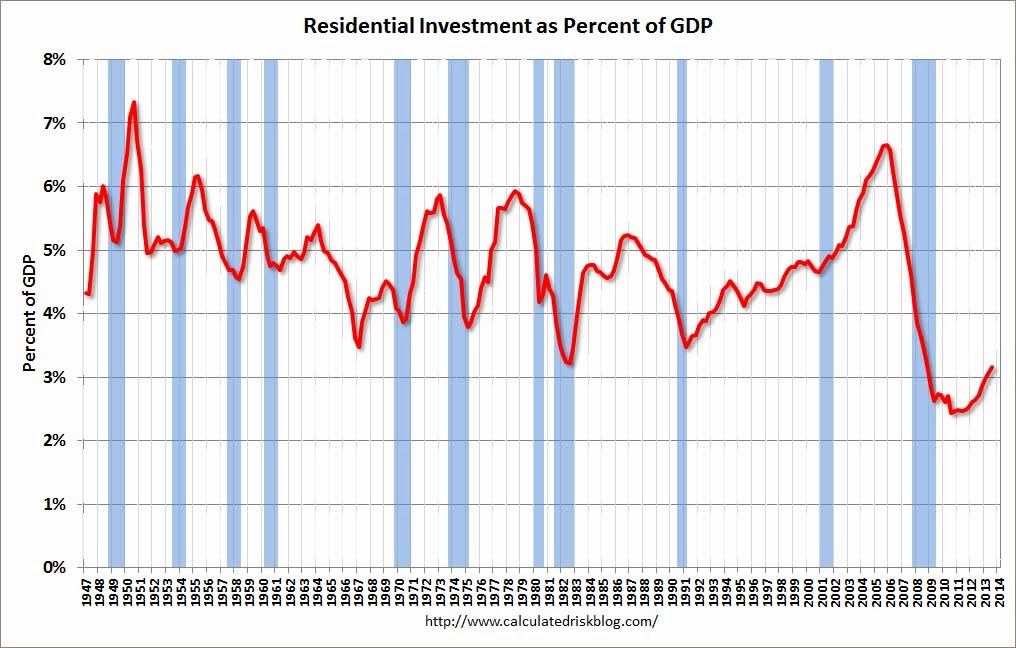

6) Residential Investment: Residential investment (RI) picked was up solidly in 2012 and 2013. Note: RI is mostly investment in new single family structures, multifamily structures, home improvement and commissions on existing home sales. Even with the recent increases, RI is still at a historical low level. How much will RI increase in 2014?

First a graph of RI as a percent of Gross Domestic Product (GDP) through Q3 2013.

Click on graph for larger image.

Click on graph for larger image.

Usually residential investment is a strong contributor to GDP growth and employment in the early stages of a recovery, but not this time – and that weakness was a key reason why the recovery was sluggish so far. Residential investment finally turned positive during 2011 and made a solid positive contribution to GDP in both 2012 and 2013.

But even with recent increases, RI as a percent of GDP is still very low – and still below the lows of previous recessions – and it seems likely that residential investment as a percent of GDP will increase further in 2014.

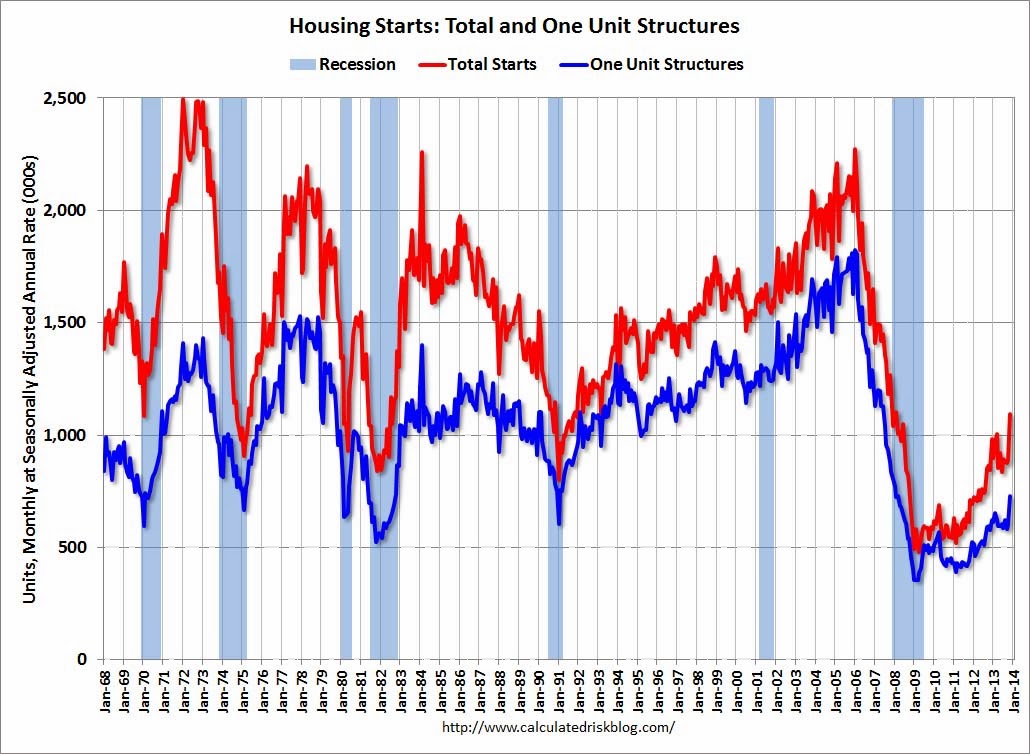

The second graph shows total and single family housing starts through November 2013.

The second graph shows total and single family housing starts through November 2013.

Housing starts are on pace to increase about 20% in 2013. And even after the sharp increase over the last two years, the approximately 938 thousand housing starts in 2013 will still be the 6th lowest on an annual basis since the Census Bureau started tracking starts in 1959 (the five lowest years were 2008 through 2012).

Here is a table showing housing starts over the last few years. No one should expect an increase to 2005 levels, however demographics and household formation suggest starts will return to close to the 1.5 million per year average from 1959 through 2000. That means starts will come close to increasing 60% over the next few years from the 2013 level.

| Housing Starts (000s) | ||||

|---|---|---|---|---|

| Total | Change | Single Family | Change | |

| 2005 | 2,068.3 | — | 1,715.8 | — |

| 2006 | 1,800.9 | -12.9% | 1,465.4 | -14.6% |

| 2007 | 1,355.0 | -24.8% | 1,046.0 | -28.6% |

| 2008 | 905.5 | -33.2% | 622.0 | -40.5% |

| 2009 | 554.0 | -38.8% | 445.1 | -28.4% |

| 2010 | 586.9 | 5.9% | 471.2 | 5.9% |

| 2011 | 608.8 | 3.7% | 430.6 | -8.6% |

| 2012 | 780.6 | 28.2% | 535.3 | 24.3% |

| 20131 | 938.0 | 20% | 625.0 | 17% |

| 12013 estimated | ||||

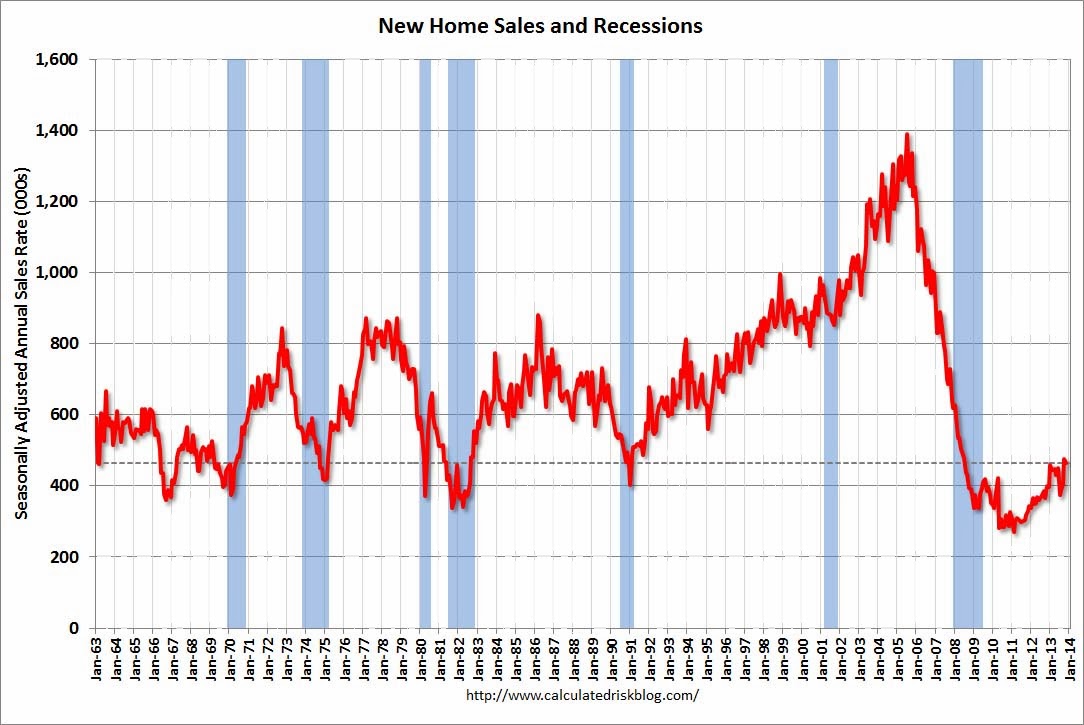

The third graph shows New Home Sales since 1963 through November 2013. The dashed line is the current sales rate.

The third graph shows New Home Sales since 1963 through November 2013. The dashed line is the current sales rate.

Just like for RI as a percent of GDP, and housing starts, new home sales were up in 2013, but are still near the low historically.

New home sales will still be competing with distressed sales (short sales and foreclosures) in some judicial foreclosure states in 2014. However, unlike last year when I reported that some builders were land constrained (not enough finished lots in the pipeline), land should be less of an issue this year. Even with the foreclosures, I expect another solid year of growth for new home sales.

Here are some recent forecasts for housing in 2014. I expect growth for new home sales and housing starts in the 20% range in 2014 compared to 2013. That would still make 2014 the tenth weakest year on record for housing starts (behind 2008 through 2012 and few other recession lows). So I expect further growth in 2015 too.

Here are the ten questions for 2014 and a few predictions:

• Question #6 for 2014: How much will Residential Investment increase?

• Question #7 for 2014: What will happen with house prices in 2014?

• Question #8 for 2014: Housing Credit: Will we see easier mortgage lending in 2014?

• Question #9 for 2014: How much will housing inventory increase in 2014?

• Question #10 for 2014: Downside Risks