The call for comments on the post about taxation (here) has generated an excellent discussion – with comments that are both thoughtful and informative. Thanks everyone! Since the process seemed to work so well, let’s try something like that again.

The topic this time is the recent decline in labor productivity growth in the US.

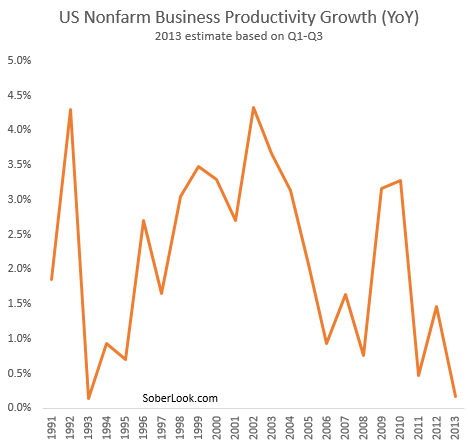

|

| Source: BLS (PRS85006093) |

The slowdown seems to be a puzzle, with a variety of explanations, none of which seem to be entirely satisfactory. Here is what Ben Bernanke had to say about it yesterday:

Ben Bernanke: – Although the Federal Reserve, like other forecasters, has tended to be overoptimistic in its forecasts of real GDP during this recovery, we have also, at times, been too pessimistic in our forecasts of the unemployment rate. For example, over the past year unemployment has declined notably more quickly than we or other forecasters expected, even as GDP growth was moderately lower than expected a year ago. This discrepancy reflects a number of factors, including declines in participation, but an important reason is the slow growth of productivity during this recovery; intuitively, when productivity gains are limited, firms need more workers even if demand is growing slowly. Disappointing productivity growth accordingly must be added to the list of reasons that economic growth has been slower than hoped. (Incidentally, the slow pace of productivity gains early in the recovery was not evident until well after the fact because of large data revisions–an illustration of the frustrations of real-time policymaking.) The reasons for weak productivity growth are not entirely clear: It may be a result of the severity of the financial crisis, for example, if tight credit conditions have inhibited innovation, productivity-improving investments, and the formation of new firms; or it may simply reflect slow growth in sales, which have led firms to use capital and labor less intensively, or even mismeasurement. Notably, productivity growth has also flagged in a number of foreign economies that were hard-hit by the financial crisis. Yet another possibility is weak productivity growth reflects longer-term trends largely unrelated to the recession. Obviously, the resolution of the productivity puzzle will be important in shaping our expectations for longer-term growth.

Thoughts? Comments?

From our sponsor: