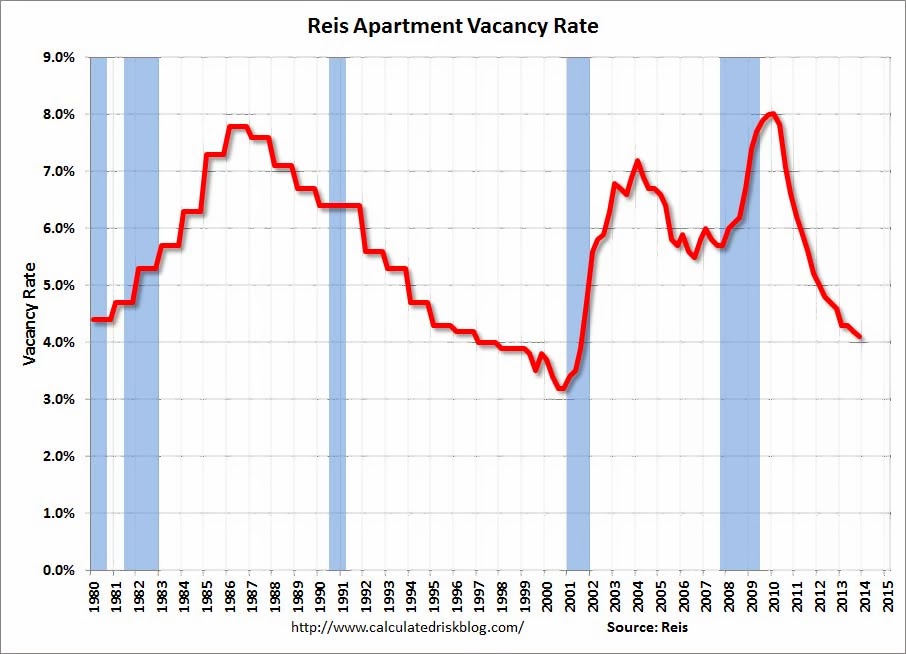

Reis reported that the apartment vacancy rate declined in Q4 to 4.1% from 4.2% in Q3. In Q4 2012 (a year ago) the vacancy rate was at 4.6%, and the rate peaked at 8.0% at the end of 2009.

Some data and comments from Reis Senior Economist Ryan Severino:

Vacancy declined by 10 basis points during fourth quarter to 4.1%, in line with last quarter’s 10 basis point decline. Over the last year the national vacancy rate has declined by 50 basis points, on par with the year‐over‐year rate from the last few quarters. Demand for apartments remains strong four years after the recovery began, even as construction activity has gradually been increasing. Not even the seasonal weakness normally observed during the fourth quarters of calendar years had much if any impact on the market dynamics. The national vacancy rate now stands 390 basis points below the cyclical peak of 8.0% observed right after the recession concluded in late 2009.

Shrugging off the typical seasonal weakness that is observed during the fourth quarter of calendar years, demand for apartments remained stout in the fourth quarter of 2013. The sector absorbed 50,728 units, the largest figure since the fourth quarter of 2010. For 2013, the sector absorbed almost 165,000 units, ahead of 2012 but below the incredibly robust demand of 2010 and 2011. Meanwhile completions during the third quarter were 41,683 units, the highest quarterly total in ten years since the fourth quarter of 2003 when the market delivered 41,995 units. As we have been warning for the last few quarters, supply growth is clearly on an upswing. Roughly 127,000 units were delivered during 2013. This is in line with the long‐term historical average level of completions and the highest annual total since 2009. Four years after the advent of a recovery in the apartment market, newly completed units continue to be absorbed.

Asking and effective rents both grew by 0.8% during the fourth quarter. … rent growth for 2013 came in below rent growth in 2012. Given the incredibly low vacancy rate, rent growth this weak is unprecedented. Normally at such a low vacancy rate, rent growth is at least 100 basis points above current growth rates on an annual basis. Although the labor market continues to convalesce, it remains far too slack for rent growth to accelerate much. In the past when the national vacancy rate fell near 4%, the economy and the labor market were stronger than they currently are. Moreover, on a nominal basis, rents are at historically high levels, which is also restraining tenants’ ability to pay higher rents in many markets.

…

The apartment market has been on quite a tear over the last four years, with demand seemingly insatiable. With the economy and labor market expected to improve in 2014, one would think that the good times will continue unabated. However, the tremendous performance in the apartment market has spurred a substantial increase in construction activity and this is dampening the outlook for 2014. Completions next year should total more than 160,000, roughly one‐third greater than the long‐term historical average for annual completions. Demand will not implode but will struggle to keep pace with escalating completions. Therefore, we anticipate that for the first time since 2009 the national vacancy rate will rise in 2014.

emphasis added

Click on graph for larger image.

Click on graph for larger image.

This graph shows the apartment vacancy rate starting in 1980. (Annual rate before 1999, quarterly starting in 1999). Note: Reis is just for large cities.

New supply is finally coming on the market and the decline in the vacancy rate has slowed – and Reis is projecting a slight increase in the vacancy rate this year

Apartment vacancy data courtesy of Reis.