The Department of Commerce reported this morning:

[T]otal December exports of $191.3 billion and imports of $230.0 billion resulted in a goods and services deficit of $38.7 billion, up from $34.6 billion in November, revised. December exports were $3.5 billion less than November exports of $194.8 billion. December imports were $0.6 billion more than November imports of $229.4 billion.

The trade deficit was larger than the consensus forecast of $36.0 billion.

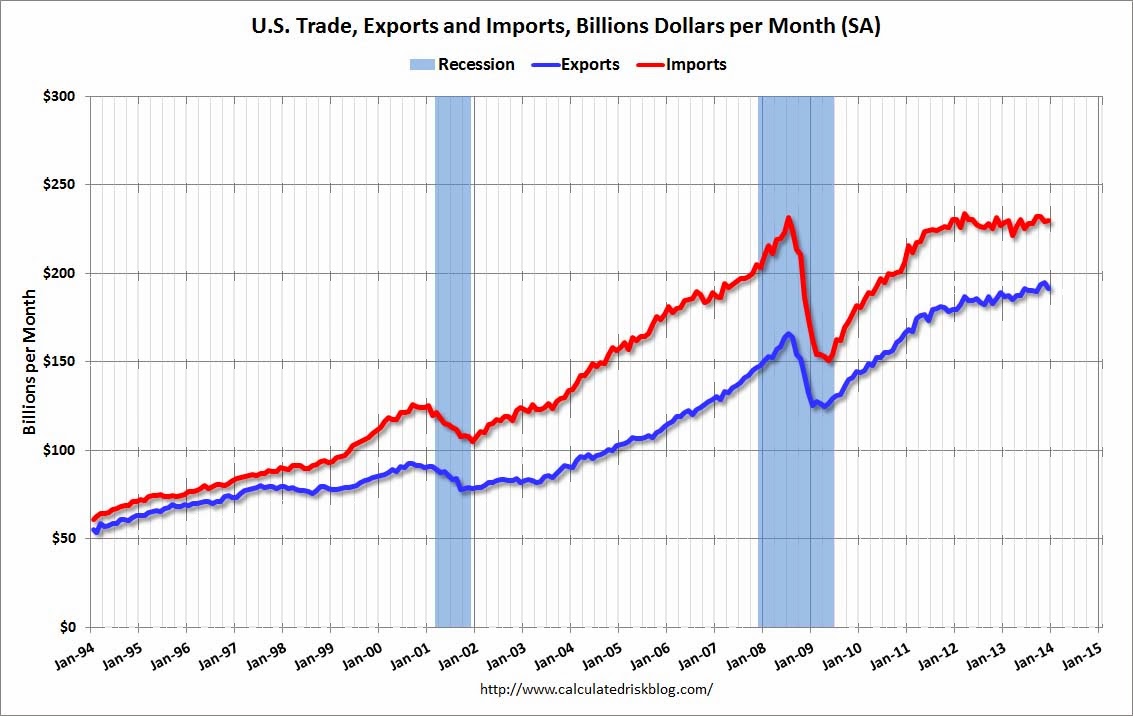

The first graph shows the monthly U.S. exports and imports in dollars through December 2013.

Click on graph for larger image.

Click on graph for larger image.

Imports increased, and exports decreased in December.

Exports are 15% above the pre-recession peak and up 1% compared to December 2012; imports are just below the pre-recession peak, and up about 1% compared to December 2012.

The second graph shows the U.S. trade deficit, with and without petroleum, through December.

The blue line is the total deficit, and the black line is the petroleum deficit, and the red line is the trade deficit ex-petroleum products.

The blue line is the total deficit, and the black line is the petroleum deficit, and the red line is the trade deficit ex-petroleum products.

Oil averaged $91.34 in December, down from $94.69 in November, and down from $95.16 in December 2012. The petroleum deficit has generally been declining and is the major reason the overall deficit has declined since early 2012.

The trade deficit with China was mostly unchanged at $24.47 billion in December, from $24.53 billion in December 2012. A majority of the trade deficit is related to China.

Overall it appears exports are picking up a little, and imports (ex-oil) are increasing too.