This will be a busy week for economic data with several key reports including the March employment report on Friday.

Other key reports include the ISM manufacturing index on Tuesday, February vehicle sales on Tuesday, the ISM service index on Thursday, and the February trade deficit report on Thursday.

Also, Reis is scheduled to release their Q1 surveys of rents and vacancy rates for apartments, offices and malls.

9:45 AM: Chicago Purchasing Managers Index for March. The consensus is for a decrease to 58.5, down from 59.8 in February.

9:55 AM: Speech, Fed Chair Janet Yellen, Strengthening Communities, At the 2014 National Interagency Community Reinvestment Conference, Chicago, Ill.

10:30 AM: Dallas Fed Manufacturing Survey for March. This is the last of the regional Fed manufacturing surveys for March.

Early: Reis Q1 2014 Office Survey of rents and vacancy rates.

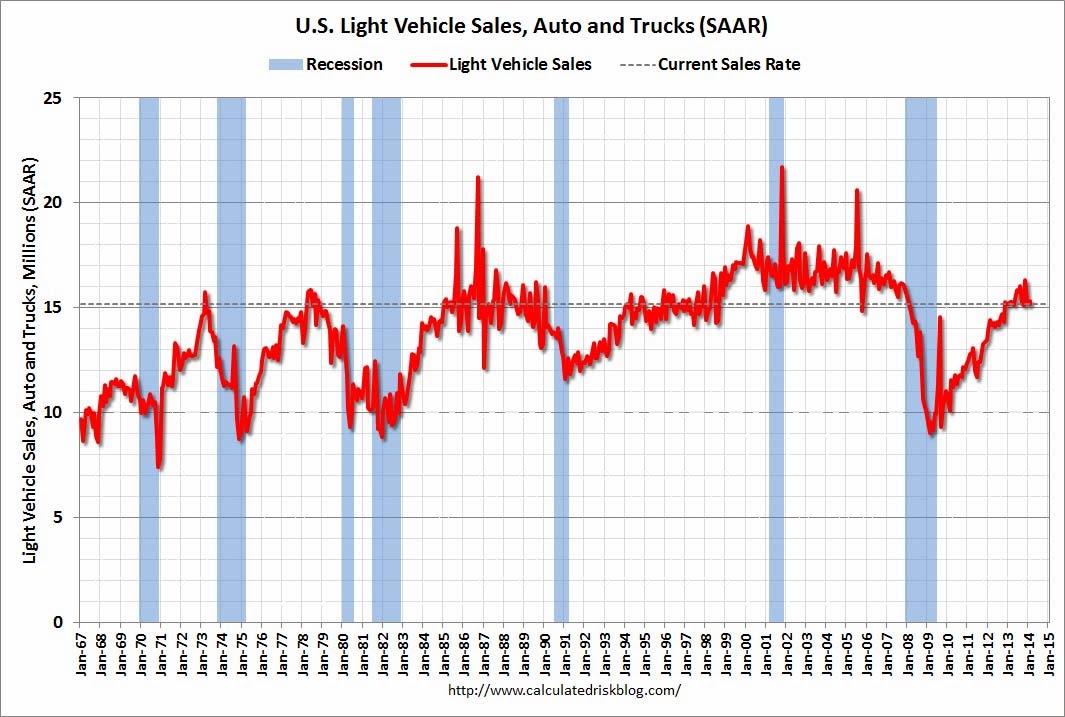

All day: Light vehicle sales for March. The consensus is for light vehicle sales to increase to 15.8 million SAAR in March (Seasonally Adjusted Annual Rate) from 15.3 million SAAR in February.

All day: Light vehicle sales for March. The consensus is for light vehicle sales to increase to 15.8 million SAAR in March (Seasonally Adjusted Annual Rate) from 15.3 million SAAR in February.

This graph shows light vehicle sales since the BEA started keeping data in 1967. The dashed line is the February sales rate.

9:00 AM ET: The Markit US PMI Manufacturing Index for March.

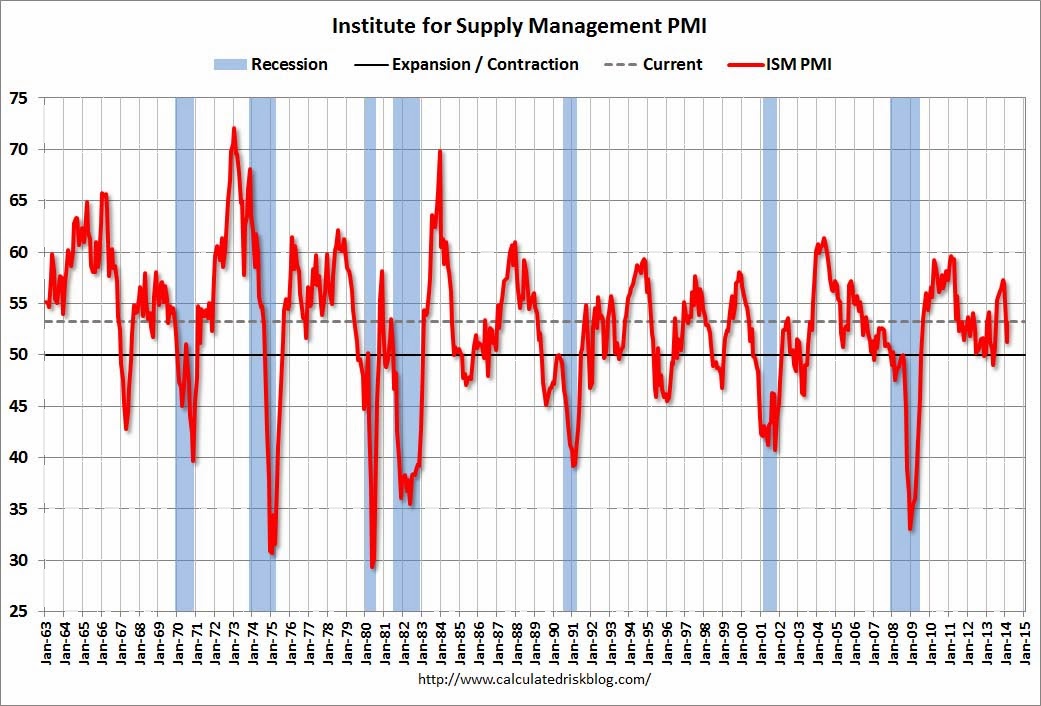

Here is a long term graph of the ISM manufacturing index.

The ISM manufacturing index indicated expansion in February at 53.2%. The employment index was at 52.3%, and the new orders index was at 54.5%.

10:00 AM: Construction Spending for February. The consensus is for a 0.1% increase in construction spending.

Early: Reis Q1 2014 Apartment Survey of rents and vacancy rates.

7:00 AM: The Mortgage Bankers Association (MBA) will release the results for the mortgage purchase applications index.

8:15 AM: The ADP Employment Report for March. This report is for private payrolls only (no government). The consensus is for 190,000 payroll jobs added in March, up from 139,000 in February.

10:00 AM: Manufacturers’ Shipments, Inventories and Orders (Factory Orders) for February. The consensus is for a 0.8% increase in February orders.

Early: Reis Q1 2014 Mall Survey of rents and vacancy rates.

8:30 AM: The initial weekly unemployment claims report will be released. The consensus is for claims to increase to 320 thousand from 311 thousand.

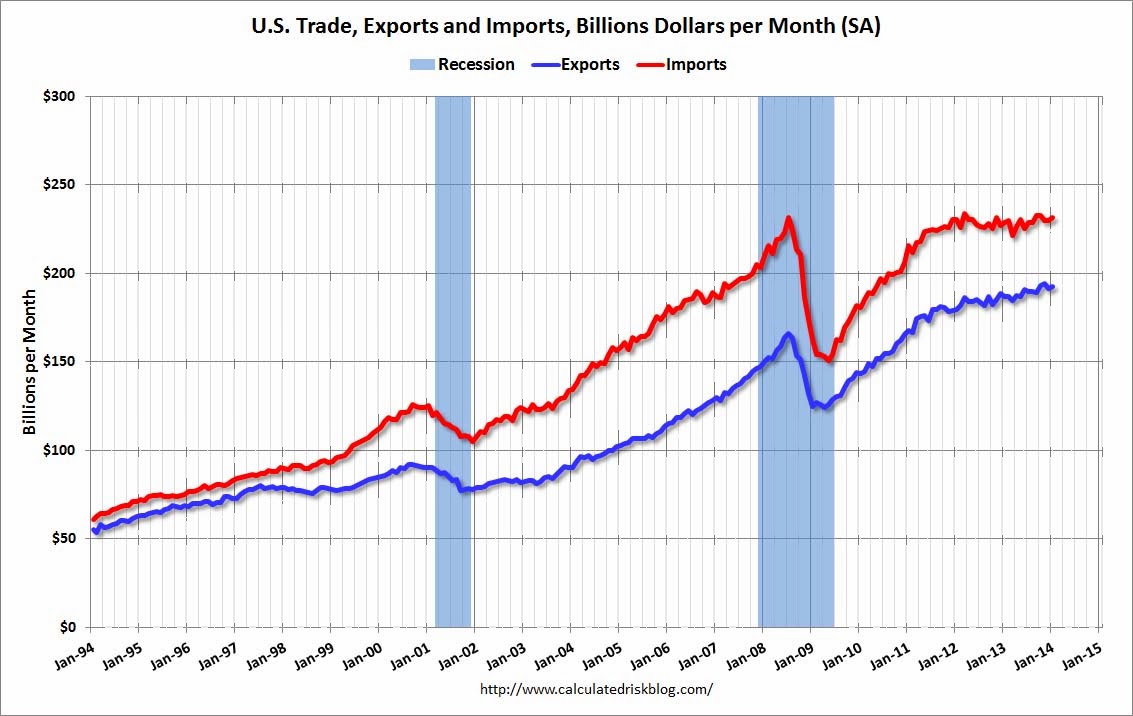

8:30 AM: Trade Balance report for February from the Census Bureau.

8:30 AM: Trade Balance report for February from the Census Bureau.

Imports and exports increased in January.

The consensus is for the U.S. trade deficit to decrease to $38.5 billion in February from $39.1 billion in January.

10:00 AM: ISM non-Manufacturing Index for March. The consensus is for a reading of 53.5, up from 51.6 in February. Note: Above 50 indicates expansion, below 50 contraction.

8:30 AM: Employment Report for March. The consensus is for an increase of 206,000 non-farm payroll jobs in March, up from the 175,000 non-farm payroll jobs added in February.

The consensus is for the unemployment rate to declined to 6.6% in March.

This graph shows the percentage of payroll jobs lost during post WWII recessions through February.

This graph shows the percentage of payroll jobs lost during post WWII recessions through February.

The economy has added 8.7 million private sector jobs since employment bottomed in February 2010 (8.0 million total jobs added including all the public sector layoffs).

There are still almost 129 thousand fewer private sector jobs now than when the recession started in 2007. Private sector employment at a new high will probably be a headline for the March report.