by Joseph Joyce (is a Professor of Economics at Wellesley College and the Faculty Director of the Madeleine Korbel Albright Institute for Global Affairs. His book, The IMF and Global Financial Crises: Phoenix Rising?, was published in 2012 by Cambridge University Press.)

Recovery in Europe?

Greece has returned to the bond market, issuing $4.2 billion of five-year bonds at an interest rate of 4.95%. The government’s ability to borrow again is a “reward” for posting a surplus on its primary budget (although the accounting that produced the surplus has been questioned). This has been viewed as a sign, albeit fragile, of recovery. Portugal has also sold bonds and hopes to exit its bailout program this spring. But what does recovery mean for these countries, and is it sustainable?

Growth” for these countries reflects a rise from a brutally harsh downturn. Greece has an unemployment rate of 26.7%, with much higher rates for its youth. Portugal’s unemployment rate of 15.3% was achieved in part by emigration.

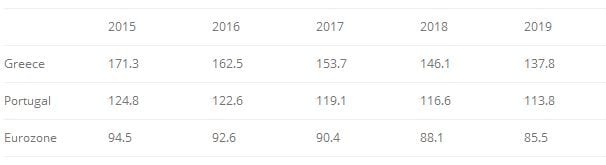

A look forward indicates that the debt that drove these countries to borrow from their European neighbors and the IMF will fall in the next five years but continue at elevated levels. The latest Fiscal Monitor of the International Monetary Fund forecasts gross government debt to GDP ratios for these countries, as well as for the Eurozone:

Even if the debt/GDP ratios above the Reinhart-Rogoff 90% threshold do not pose a threat to growth, it is noticeable that the Eurozone’s debt does not fall below it until 2018, while debt/GDP in Greece and Portugal will be in triple digits for many years.

These debt levels become more worrisome in light of fears of deflation in the Eurozone. Greek consumer prices have been falling, and inflation in the Eurozone is below its 2% target level. European Central Bank head Mario Draghi has downplayed these concerns, pointing to rising prices in other Eurozone countries. But IMF economists Reza Moghadem, Ranjit Teja and Pelin Berkman point out that even low inflation can also pose problems. Deflation and less than expected rates of inflation increase the burden of existing debt. Greece’s debt will become more of a burden if it rises in real terms. Low inflation also makes wage adjustment harder to achieve.

The ECB would (presumably) respond if the prospect of deflation became more likely. But would it be able to stave off falling prices through its version of quantitative easing? There are concerns that large-scale purchases of assets by the ECB might not be as effective as anticipated. Interest rates have already fallen and are unlikely to fall further. Moreover, the decline in borrowing costs for Greece and other sovereign borrowers may have already have factored in ECB intervention.

Draghi’s pledge in 2012 to do “whatever it takes” to protect the euro undoubtedly lowered concerns about a collapse of the Eurozone. But, as I have argued before, the confidence within the Eurozone inspired by the ECB’s powers could vanish, particularly if there were doubts about the ECB’s ability to actually accomplish whatever it takes to avoid deflation. Lower borrowing costs based on faith in the ECB will ease conditions in the Eurozone crisis countries. But they need to be backed up by improving economic fundamentals before they are seen as justified. Until then, purchasing sovereign debt is a high-risk proposition, no matter what the interest rates signal.

cross posted with Capital Ebb and Flows