In cutting through some of the media noise on today’s action form the ECB, here are a few points worth discussing.

1. The negative rate on deposits would have been far more effective a couple of years ago when the Eurozone banks’ excess reserves were a multiple of what they are now.

2. The end of sterilization of the SMP portfolio, bonds that the ECB had purchased a few years back (see discussion from Feb), will provide a boost to excess reserves. The current SMP balance is about €165bn – which is material relative to current excess reserve levels. Additional excess reserves will make the negative rate policy more effective.

3. The negative rate on deposits is sending banks into short-term periphery paper, as yields compress further.

|

| Spain’s 1y government bond yield (source: Investing.com) |

It’s important to note that excess reserves are a bit like a hot potato – you can pass them from bank to bank, but someone always gets stuck with them. That means some euro area banks will be making payments to the ECB of 0.1%.

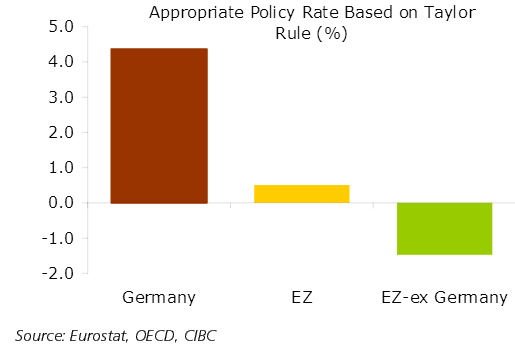

4. The cut in ECB’s main financing rate is basically symbolic. The problem with this near-zero rate is that if the ECB could set a separate rate for Germany vs. the rest of the member states, these rates would have been dramatically different. The so-called Taylor Rule, which models the “appropriate” interest rate, produces the following result.

|

| Source: CIBC |

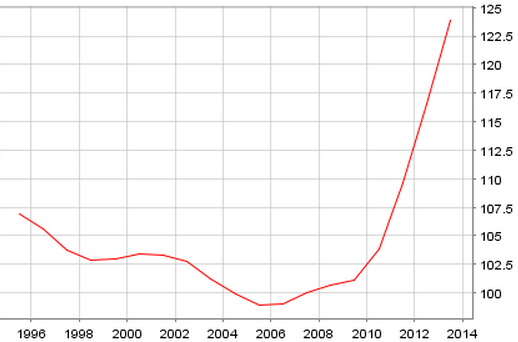

This high discrepancy maintains tight conditions in “EZ ex-Germany”, while risking asset bubbles in Germany due to a highly accommodate policy there. Here is an example.

|

| Germany; Residential property prices, New and existing dwellings; Residential property in good & poor condition; Whole country (source: ECB) |

5. The targeted approach to providing liquidity, the so-called TLTRO, is a good idea.

Bloomberg: – Financial institutions will be allowed to borrow money from the ECB equivalent to as much as 7 percent of their outstanding loans to non-financial corporations and households, excluding mortgages.

The maturity will be up to four years, priced at the ECB’s benchmark rate when the loans are taken out plus 0.1 percentage point. Banks that don’t pass the money on will be obliged to repay it after two years. The so-called targeted longer-term refinancing operations, or TLTROs, will be carried out in September and December.

From March 2015 to June 2016, on a quarterly basis, banks will be able to borrow as much as three times the amount of their net lending to euro-area companies, above a threshold set by the ECB.

This creates incentives for banks to grow their “real economy” loan books. One of the problems with the Fed’s QE program has been the weakening of loan growth (see post). Large firms and mortgage holders, who were able to refinance, certainly benefited from QE, but some of the biggest beneficiaries were asset management firms. That’s why a targeted approach could prove to have more “bang for the buck”…

6. The ABS buying program is still in the works. There isn’t sufficient amount of paper out there to have a large impact (see post), but we’ll see what the central bank cooks up. They certainly have been quite creative.

7. Markets cheered, but the impact varied by asset class. The currency markets for example had a great deal of this ECB action already priced in – and then some. The euro fell sharply on the announcements and then rebounded to finish up on the day.

|

| Source: Investing.com |

IMPORTANT: We require that any re-published posts preserve ALL embedded links to previous Sober Look and Twitter posts. Sober Look represents an ongoing discussion which relies on continuity as well as references to key external materials.

From our sponsor: