What is the optimal investment portfolio? Is it the one that contains the hottest performing stocks and funds? Actually, it’s the portfolio that perfectly represents a person’s psychology, life circumstances, financial needs, and future goals.

My latest Portfolio Report Card is for K.B., a 49 year-old U.S. Marine Officer serving overseas. He told me he considers himself a “moderately aggressive” investor and have enough money to retire comfortably is his biggest concern.

AUDIO: Ron Grades a Software Executive’s $1 Million Portfolio

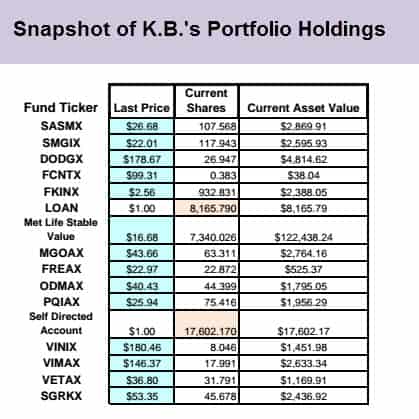

He self-manages a 401(k) retirement plan with $171,946 invested across 12 mutual funds and two individual stocks; Apple (NasdaqGS: AAPL) and Keryx Biopharmaceuticals (NasdaqCM:KERX). Does K.B.’s portfolio pass or fail? Before I assign his retirement portfolio a final grade, let’s examine it together.

Diversification

Any person that claims to have a diversified portfolio should market exposure to all the major asset classes – not just the ones they like or are momentarily hot.

K.B.’s portfolio does a good job covering major asset classes like large-cap U.S. stocks (Nasdaq:DODGX), mid-cap U.S. stocks (Nasdaq:MGOAX), small-cap U.S. stocks (Nasdaq:SASMX), bonds (Nasdaq:FKINX), and real estate (Nasdaq:FREAX). Even so, he’s not out of the woods. Why?

Since 71% of his portfolio is allocated in the MetLife Stable Value Fund – a cash preservation strategy – owning these other asset categories does little to help his overall diversification. Also, some of his holdings like MGOAX, VIMAX, SMGIX, DODGX, and VETAX are unnecessary duplication because they own the same types of stocks.|

Risk

A properly built portfolio should accurately reflect a person’s true risk tolerance along with their unique investor personality.

Although K.B. classifies himself as a “moderately aggressive” investor, his portfolio’s current design isn’t compatible with that description.

In this case, he’s got 71% in cash assets, 27% in stocks and the remaining 2% in bonds and real estate. Put another way, K.B.’s current asset mix matches the risk profile of a conservative investor with capital preservation as their main goal.

Cost

As previously mentioned, K.B.’s largest holding is the MetLife Stable Value Fund, which charges annual expenses of 0.66%. Five of his mutual funds have upfront sales loads in excess of 4% and annual expense ratios above 1%. He’s getting taken to the cleaners on cost.

Although he owns two Vanguard funds with rock bottom expenses – VINIX charges just 0.04% and VIMAX charges just 0.09% annually – the bulk of his assets are invested elsewhere in funds with substantially higher operating costs.

If he leaves his current investments in place, I estimate K.B. will forfeit in fees around $17,000 or 10% of his current portfolio. That’s a lot of money to be leaving on the table!

Tax-Efficiency

Most 401(k) plans have no problems when it comes to tax-efficiency, but not in K.B.’s case. That’s because he has an $8,100 outstanding 401(k) loan. Here’s what that means: If he terminates his job for whatever reason without paying off the full balance of the loan, the money becomes taxable income. And until he completely pays off the loan, it’ll continue to be a potential tax liability that seriously threatens the health of his retirement account.

Performance

The correct standard of an investment portfolio’s performance is how it performs relative to a blended mix of passive index funds or ETFs.

From June 2013 to June 2014, K.B.’s investment portfolio gained 14% while a portfolio of passive index ETFs that reflect a moderately aggressive investor that matches his profile gained 15.39%.

Summary

K.B.’s final Portfolio Report Card is a “D.” Unfortunately, his portfolio is not compatible with his risk profile and is overexposed to low yielding cash. Moreover, he hasn’t taken deliberate steps to minimize the cost of his mutual fund holdings.

K.B.’s outstanding 401(k) loan will be a constant tax threat until he pays it off. And his portfolio’s one-year performance trailed a basket of index ETFs, which means he would’ve been better off with the latter choice.

Portfolios with a “D” are poorly designed and have major flaws that require immediate and major changes. Hopefully, K.B. can overhaul his portfolio and get back on track.

Ron DeLegge’s Portfolio Report Card challenge stands: If your investment portfolio scores an “A”, you’ll get paid $100. Ron grades family trust accounts, 401(k) rollovers, 457 plans, 403(b), UGMA accounts, and anything posing as an “investment.”

Follow us on Twitter @ ETFguide