Labor share data going back many years was revised last week. According to these new revisions, the economy has been against the effective demand limit since the beginning of the year. With the stock markets retreating from their record highs, this should not be surprising.

Keep in mind that the updated graphs below are based on my own theory of effective demand…

The effective demand limit determines true slack in the economy. Productive capacity is not established by what we should be able to produce, but by the relative strength of demand to purchase production.

The effective demand limit says that the combined utilization rates of labor and capital will not surpass an effective labor share. Therefore, slack in the economy is determined by…

slack = effective labor share – (capacity utilization * (1 – unemployment rate)) > 0

The UT index

The UT index is a measure of the slack (Unused Total capacity of labor and capital). Here is a graph of the UT index since 1967.

The UT index wants to stay above 0%. Firms (in the aggregate) do not increase profits when slack goes negative, because firms will pay the increased cost of employing more labor and capital, instead of consumers paying that cost.

The UT index shows that slack has been at the zero lower bound since the end of 2013. It bounced on 0% in the 4thQ of 2013 and is now hovering above 0%. … So how has unemployment been able to decline in 2014 if slack is zero? Well, labor share has risen off of its low at the end of 2013. There is more relative consumer power from labor.

If labor share stays constant though, unemployment and capacity utilization will be capped. That is to say… the unemployment rate will only mildly decline, and capacity utilization will stay constant or decline. That has been a normal pattern in past business cycles.

I project that within the next 4 quarters, the UT index will start rising as it did in previous business cycles. You might wonder why slack would start increasing during a business cycle. The reason is that a recession is forming, profit rates are dropping and firms start employing less labor and capital.

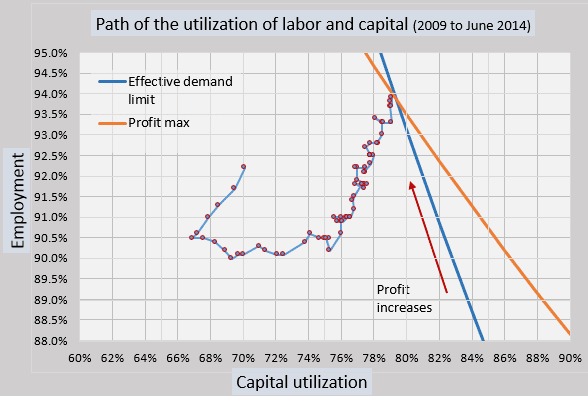

Limit on Employment and Capacity Utilization

The down-sloping lines in this graph represent profit maximization limits of effective demand. (monthly data)

The scatter plot of employment with capacity utilization shows increasing profits moving Northeast. Then, when the plot hits the limit lines, profits will increase by moving Northwest along the limit lines. I project that if employment rises, we will eventually see a corresponding decline in capacity utilization, as long as effective labor share stays around 74.5%. If labor share rises, the limit lines will move to the right allowing greater employment of labor and capital. Firms have to sacrifice some of their profits though to raise labor share.

Productivity

The pattern in the past is that productivity stalls against the effective demand limit (where real GDP equals Effective demand.) It is happening again. The last 2 quarters of 2013 showed productivity started to rise. But the first two quarters of 2014 show productivity dropped back to its previous trend. Productivity is so far bound within the effective demand limit.

Path of Real GDP

The green line shows Real GDP rising since the crisis in terms of labor and capital utilization. Even though many think real GDP grew a lot in the 2ndQ of 2014, it is still close to the polynomial trend line. The red line of effective demand is bumping against real GDP. The pattern in the past says that real GDP will start rising up near the red vertical line as the utilization of labor and capital (TFUR) stops rising on the x-axis. The process warns that a recession is forming. I project that this vertical movement will be noticeable within 4 more quarters.

Conclusion

With the new revisions of labor share, the economy is reaching the effective demand limit. The projection going forward is that there is little true slack in terms of labor and capital. The business cycle is peaking. Profit rates are peaking. The stock market has little true upside left. I suspect the next year will be troubling to those who do not see the effective demand limit.