There is nothing remotely “normal” about the echo-bubble’s rise, and we can anticipate that its deflation will be equally abnormal.

Conventional wisdom on the resurgence of the housing markets takes one of two paths:

1. Housing is not in a bubble, it is merely returning to “normal”

2. Housing is bubbly in some markets, but prices will continue to rise

Here’s an alternative view: housing is in an echo-bubble that’s popping.Courtesy of the excellent Market Daily Briefing, here are some charts that make the case that the housing echo-bubble was just another Federal Reserve-induced speculative asset bubble that’s popping, like every other speculative bubble in recorded history.

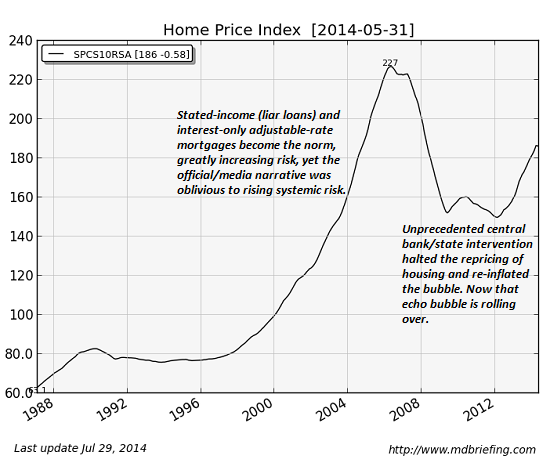

First up: home prices, as measured by the Case-Shiller Price Index. Note the near-perfect symmetry of the echo-bubble: it has taken roughly the same time-span to inflate and reach a top as the first housing bubble from January 2004 to its peak 2+ years later.

The echo-bubble has topped out at about 50% of the decline from the primary bubble top to the trough in 2012.

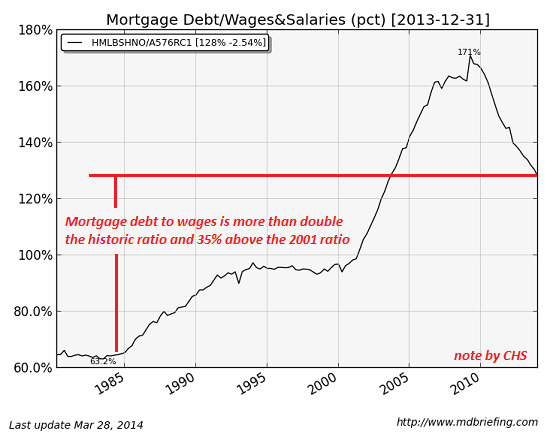

The distorted fundamentals of the echo-bubble are revealed in this chart of mortgage debt to wages. Current levels of mortgage debt are double historic levels, and 35% above the level of 2001, when the primary housing bubble lifted off.

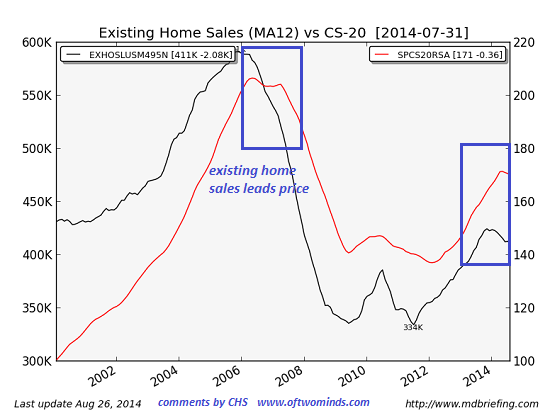

The third charts tells us the echo-bubble is popping. Note that housing sales lead price by about six months: sales started falling in late 2005, and prices rolled over in mid-2006.

Housing sales rolled over in December 2013, and sure enough, prices are starting to weaken in many markets.

The echo-bubble doesn’t pass the sniff test as a “normal” housing recovery.Exhibit #1: who’s buying and who’s not buying:

1. Marginal buyers using 3% down-payment FHA/VA loans who wouldn’t qualify for conventional mortgages. The risk of marginal borrowers defaulting is high, a reality reflected in FHA’s default rate:

When lending sources dried up during the financial crisis, the FHA propped up the housing market by insuring the lenders it works with against losses and enticing them back into the market. But the FHA’s default rate shot up as its loan volume expanded, depleting its cash reserves to levels below what is required by law. In September 2013, the FHA tapped taxpayer money to cover its losses for the first time in the agency’s 80-year history.

2. Who’s not buying: Upper-Income, Educated, Married with Children, and Still Not Buying:Declining Homeownership among “Prime” First-Time Home Buying Candidates (Fannie Mae Housing Insights, Volume 4, Issue 4)

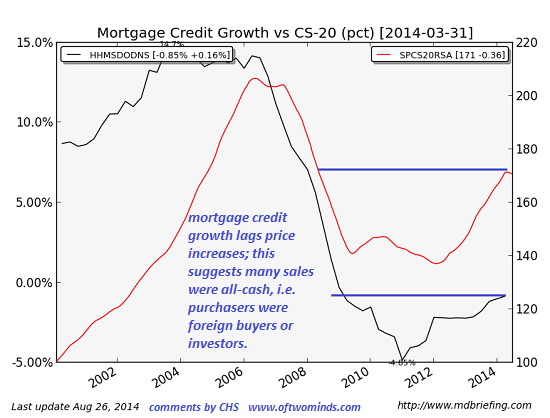

3. The dominance of all-cash buyers–generally investors (those close to the money spigots of the Fed’s free money for financiers) and foreign buyers.

Note the difference between mortgage credit expansion, which has lagged price gains. This suggests many of the sales (about 35% in many hot markets) were all-cash purchases that did not require a mortgage

Take away the Fed’s zero-interest rate policy (ZIRP), its free money for financiersand foreign buyers seeking a safe haven for their hot money, and what’s left of the supposedly “normal” housing recovery? Not much.

There is nothing remotely “normal” about the echo-bubble’s rise, and we can anticipate that its deflation will be equally abnormal.

How do we know when an asset class is in a bubble? When everyone who stands to benefit from the continuation of the expansion declares it can’t be a bubble.