Every so often, lost amongst the ticker tape and chyrons, a company makes a stealth move to propel them forward.

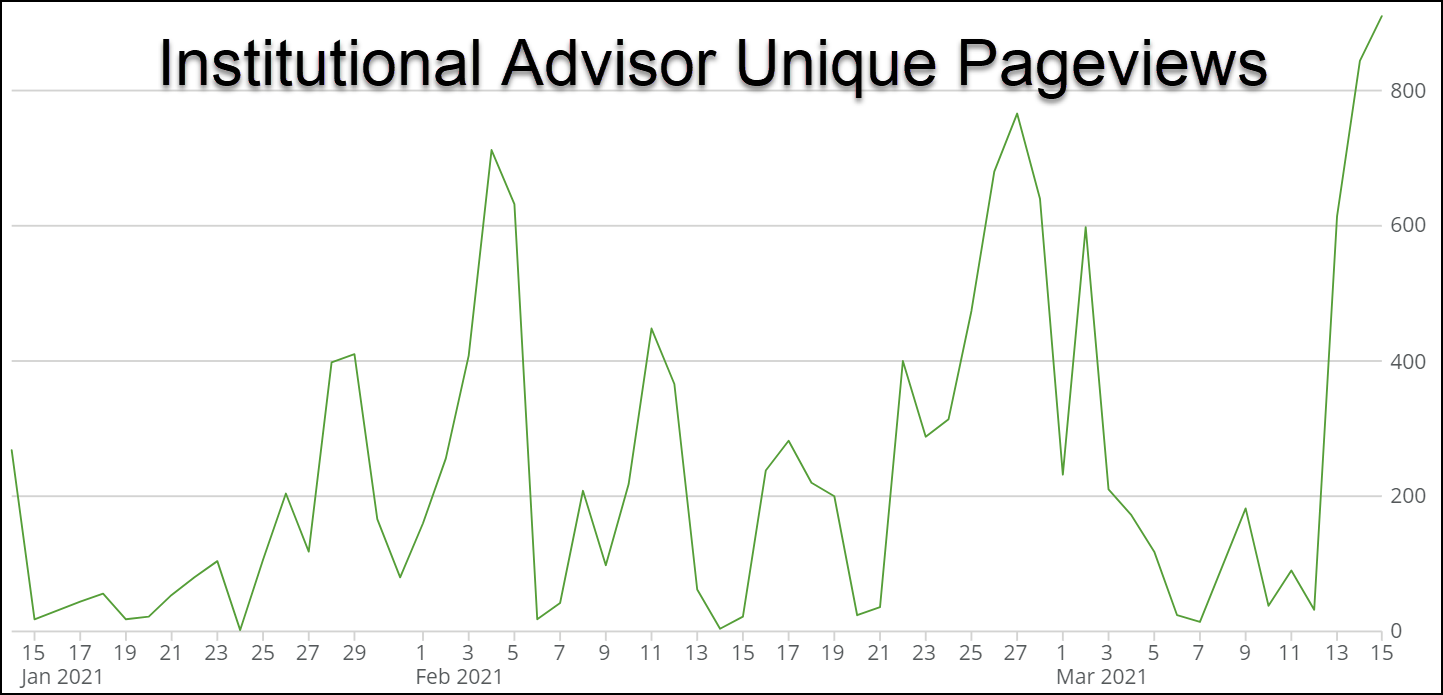

But our TrackstarIQ data spotted some BIG INTEREST in Peloton (PTON).

The question is…why?

Why are institutional advisors reading up on this stock?

The answer isn’t so simple.

That’s why we combed through the data and newsfeeds to put together a comprehensive look at the Peloton story.

But we’re taking it a step further, marrying qualitative and quantitative analysis – fundamental storylines with technical chart trading.

And we think we have a pretty good idea of what’s going on and where the stock might be headed.

See if you agree.

Does the news matter?

One of the first questions anyone should ask when they read a headline is this…

Does this news matter?

We’re not talking about over the next 24 hours (unless you trade short-term).

For investors, we want to know if this news materially changes the outlook for the company.

In this case, Peloton (PTON) announced a partnership with Adidas. However, there were conflicting news releases about whether this was a ‘potential’ or ‘done’ deal.

Considering the company puts out over $1 billion in revenue annually, it’s hard to see this moving the needle.

Still, clothing and branding certainly deepen the relationship with their current customers.

What mattered more to markets happened over a week earlier.

On March 8th, Peloton announced they would be entering the Australian market in the second half of 2021.

That IS big news.

Here’s why.

Australia has around 10 million potential consumers that fit within its possible demographics. That’s not huge, considering they already have 4.4+ million members.

However, it opens the door to the Asian market, which holds immense potential, as you can probably imagine.

A look at their financials

Before we take a look at their financials, let’s quickly discuss how the company operates.

Peloton creates fitness products, notably their bikes, that consumers buy. These connect to a network of classes and content through a subscription service.

The key here is their content. Peloton creates an almost cultlike following with its members. It’s more than just a fitness brand. It’s a lifestyle.

They bring in celebrities from Beyonce to create music partnerships with the Elvis Presley Estate to Sony Music.

Generally, the company doesn’t make much, if anything, off the initial product sale. Their high margin revenues come from subscriptions. You can buy a connected subscription with their product or sign up for a digital subscription (at a higher price) without one.

Now, let’s look at some key stats worth noting out of their last quarterly report:

- Q2 revenue up 128% over the prior year

- Connected fitness subscriptions grew 134%

- Digital subscriptions grew 472%

- Connected fitness gross margin was 35.3%

- Subscription gross margin was 60.3%

These numbers illustrate the enormous growth as well as the lucrative margins provided by their subscriptions.

This is also a great example of why entrepreneurs love to develop apps. After the initial creation costs, it sort of goes on autopilot.

What institutional advisors care about

Institutional advisors look at an investment in terms of years, not months. They can’t go in and out of stocks willy-nilly. Transaction costs would skyrocket, not to mention, it would require immense staffing resources.

When they evaluate a company, they look at its POTENTIAL.

Potential is a loaded word and doesn’t mean the same thing to everyone.

However, most long-term investors appraise to areas with a critical eye: growth and profitability.

Yes, you can make money with a company like RR Donnely (Yellow Pages) that fought declining revenues over time.

And yes, you can make money with a company that takes decades to turn a profit…like Amazon.

Nevertheless, a company like Peloton that turns a profit AND expands revenues at triple digits presents an ideal candidate.

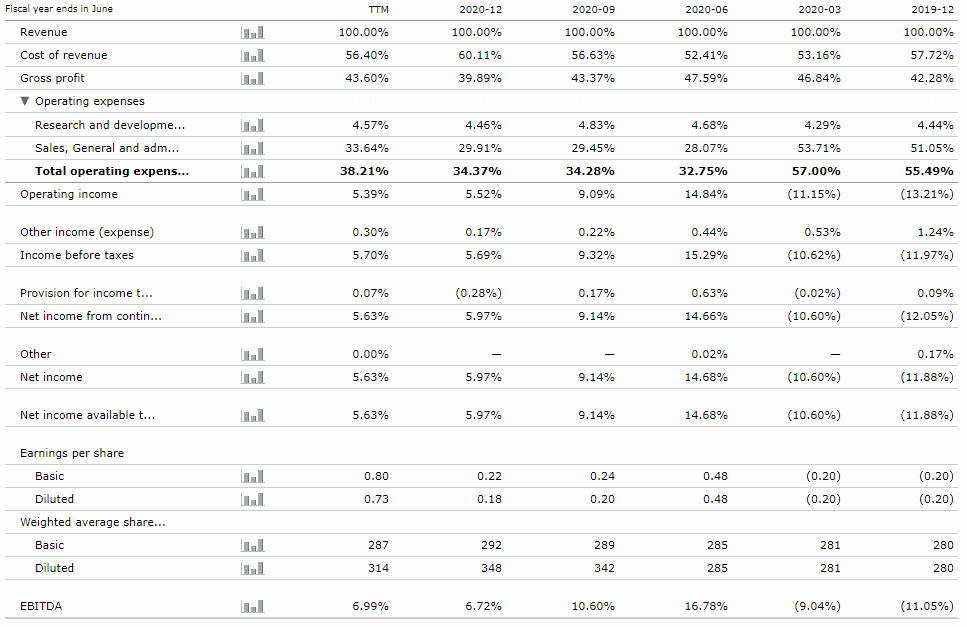

Peloton managed to turn a profit in the last year almost exclusively through a drop in selling, general and administrative expenses (SG&A).

Source: Morningstar PTON Quarterly Financials

Now, the stock isn’t cheap by traditional valuation metrics. Price to earnings ratio comes in at a lofty 239x. Price to cash flow sits at 146x. Even price to sales is 7.46x.

However, their forward (estimates for the future) price to earnings ratio is 116x. And expectations are earnings will more than double by next year.

Compare that to the S&P 500 P/E ratio is currently 27x. If PTON grew earnings by 100% each year, it would take about 4-5 years at the current price to get to the same valuation as the market.

Tune in tomorrow for part 2 of this series on Peloton – charts and technical analysis!