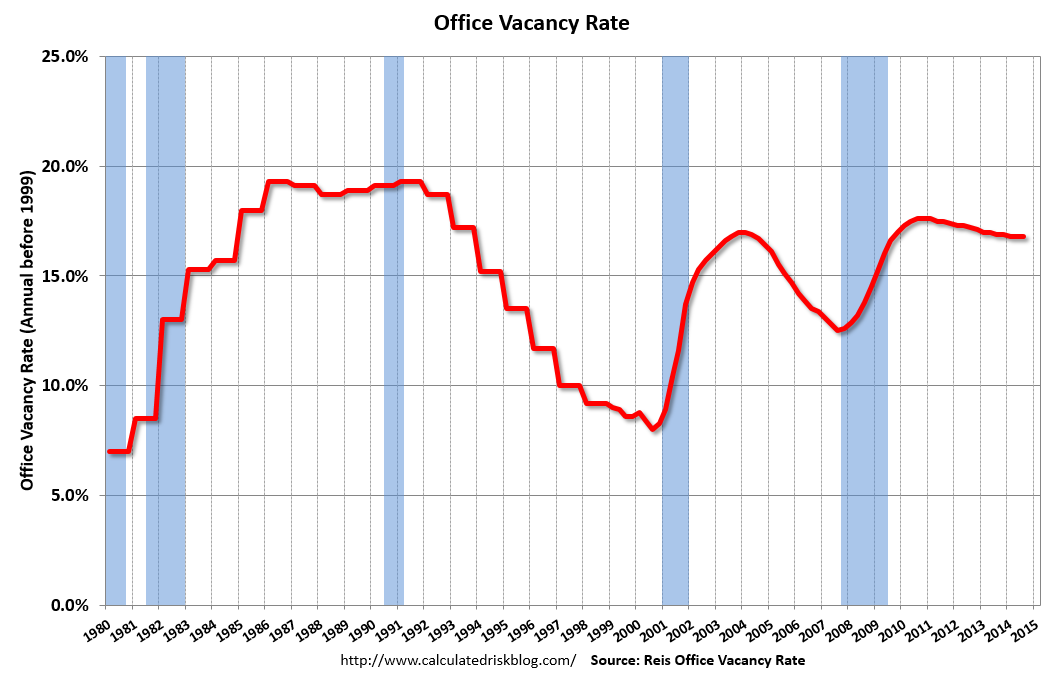

Reis released their Q3 2014 Office Vacancy survey this morning. Reis reported that the office vacancy rate was unchanged in Q3 compared to Q2 at 16.8%. This is down slightly from 16.9% in Q3 2013, and down from the cycle peak of 17.6%.

From Reis Senior Economist Ryan Severino:

The national vacancy rate once again held steady, registering 16.8% for the third consecutive quarter. Although this is superficially alarming, a few qualifications are necessary and important. First, net absorption technically outpaced new construction once again. However, much like last quarter, the difference was not sufficient enough to push the vacancy rate downward. Nonetheless, it is important to note that demand is not evaporating ‐ it is simply not producing a declining vacancy rate in recent quarters. Second, as we have observed in the recent past, construction and net absorption remain linked to each other due to the ongoing preleasing requirement in place for new construction financing. That has a tendency to keep supply and demand roughly in balance during weak recoveries such as this one when there is relatively little demand for existing inventory.

Third, this pattern is not without precedent. Something similar occurred just last year. The national vacancy rate was identical during the first three quarters of 2013 before declining again during the fourth quarter. Therefore, this pause in vacancy compression needs to be examined in the proper context ‐ it is not signaling that the market recovery is going to reverse and vacancy rates will soon begin increasing. However, the unchanged vacancy rate serves as a stark reminder that five years removed from the advent of economic recovery in the United States, the office market recovery remains in early stages. If the labor market recovery continues its acceleration, this will change, but through the third quarter of this year its struggles continue.

emphasis added

On absorption and new construction:

Net absorption increased by 7.157 million square feet during the third quarter. This is a rebound from last quarter’s 3.171 million SF. Although this is far from a healthy level of demand, it is back closer to the trend in net absorption that has occurred in recent quarters. Therefore, last quarter’s weak reading appears to be an anomaly and the longer‐term trend in increasing net absorption, though relatively tepid, remains intact. The ongoing improvement in the labor market will serve as a catalyst for net absorption in the coming quarters. New construction totaled 4.791 million square feet during the third quarter. Construction levels remain far below those indicative of a healthy market environment.

On rents:

Asking and effective rents both grew by 0.4% during the third quarter. This is a slight deceleration from last quarter’s performance for both rent metrics. Nevertheless, asking and effective rents have now risen for sixteen consecutive quarters. Moreover, we continue to see modest but ongoing acceleration in rent growth over time. Asking rent growth was 1.6% during 2011, 1.8% during 2012, and 2.1% in 2013, and 2.5% over the prior 12 months ending with the second quarter of this year. During the third quarter, the 12‐month change in asking rent increased just slightly to 2.6%. Given how elevated the national vacancy rate remains, we should not expect much acceleration in rent growth until the vacancy rate declines to a more conducive level, hundreds of basis points below the current 16.8% rate.

Click on graph for larger image.

Click on graph for larger image.

This graph shows the office vacancy rate starting in 1980 (prior to 1999 the data is annual).

Reis reported the vacancy rate was unchanged at 16.8% in Q3, and was down from 16.9% in Q2 2013. The vacancy rate peaked in this cycle at 17.6% in Q3 and Q4 2010, and Q1 2011.

There will not be a significant pickup in new construction until the vacancy rate falls much further.

Office vacancy data courtesy of Reis.