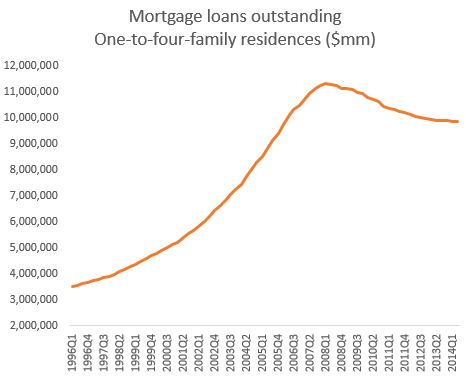

The availability of residential mortgage bonds in the United States has been shrinking. Private mortgage securitization markets are nonexistent since the financial crisis and the GSEs are not generating enough new supply. The reason of course is the lack of mortgage loan growth in the US. While corporate, consumer, and commercial real estate loan balances are rising, residential loans have stalled.

|

| Source: FRB |

On the supply side here are some reasons for the weakness in mortgage loan origination:

Scotiabank: – … banks have been more stringent with lending standards since they were forced to buy back soured mortgages from Fannie Mae and Freddie Mac [putbacks] which led to significant losses in 2012 and 2013. Then, last year, Fannie Mae Fannie Mae stopped guaranteeing mortgages with down payments of 3% or less. Plus, in early January, the Consumer Financial Protection Bureau implemented its Ability-to-Repay and Qualified Mortgage Standards rules [see post] which tightened regulation surrounding mortgage securitization. In a special section of the Federal Reserve’s July Senior Loan Officer Survey, 36% of respondents said their approval rate was lower than it would be without the rule for those with lower credit scores (less than 680), and 31% of respondents replied that it was lower for those with higher credit scores (greater than 680).

Add to that the recent increases in FHA mortgage insurance premiums (needed to replenish the FHA reserves – discussed here) for high LTV loans. Many potential first-time buyers with no ability to come up with sufficient down payment are shut out of the market.

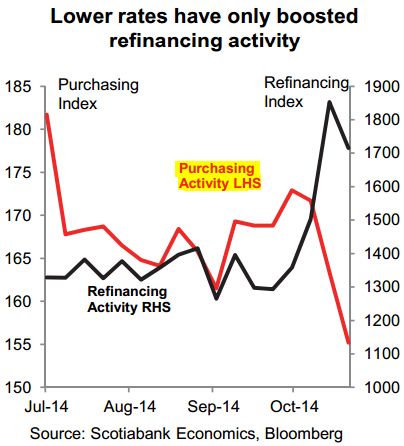

At the same time the demand for mortgage loans has weakened, with the recent rate drop only impacting refi activity. Part of the reason is the rise in property prices over the past couple of years which also prices may first-time buyers out of the market.

|

| Source: Source: Scotiabank |

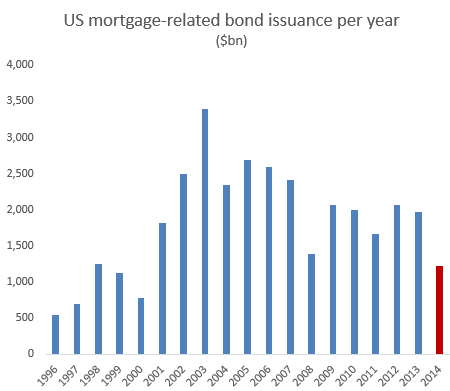

As a result of these trends, US mortgage bond market continues to shrink. The amount issued this year is on target to be the lowest since 2000.

|

| 2014 figure is based on annualized Q1-Q3 issuance (source: SIFMA) |

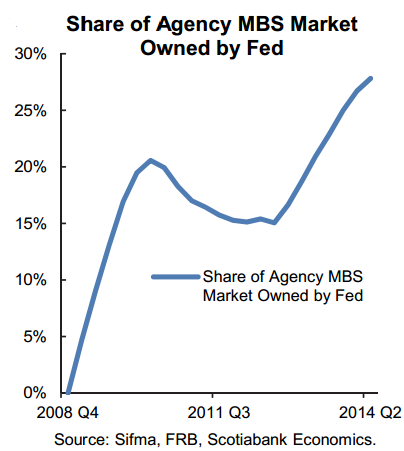

To exacerbate the situation, over a quarter of outstanding MBS bonds has been permanently locked up on the balance sheet of the Federal Reserve. This takes a significant chunk of an already shrinking market out of private hands. And in spite of the securities purchases ending, the Fed will continue to buy MBS to compensate for prepayment amortization.

|

| Source: Scotiabank |

_________________________________________________________________________

Sign up for our daily newsletter called the Daily Shot. It’s a quick graphical summary of topics covered here and on Twitter (see overview). Emails are distributed via Freelists.org and are NEVER sold or otherwise shared with anyone.

From our sponsor: