Add these factors up and we conclude there is no visible price limit on oil after supply falters.

I’ve been discussing the concept of an Oil Head-Fake since 2008, most recently inThe Oil Head-Fake: The Illusion that Lower Oil Prices Are Positive (September 29, 2014) Oil: One Last Head-Fake? (May 9, 2008)

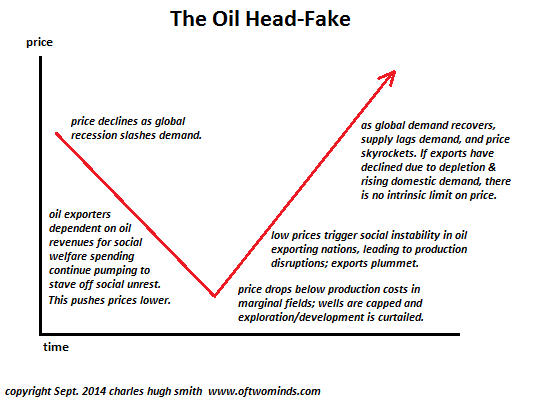

The basic idea is straightforward: as global demand slackens, oil producers are incapable of reducing supply due to their dependence on oil revenues. This leads to oversupply which further depresses prices, to the point that marginal wells are shut off and costly exploration-development projects are shelved.

This process is far from orderly, as the low prices destabilize oil-dependent governments and regions. Geopolitical turmoil is only half the story; the immense mountain of debt that’s been built on the collateral of oil collapses as cash-starved borrowers default on bonds and loans. This meltdown of oil-based debt then destabilizes an increasingly fragile global financial system.

Supply can be turned off easily enough, but it can’t be expanded as easily. Costly deepwater wells that were shelved in the price bust can be restarted, but it takes many years to bring these hyper-expensive projects online.

Meanwhile, existing production declines without constant injections of capital and expertise. Contrary to popular conception that oil flows for decades without having to do anything other than poke a hole in the ground, oil fields need huge investments of capital to maintain high production: carbon dioxide or water must be injected into the wells, and so on.

So even if fields are kept online through the price bust, their production will decline as capital spending dries up.

The end result of the price bust is impaired supply: impaired by depletion, impaired by reduced investment, impaired by the collapse of oil-based debt.

Even if demand only remains constant, the price of oil will rise as supply falls. And with several billion people aspiring to the energy-intensive middle-class lifestyle of the developed world, we can anticipate global demand rising even if it stagnates in the developed world.

The price drop is a head-fake: it doesn’t usher in a new era of permanently cheap oil. Rather, it unleashes dynamics that impair supply on multiple levels: geophysical, geopolitical, demographic and financial.

When supply cannot be jacked up to meet demand, prices will rise. As I have noted before, demand is somewhat elastic in the developed world–business meetings can be done online, vacations can be postponed, car pools can reduce single-driver trips, and so on.

In the developing world, the entrepreneur who uses his motorcycle to earn his livelihood doesn’t have an alternative; if the price of a liter of fuel doubles, he has no choice but to pay it.

In other words, as the number of people who depend on oil rises, the elasticity of demand declines accordingly. Higher prices may not reduce demand in the way conventional economic models expect.

The oil-exporting nations have introduced another disruptive dynamic: fuel subsidies for their domestic markets. These fuel subsidies are political bribes to the citizenry chafing under the poverty and powerlessness of life in oil-financed kleptocracies.

Simple supply and demand dictates the destabilizing result of these generous subsidies: the cheap fuel is squandered and demand soars. Many of the nations that heavily subsidize fuel are facing the evaporation of their oil exports as domestic demand absorbs more of their total production.

This dynamic will force kleptocracies into a double-bind: if they end the subsidies, they face destabilizing domestic unrest. If they continue the subsidies, they lose their oil exports and income needed to service their debt, fund their welfare states and armed forces.

Either way, the kleptocracies implode, and in the resulting turmoil capital investment in their oil production will plummet, further reducing supply.

Add these factors up and we conclude there is no visible price limit on oil after supply falters. If I need two liters of petrol to make money for food today, I will pay whatever it takes. $200/barrel oil is no impediment because I need those few liters to earn my livelihood.

When oil prices move high enough that alternatives are clearly bargains, then demand will face headwinds. But all the alternatives require capital, and if not capital, then credit, and that is precisely what will be impaired by the collapse of the global credit engine as the oil head-fake and various asset bubbles implode.

How to forge a career in a dysfunctional economy:

Get a Job, Build a Real Career and Defy a Bewildering Economy,

a mere $9.95 for the Kindle ebook edition and $15.47 for the print edition.