The Census Bureau reported that overall construction spending decreased in November:

The U.S. Census Bureau of the Department of Commerce announced today that construction spending during November 2014 was estimated at a seasonally adjusted annual rate of $975.0 billion, 0.3 percent below the revised October estimate of $977.7 billion.

Private spending increased and public spending decreased in November:

Spending on private construction was at a seasonally adjusted annual rate of $697.7 billion, 0.3 percent above the revised October estimate of $695.7 billion. Residential construction was at a seasonally adjusted annual rate of $352.7 billion in November, 0.9 percent above the revised October estimate of $349.6 billion. Nonresidential construction was at a seasonally adjusted annual rate of $345.0 billion in November, 0.3 percent below the revised October estimate of $346.1 billion. …

In November, the estimated seasonally adjusted annual rate of public construction spending was $277.3 billion, 1.7 percent below the revised October estimate of $282.0 billion.

emphasis added

Note: Non-residential for offices and hotels is increasing, but spending for oil and gas is generally declining (up slightly in November from October). Early in the recovery, there was a surge in non-residential spending for oil and gas (because prices increased), but now, with falling prices, oil and gas is a drag on overall construction spending.

As an example, construction spending for lodging is up 11% year-over-year, whereas spending for power (includes oil and gas) construction peaked in mid-2014.

Click on graph for larger image.

Click on graph for larger image.

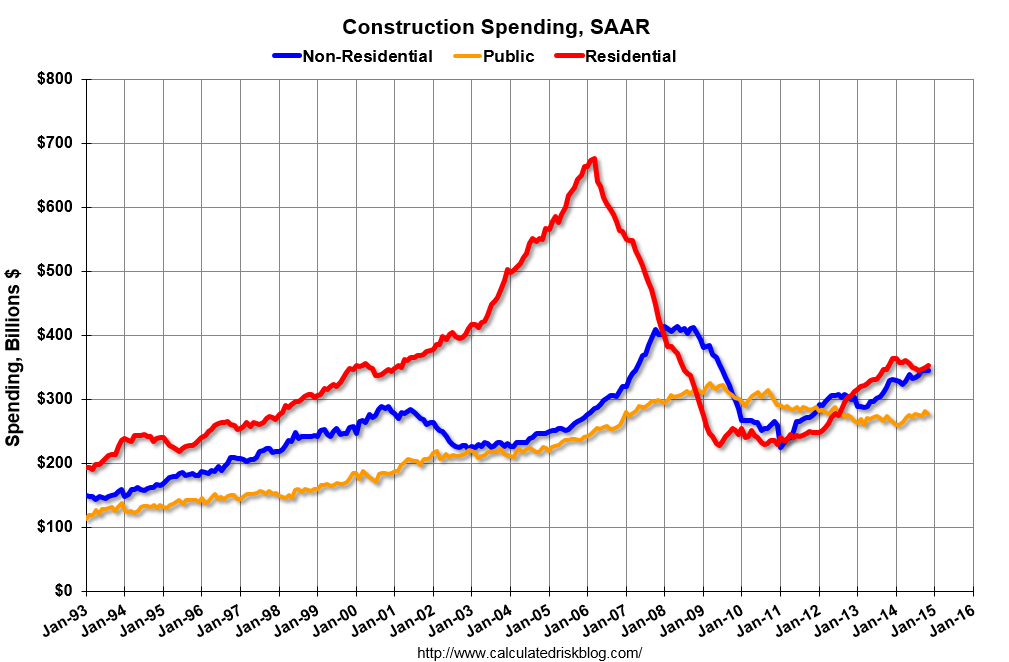

This graph shows private residential and nonresidential construction spending, and public spending, since 1993. Note: nominal dollars, not inflation adjusted.

Private residential spending is 48% below the peak in early 2006 – but up 54% from the post-bubble low.

Non-residential spending is 18% below the peak in January 2008, and up about 53% from the recent low.

Public construction spending is now 15% below the peak in March 2009 and about 5% above the post-recession low.

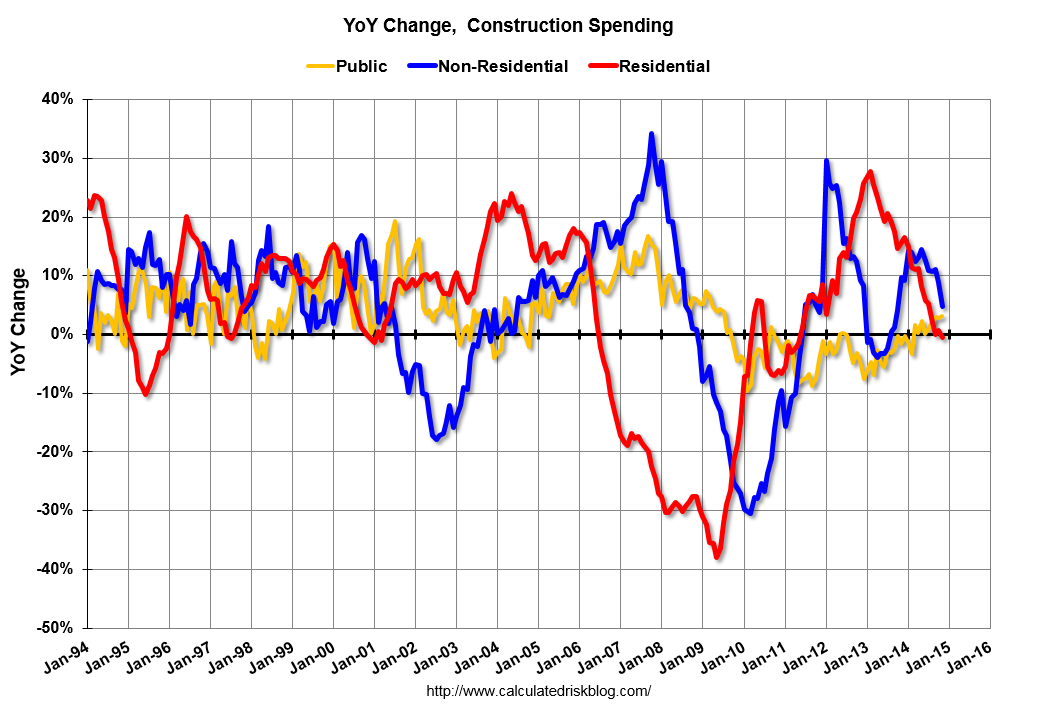

The second graph shows the year-over-year change in construction spending.

The second graph shows the year-over-year change in construction spending.

On a year-over-year basis, private residential construction spending is now unchanged. Non-residential spending is up 5% year-over-year. Public spending is up 3% year-over-year.

Looking forward, all categories of construction spending should increase in 2015. Residential spending is still very low, non-residential is starting to pickup (except oil and gas), and public spending has probably hit bottom after several years of austerity.

This was below the consensus forecast of a 0.5% increase, however there were some upward revisions to spending in September and October.