Black Knight Financial Services (BKFS) released their Mortgage Monitor report for November today. According to BKFS, 6.08% of mortgages were delinquent in November, up from 5.44% in October. BKFS reported that 1.63% of mortgages were in the foreclosure process, down from 2.50% in November 2013.

This gives a total of 7.71% delinquent or in foreclosure. It breaks down as:

• 1,925,000 properties that are 30 or more days, and less than 90 days past due, but not in foreclosure.

• 1,163,000 properties that are 90 or more days delinquent, but not in foreclosure.

• 829,000 loans in foreclosure process.

For a total of 3,917,000 loans delinquent or in foreclosure in November. This is down from 4,497,000 in November 2013.

Black Knight had several comments on the “spike” in delinquencies in November:

• November’s spike in delinquencies was the largest month-over month increase (for any month) since November 2008

• Much of the increase seems to have been calendar-driven; two federal holidays (Veterans Day and Thanksgiving) and the last two days of the month being a weekend resulted in just 18 possible payment processing days

• The five largest M/M delinquency rate increases over the last 7 years have all occurred in months ending on a Sunday

If this was just seasonal (and calendar related), then delinquencies should decline solidly in December.

Click on graph for larger image.

Click on graph for larger image.

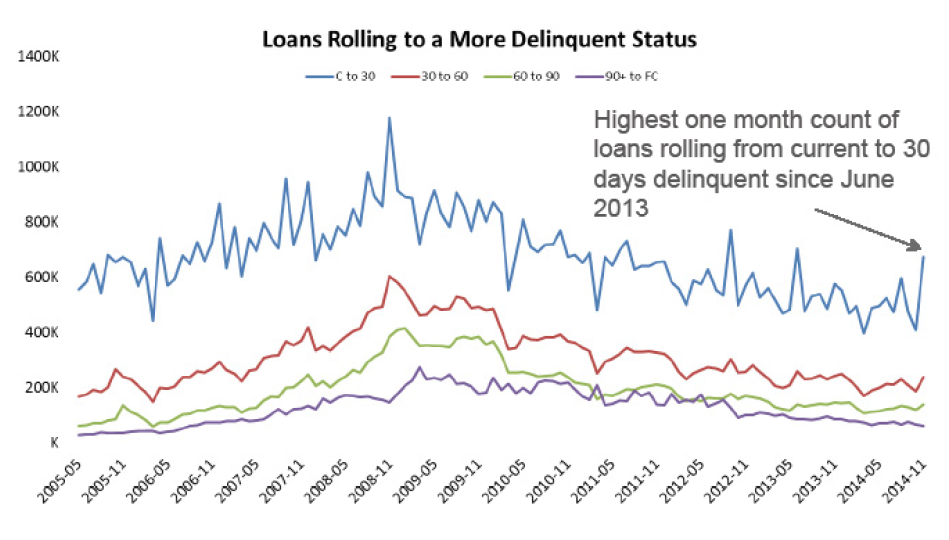

This graph from Black Knight shows the number of loans rolling to a more delinquent status. There was a big spike from current to 30 days delinquent, and that should reverse if seasonal.

From Black Knight:

• Increased roll-rates were seen across all early stage delinquency categories (i.e., loans rolling from current status to 30-days delinquent, 30 to 60 days delinquent, etc.)

• November saw the highest one month count of loans rolling from current to 30-days delinquent since June 2013

• While early stage delinquent categories saw increased roll-rates, rolls from delinquent to foreclosure status were still down

There is much more in the mortgage monitor.