- Global bond bubble poses systemic risk to financial system

- FT warns that a June rate hike could put fixed-income funds under severe pressure

- Fed’s Bullard warns of “dire consequences” of developing asset price bubbles

- UK fund managers worried about “inflated value of bonds”

- Regulators talk tough but have wavered since 2011

- Mutual fund markets have “ballooned” since 2008

- “Gates” or capital controls that limit investor withdrawals in troubled times are likely

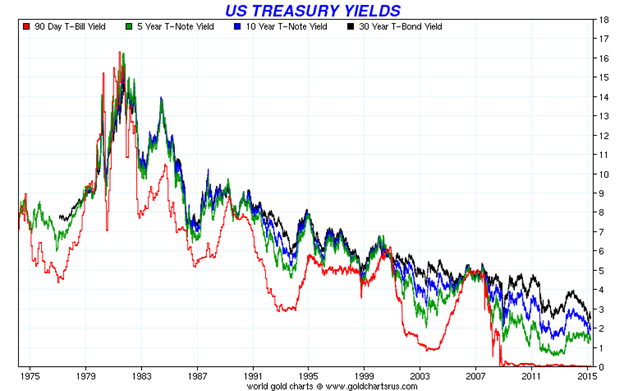

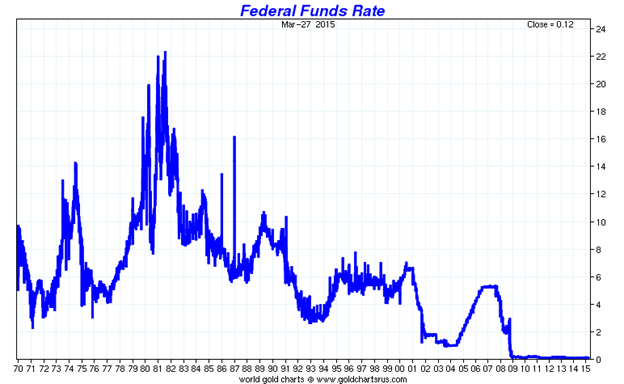

The Financial Times (U.S. edition) warned today about the growing global ‘bond bubble’ and potential severe problems in the bond markets and ‘systemic risk’ which may come to a head in June if the Federal Reserve raises interest rates.

In an article entitled “Time to find out hard way if asset management is systemic risk“, it quotes James Bullard from the Fed warning of “dire consequences” due to developing asset price bubbles if the Fed does not raise rates soon.

It refers to fact that “80 per cent of fund managers surveyed by CFA UK, a financial standards body, signalled worries about the inflated value of bonds.” It discusses how plans have been in the making to manage risks posed by certain funds by “boosting supervision of asset managers.”

For example, earlier this month “the Financial Stability Board and the International Organisation of Securities Commissions promised a plan to identify systemically important funds and contain their risks.”

The FT explains that such regulation was requested by the G20 at the end of 2011. The FT warns that the plan to make a plan – which will not be operational until early next year – will come too late to deal with the expected Fed rate hike.

A report published this month by Morgan Stanley and consultants at Oliver Wyman argues that “the closest parallel to today’s scenario occurred in 1994, when an increase in Fed rates was followed by a 5 per cent outflow from fixed-income funds.”

Today such funds are holding roughly 7 per cent of their assets in cash with which to weather potential outflows. However, the article warns that “many bond watchers are nervous that the fundamental changes in the financial world make historical parallels misleading”, particularly the “scale of the market”.

U.S. mutual funds which make up half of the global total have doubled to $15 trillion since 2008.

“Since that 1994 Fed rate rise, the US’s bond-invested mutual funds have grown sixfold to more than $3 trillion today.”

Since 2000, the global bond markets size has nearly tripled in size. Today it is worth more than $100 trillion and it is backed by and intertwined with the gargantuan $550 trillion plus derivatives market.

It continues

“Expanded markets might normally be more liquid, but not this one. Thanks to the crisis and post-crisis regulation, investment banks no longer fulfil the same kind of market-making role they used to. At a time of volatility and potential large-scale selling, the absence of such a buffer is likely to add to the downward pressure on prices.”

Downward pressure on prices will mean higher interest rates – potentially sharply and rapidly higher.

This perceived weakness has caused what the FT describes as “global policy makers” to designate some larger funds and the companies that run them as “Systemically Important Financial Institutions” – SIFIs – along with some banks and insurers.

“So bank-style capital charges for asset managers now look unlikely.”

“Gates” that limit investor withdrawals from a fund in troubled times are a possibility. Stress tests, focused on funds’ liquidity positions, seem probable. And standardised disclosures of cash and hidden leverage (through derivatives exposures) are also expected.”The developing bail-in regime also poses risks to investors in bonds who could find their investment “bailed in.”

“Gates” are capital controls that would make bond funds less liquid and pose risks to investors and pensioners.

The FT suggests that these measures will come too late:

“With a Fed rate rise expected as early as June, the world will soon find out the hard way whether the asset management industry is a systemic risk or not.”

Investment managers are now over allocated to bonds due to their perceived safe haven status. Conversely, gold remains under allocated to in investment and pension portfolios globally. The majority of investment and pension funds having no allocation to gold whatsoever.

Gold will again act as a hedging instrument when safe haven bonds come under pressure in the coming months and the global bond bubble bursts.

Must read research on developing bail-in regimes including world’s top 50 banks here:

Protecting Your Savings In The Coming Bail-In Era

From Bail-Outs to Bail-Ins: Risks and Ramifications

MARKET UPDATE

Today’s AM fix was USD 1,179.25, EUR 1,098.84 and GBP 797.95 per ounce.

Yesterday’s AM fix was USD 1,187.40, EUR 1,095.01 and GBP 800.36 per ounce.

Gold in USD – Q1, 2015 – (Thomson Reuters)

Gold dropped 1.1 percent or $13.20 and closed at $1,185.50 an ounce yesterday, while silver lost 1.42 percent or $0.24, closing at $16.71 an ounce. Overnight in Singapore, gold prices fell marginally to touch a low of $1,179 per ounce but in London gold prices have eked out small gains.

Gold looks set for a third quarterly decline, though as it is only down by $2 since the close on December 31st 2014 and it will be interesting to see if it closes lower. Bullion banks may wish to “paint the tape” and ensure a lower quarterly close to keep animal spirits in the gold market muted and encourage momentum traders to go short.

Silver prices are again outperforming and are up by over 5% in dollar terms, from $15.66 to $16.60 per ounce, and more in sterling and euro terms.

Platinum is down 6.6% and palladium is this quarter’s biggest faller among the precious metals, down 7.1%.

Gold prices in sterling and particularly euros has seen strong gains in the quarter and we believe that this is a forerunner to higher gold prices in dollar terms this year.

Updates and Award Winning Research Here