This is one of those stories that gets more amazing the further you dig into it. Seems that while Chicago descends into a very public, front page news bankruptcy, Kentucky is, dollar for dollar, screwing up even more badly:

State pension funding level drops again, to 17 percent

(Kentucky.com) – The $16 billion Kentucky Retirement Systems on Thursday lowered the rate of investment return it assumes state pension assets will earn, which means funding levels for two tax-subsidized systems — ranked among the nation’s worst — fell even further.

For the next state budget, the change means lawmakers must find tens of millions of extra dollars to keep the retirement systems afloat. The state’s annual recommended contribution to KRS already was expected to hit $880 million.

“We’re in a disastrous cash position. We need help immediately from the next governor and the legislature,” said Jim Carroll, a member of an advocacy group called Kentucky Government Retirees. “We’re in a fund that can’t afford any more market losses. There’s no cushion left. What happens if the market crashes is, we go flat busted, and then maybe a judge has to step in and order the state to make payments.”

The KRS board of trustees voted to drop the assumed rate of return from 7.5 percent to 6.75 percent for two of the pension funds the agency oversees, the Kentucky Employees Retirement System (Non-Hazardous), which includes 120,595 state workers and retirees, and the State Police Retirement System, which includes 2,379 active and retired troopers.

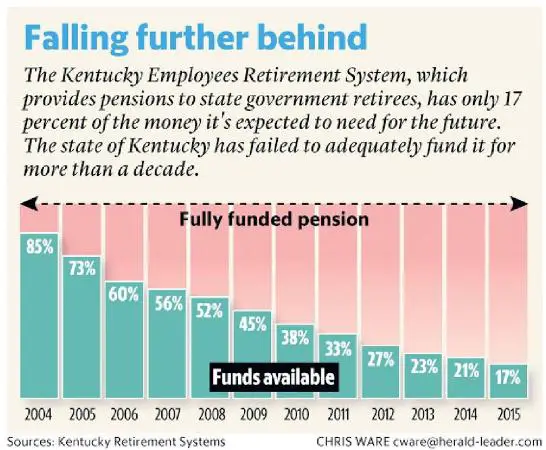

Consequently, KERS now has only 17 percent of the money it’s expected to need to pay promised benefits, down from the 19 percent announced just last month, and it faces $10.9 billion in unfunded liabilities, as compared to the previous sum of $10 billion. SPRS’ funding level now stands at 31 percent, down from last month’s 33 percent, and it must cover a $542 million gap in coming years, up from $485 million.

The County Employees Retirement System, which includes local government workers and retirees, is in better shape financially, with $6.4 billion in pension assets and a 60 percent funding level. CERS can continue to make substantive, long-term investments that produce higher returns over time, unlike cash-strapped KERS and SPRS, so its assumed investment return will remain at 7.5 percent, KRS officials said.

KRS previously lowered the assumed rate of return for all of its funds to 7.5 percent in 2014, down from 7.75 percent, which seemed unrealistically high, given the systems’ actual investment performance. The average assumed rate of return among public pension systems this year is 7.68 percent, KRS’ investment consultants told the board Thursday.

For more than a decade, Kentucky governors and lawmakers failed to contribute the recommended sums into the state pension systems, spending the money elsewhere as funding levels steadily dropped from around 100 percent. That inadequate support left KRS unable to recover from the 2008 recession. Elsewhere around the country, where state officials were more fiscally disciplined, the median state pension fund last year had bounced back to a 70 percent funding level.

The same Kentucky lawmakers who write the state budget keep their own state retirement accounts in a separate system, one that is 85 percent funded, and they repeatedly have rejected calls to merge their pensions into the ailing KRS.

At its Thursday meeting, the KRS board approved a resolution calling for the 2016 General Assembly to make the entire annual recommended contribution to KRS, as well as any additional funds it can provide.

Board members discussed different ideas for more state funding, such as a pension obligation bond. That would require the state to borrow billions of dollars from the bond market in the hope that its return on that money, wherever it was invested, exceeded the bond payments and interest. Generally, lawmakers have not been receptive to the idea of bonding to raise large sums for KRS or the Kentucky Teachers’ Retirement System, which also faces growing unfunded liabilities.

“It’s up to them to determine if it’s available and what the source is. But we obviously would recommend additional funding, given our current cash position,” KRS executive director Bill Thielen said after the board meeting.

Where to begin…

The fact that the state’s pension plans are this underfunded after an epic bull market in stocks, bonds and real estate means that in the next downturn the carnage will be breathtaking.

The fact that these funds are still expecting 7%+ returns going forward with investment-grade bonds yielding less than half that much and equities at valuation levels that have historically preceded bear markets implies that the people running these plans are clueless, desperate or some combination thereof.

The fact that the politicians’ pension plan is almost fully-funded implies that they know how to run such a program competently but have chosen not to bother keeping the promises they made to public sector union workers. Major electoral turmoil coming.

This is all shocking, of course. But why should non-Kentuckians care? Because a lot of other state pension plans are nearly as badly run, and the aggregate amounts are in the trillions of dollars. In the next stock or bond bear market, these funds’ problems will become too big to ignore and will either result in a wave of municipal bankruptcies or a federal bailout on the scale of 2008-2009, which is to say several trillion dollars.

Out there somewhere is a black swan so heavy that its landing breaks the current system. There’s no way to know which it will be, since the possibilities (junk bonds, over-the-counter derivatives, wide-spread war, emerging market dollar-denominated loans, a sudden bear market in a major asset class) are so numerous. But public pensions are definitely in the mix, and seem to be heading this way fast.